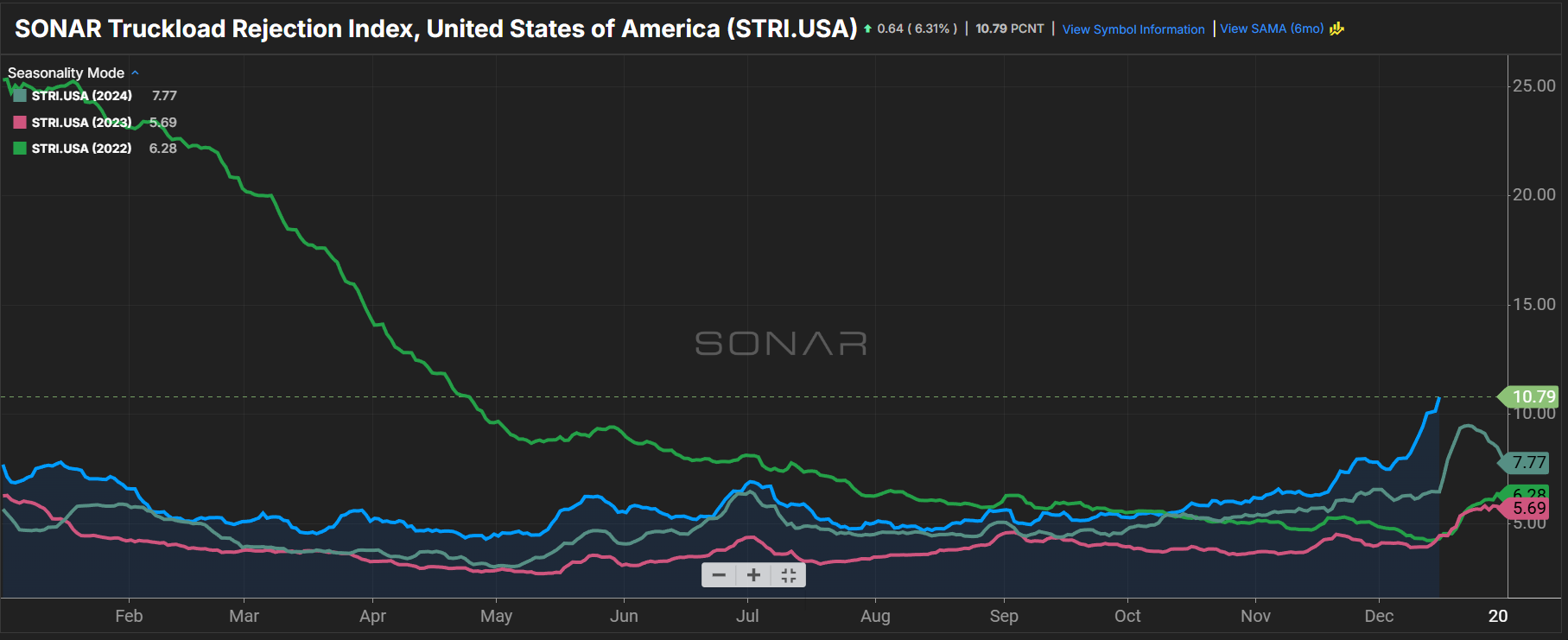

Summary: Nationwide outbound tender rejection rates continue to climb, reaching levels not seen since April 24, 2022. In the past week, the SONAR Truckload Rejection Index (STRI) rose 255 basis points, from 8.24% on Dec. 8 to 10.79%. That marks an increase of 448 basis points from 6.31% last month and 366 basis points from 7.13% last year — before the 2024 peak season pre-Christmas surge.

The trend looks even more impressive over the past three years. The current STRI is 634 basis points higher than the 4.45% recorded at this point in 2023 and 649 basis points higher than the 4.30% from 2022.

On the truckload demand side, tender volumes are lower than in the previous three years — but not by much. According to the SONAR Truckload Volume Index (STVI), volumes are 347.46 points, or 3.1%, lower than in 2024; 286.17 points, or 2.57%, lower than in 2023; and 150.59 points, or 1.37%, lower than in 2022.

Overall truckload demand has remained muted, running at or below levels from the last three years for most of 2025. The one exception: a notable narrowing in the spread following Thanksgiving.

Breaking down the tender rejection rates by mode shows similar upward movements in both the dry van and reefer segments. The SONAR Truckload Rejection Index for vans (STRIV) jumped 224 basis points week over week, from 7.36% to 9.60%. The reefer segment also gained ground but remains in a much more favorable pricing power position. The SONAR Truckload Rejection Index for reefers (STRIR) rose 351 basis points week over week, from 13.10% to 16.61%.

Compared with last year, both van and reefer rejection rates show notable improvement. The STRIV is up 310 basis points from 6.50% in 2024. The STRIR saw a larger year-over-year increase of 447 basis points from 12.14%.