|

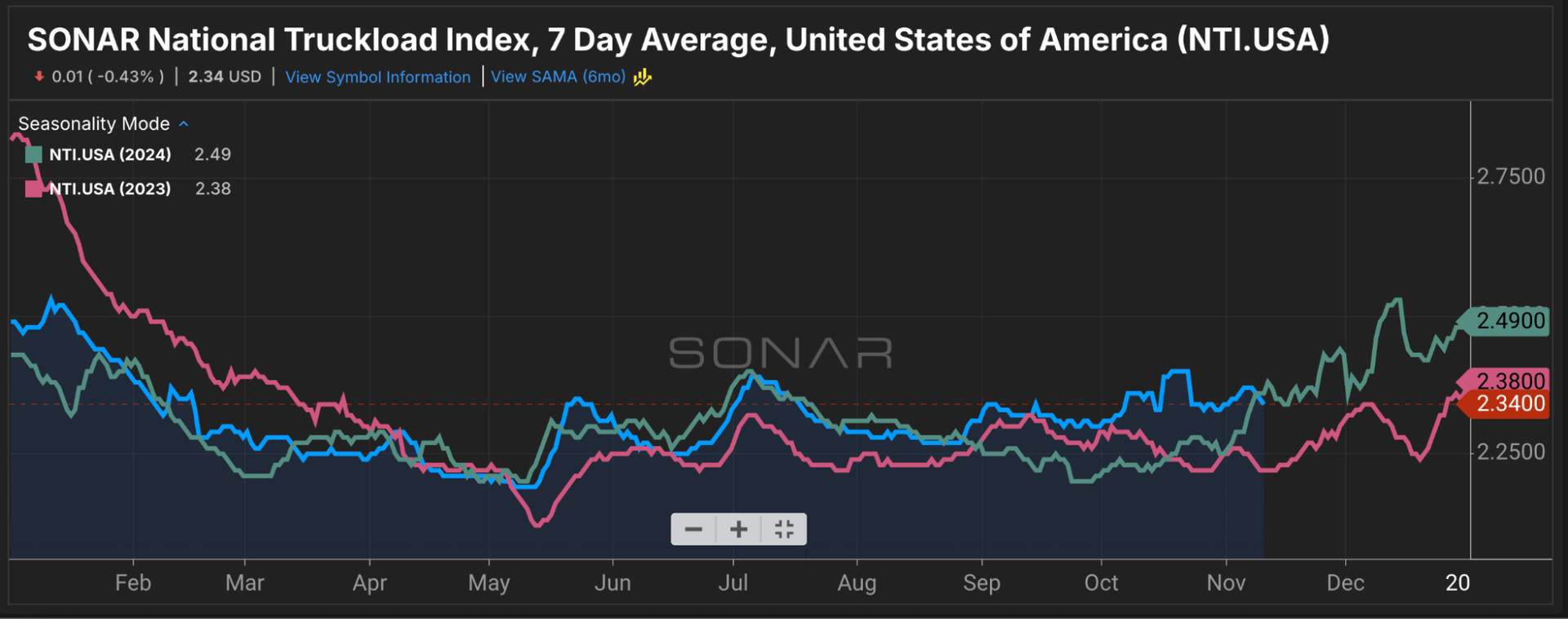

Summary: A nascent rally in dry van spot rates has stalled, ending a two-month streak in which the SONAR National Truckload Index 7-day average outperformed 2024 rates. The NTI fell 1 cent per mile week over week from $2.35 on Nov. 3 to $2.34. Compared to last year, the NTI is now 4 cents per mile, or 1.7 percent, lower than $2.38. Despite the declines, the NTI is 12 cents per mile higher than $2.22 in 2023.

Dry van outbound tender rejection rates also fell over the past week from 5.65 percent to 5.49 percent, a decline of 16 basis points. Compared to last year, VOTRI remains in a more positive position, up 34 basis points versus 5.15 percent.

While spot and tender rejection rates fell, the dog that isn’t barking is the backdrop of notably lower outbound tender volumes. OTVI is sitting at 6,700 points compared to 8,203 and 8,005 in 2023 and 2024, respectively. That’s approximately 1,305, or 16 percent, lower compared to last year. It remains to be seen if dry van outbound tender volumes improve. If that occurs, then conditions are fertile for an uptick in both spot market and outbound tender rejection rates, as enough truckload capacity has left the market through attrition and regulatory pressures to cause a measurable uptick.

On the regulatory front, a recent stay issued by a district court judge has blocked the FMCSA’s implementation of its recent final rulemaking limiting non-domiciled CDLs. FreightWaves’ John Gallagher writes, "With a stay in place, state driver’s licensing agencies presumably can resume issuing and renewing non-domiciled CDLs until the court decides whether to reject the lawsuit or issue a permanent stay, which could take weeks."

|