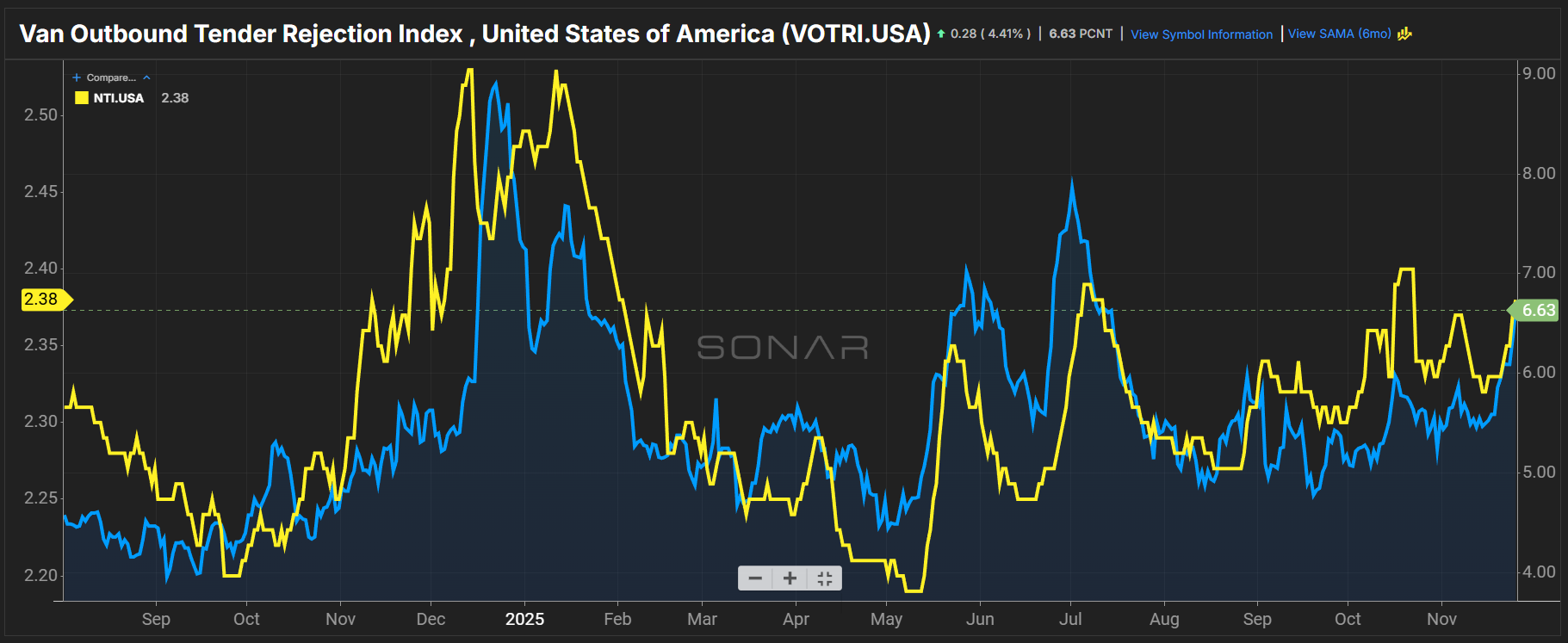

Summary: With the arrival of Thanksgiving comes the arrival of another seasonal uptick in the dry van sector as capacity ebbs and drivers return home for the holiday. When looking at the uptick compared to last year, 2025’s peaks more closely resemble fits and starts than the noticeable and sustained uptick of 2024. The next question is one of extent: Will the peaks of 2025 break 9% or will lower truckload demand continue to weigh down on truckload capacity?

That answer will come in the final weeks of 2025. Until then, truckload capacity continues to tighten along seasonal expectations. Dry van outbound tender rejection rates rose 104 basis points week over week from 5.59% on Nov. 18 to 6.63%. VOTRI is 101 basis points higher than 5.62% last month, and 104 basis points higher than the previous year.

Dry van spot market conditions also tightened but remain lower compared to the previous year. The SONAR National Truckload Index seven-day average gained 5 cents per mile all-in from $2.33 per mile to $2.38 per mile. That is the same gain as last month but 4 cents per mile lower than $2.42 in 2024.

The next push against truckload capacity, begun by the FMCSA through its interim final rulemaking targeting non-domiciled CDL holders, may come from the freight validation tools brokers and shippers use to tender loads. It’s one thing for the government to regulate and identify bad actors, but another thing entirely for them to book loads and engage in interstate commerce.

A recent announcement by freight validation platform Highway appears to be targeting this scrutinized segment with the recent release of a new feature allowing brokers and shippers the ability to identify carriers who have drivers with a non-domiciled CDL. These are the early days of private enterprise attempting to address the recent flurry of government scrutiny, which is now tied up in legal battles and partisan politics.

For truckload capacity, the outcome is the same: additional limits to who and what can be hauled, whether government- or privately mandated. Whether this is enough to tip the scales for the truckload capacity that is left remains to be seen, as truckload demand remains muted in the face of macroeconomic headwinds and tariff-related uncertainty.