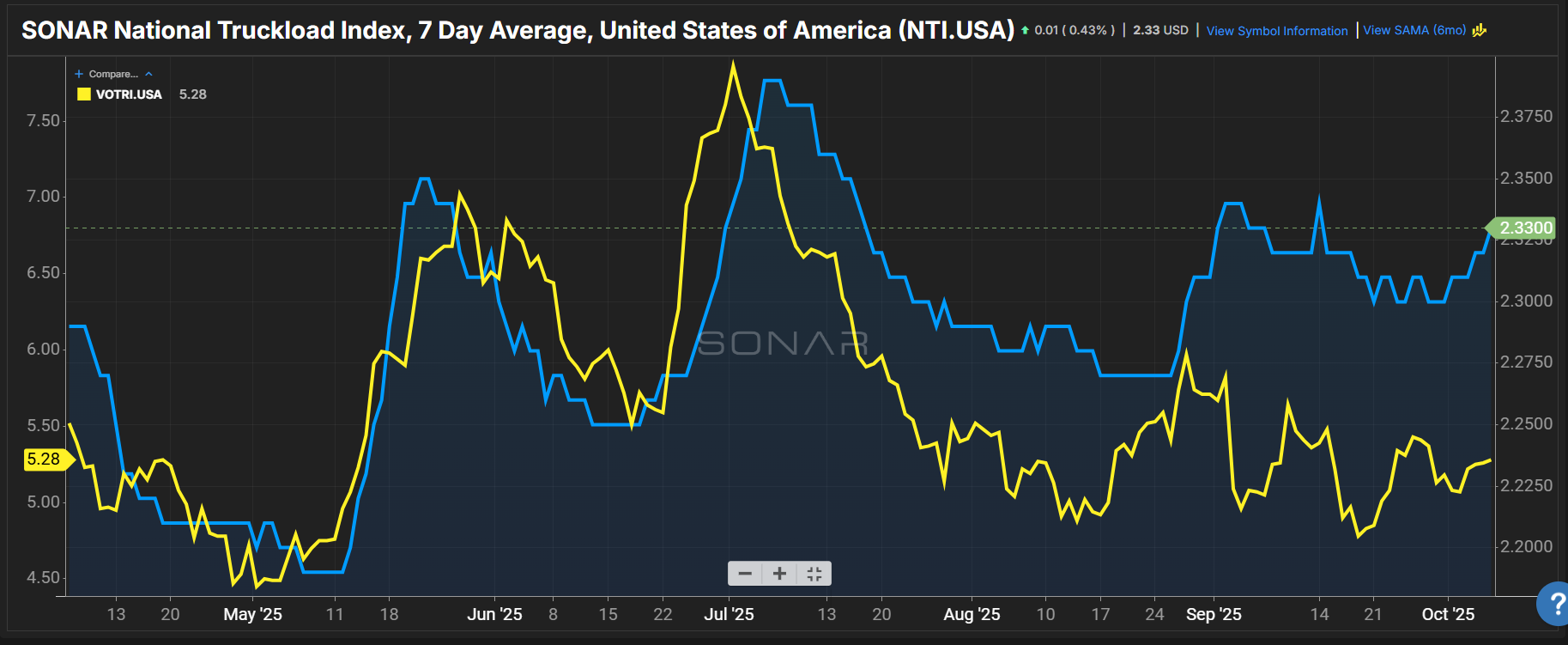

Summary: The first week of October saw improved dry van spot rates while outbound tender rejection rates continued to hover at or above 5%. The SONAR National Truckload Index 7-day average gained 3 cents per mile all-in week-over-week from $2.30 on Sept. 29 to $2.33 per mile. The rebound put the NTI at the same level as last month and 10 cents per mile higher than $2.23 last year.

Dry van outbound tender volumes also saw gains. VOTRI gained 15 basis points week-over-week from 5.13% to 5.28%. For the month, VOTRI is 23 basis points higher and 48 basis points more than last year’s value of 4.80%.

While pricing power saw slight gains due to less capacity, dry van demand remains depressed compared with the previous year. Dry van outbound tender volumes are at 6,788.04 index points, 1,533.58 points or 18.4% lower compared with 8,321.62 points in 2024.

Looking ahead, the challenge continues to be predicting what happens next. Ravi Shanker, transportation analyst at Morgan Stanley, told clients in a Monday report, “The year that promised so much has instead been a series of stop-start months as tariff uncertainty has taken its toll. Shipper uncertainty on the cycle remains high and visibility remains low, which makes predictions (or even looking backward) difficult.”

On the demand side, domestic manufacturing remains muted. FreightWaves’ Todd Maiden wrote, “Demand remains tepid across all modes with trucking more than three years into a freight recession. Manufacturing data again disappointed in September, with the Purchasing Managers’ Index (PMI) registering a 49.1 reading (50 is neutral), keeping it in negative territory for 33 of the past 35 months. The PMI new orders subindex—a signal for future activity—slid back into contraction at 48.9.”