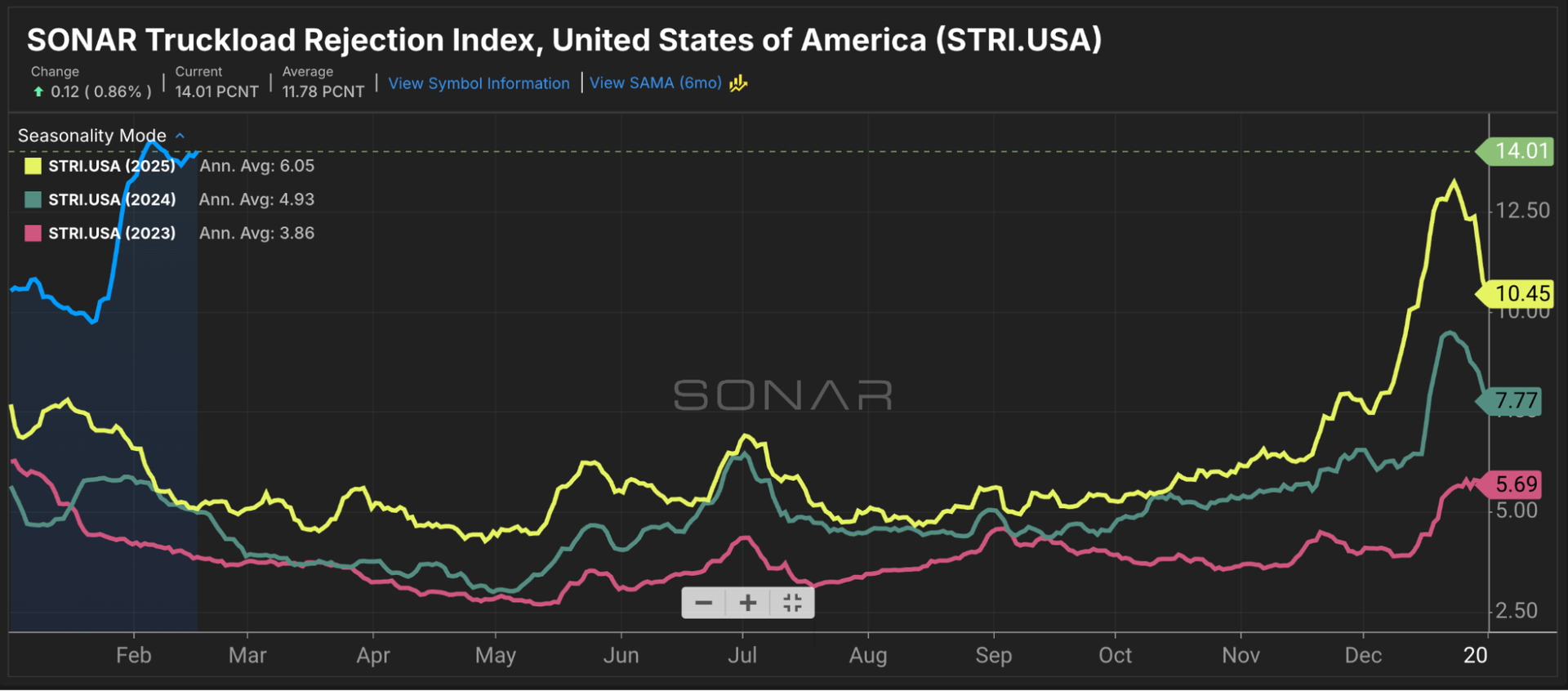

Summary: Nationwide outbound tender rejection rates remain elevated heading into mid-February. The out-of-season rally persists. Historically, the first quarter brings lower spot market and outbound tender rejection rates. At this time, the uniqueness and persistence of these elevated rates are notable. What happens next remains unclear.

The SONAR Truckload Rejection Index (STRI) gained 16 basis points week-over-week, rising from 13.85% on Feb. 9 to 14.01%. STRI is 405 basis points higher than 9.96% a month earlier and 881 basis points higher than 5.20% a year ago.

Tender rejection rates remain elevated in both the dry van and reefer segments.

The SONAR Truckload Rejection Index Van (STRIV) rose 40 basis points week-over-week from 12.46% to 12.86%. STRIV is 370 basis points higher than 9.16% a month earlier. Compared with a year ago, it is 816 basis points higher than 4.70%.

Reefer tender rejection rates are much higher than those in the van segment and the national average. The SONAR Truckload Rejection Index Reefer (STRIR) fell 28 basis points week-over-week from 19.65% to 19.37%. STRIR is 427 basis points higher than 15.10% a month earlier and 1,089 basis points higher than 8.48% a year ago.

Consistently elevated outbound tender rejection rates across multiple equipment types suggest enough truckload capacity has exited the market to create the volatility needed to shift the freight cycle from shipper-dominated to carrier-dominated. While the conditions exist, it is premature to declare a full shift toward carriers based on out-of-season first-quarter data.

Higher outbound tender rejection rates create a cascade effect as routing guides fail. Rejection rates at or above 10% typically lead to an uptick in spot market rates. Higher spot market rates, in turn, give carriers more reason to reject contracted lanes due to poor pricing or poor network fit. During this transition, repricing and strong relationships will be key for shippers and carriers navigating this volatile and rapidly changing environment.