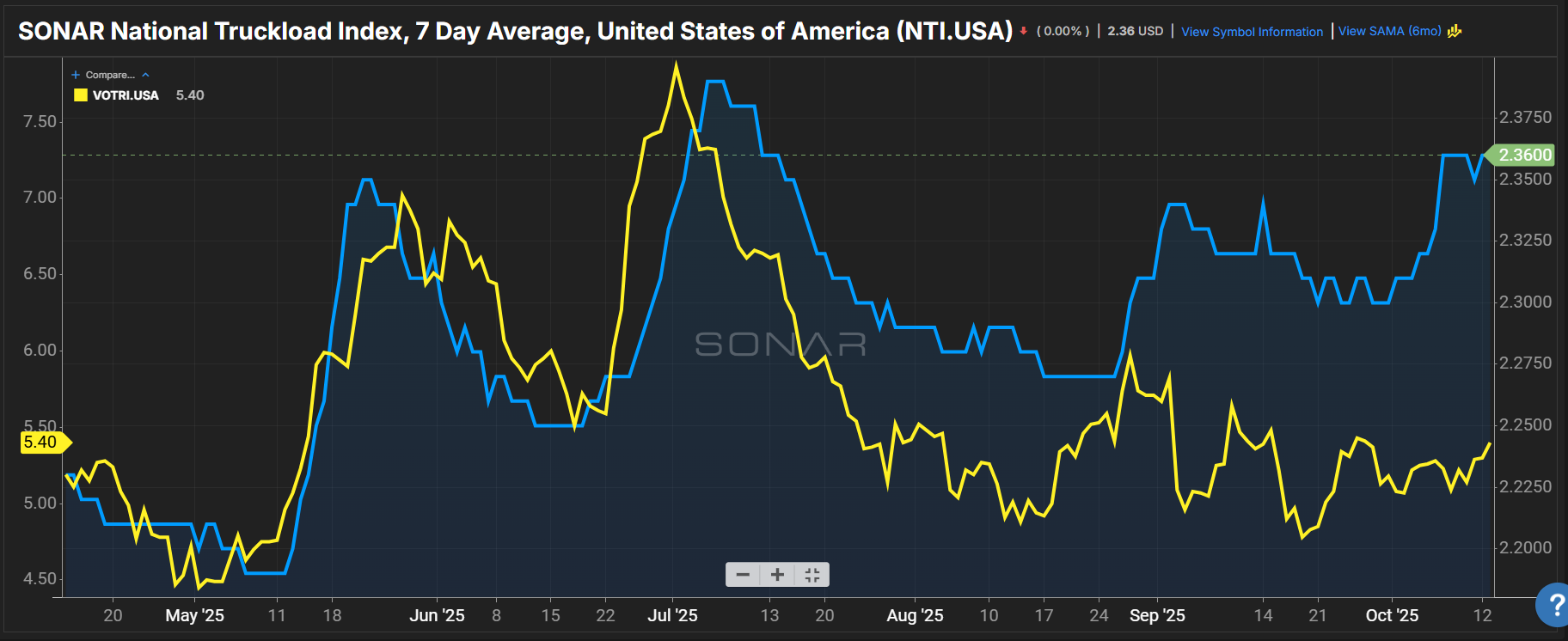

Summary: A rally in spot market rates that began the first week of October has stalled after reaching levels not seen since the week after the Fourth of July. The SONAR National Truckload Index 7-day average posted a gain of 3 cents per mile all-in week-over-week from $2.33 on Oct. 6 to $2.36 per mile.

On the contract front, dry van outbound tender rejection rates posted a slight gain. The Van Outbound Tender Rejection Index (VOTRI) rose 12 basis points week-over-week from 5.28% to 5.40%. Carrier pricing power continues to have an advantage compared to last year, but only slightly. VOTRI is 25 basis points higher year-over-year compared to 5.15% in 2024.

Fears over capacity being removed from the market due to increased regulatory scrutiny and enforcement remain. At this time, spot markets have reacted more akin to a DOT Roadcheck week, posting out-of-season gains compared to the last two years.

Carriers who utilize nondomiciled drivers who either had expired work authorizations or lacked English proficiency remain at risk. Anecdotally, reasons to bench these drivers stem more from them being deported for expired work visas than from the risk of being put out of service.

Expect more fog of war as the spot market begins its peak-season uptick during the first week of November. It will be difficult to gauge whether the uptick is directly related to spot market capacity leaving the market or to demand spikes. As it stands, if moves in the contract space continue to outpace those of the previous year, or a sudden and rapid uptick in tender rejection rates emerges, this may be one sign that the impacts of unauthorized capacity leaving the market are being felt.