Summary: The third week of February saw a slight softening in nationwide outbound tender rejection rates, while outbound tender volumes remained elevated.

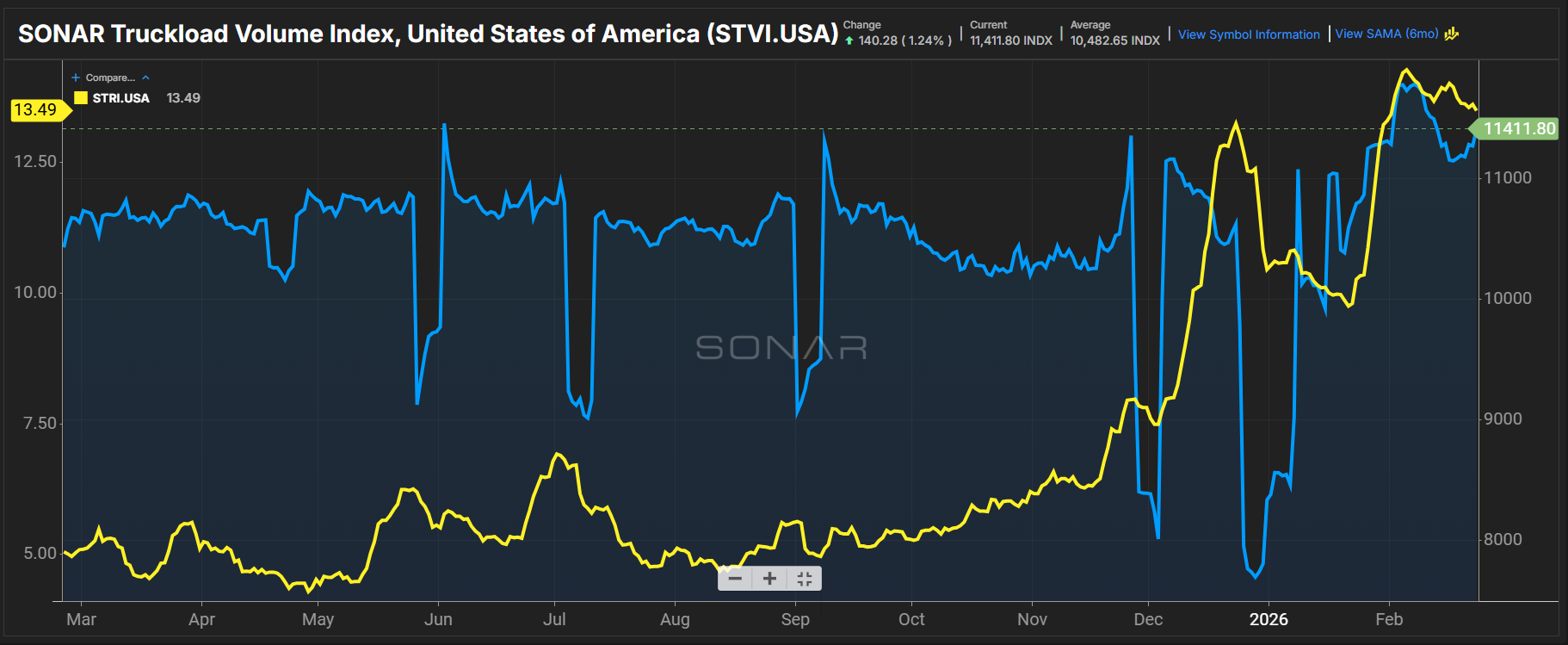

Record tender rejection rates continue to stabilize as winter storm-related disruptions coincide with an aggressive trucking regulatory environment not seen in decades. The SONAR Truckload Rejection Index (STRI) fell 52 basis points week-over-week from 14.01% on Feb. 16 to 13.49%. The STRI is 316 basis points higher than 10.33% a month ago and 844 basis points higher than 5.05% a year ago.

Tender volumes are elevated and posted week-over-week gains. The SONAR Truckload Volume Index (STVI) gained 258.12 points, or 2.3%, week-over-week from 11,153.68 points to 11,411.8 points. The STVI is 600.71 points, or 5.6%, higher than 10,811.09 points a month ago. Compared with a year ago, it is 982.91 points, or 9.4%, higher.

The STVI is outperforming levels from the past three years at this time in February. The recent trend began in the first week of February. The contrast between marginally higher outbound tender volumes and significantly higher outbound tender rejection rates suggests that substantial carrier attrition in the contract space has occurred.

This can create a preference cascade for carriers that may wish to reprice lanes or adjust their commitments, depending on rates or their relationships with customers or freight brokers.

Another possible reason for the elevated tender rejection rates is that many large nationwide carriers are migrating to dedicated lanes. Dedicated operations run on multiyear contracts, compared with one-way over-the-road freight where bid cycles may be quarterly, monthly or annual.

FreightWaves’ Todd Maiden recently wrote about changes at some of these publicly traded carriers.

Schneider’s dedicated business (8,500 tractors) now accounts for 70% of its total truckload revenue, compared with just 34% prior to the pandemic.

Werner’s one-way fleet stood at nearly 3,300 tractors in 2022 but ended 2025 with fewer than 2,400 units. While Werner’s one-way fleet declined, it is now the fifth-largest dedicated provider in the U.S., with roughly 7,400 trucks. More than 70% of its truckload fleet is tied to dedicated agreements.

J.B. Hunt plans to add 800 to 1,000 trucks each year to its dedicated fleet, which sits around 12,600 units. Hunt’s one-way truckload segment relies more on independent contractors to haul freight in J.B. Hunt trailers.

Fewer large truckload players in the one-way space due to the extended Great Freight Recession is one underreported factor possibly explaining the higher-for-longer rejection rates.

Another may come from the greater market penetration of freight brokerages in shipper routing guides — a fantastic deal when rates are lower and more predictable but riskier when the capacity they rely on is more opportunistic and less likely to honor a lower rate as pricing power rapidly improves.