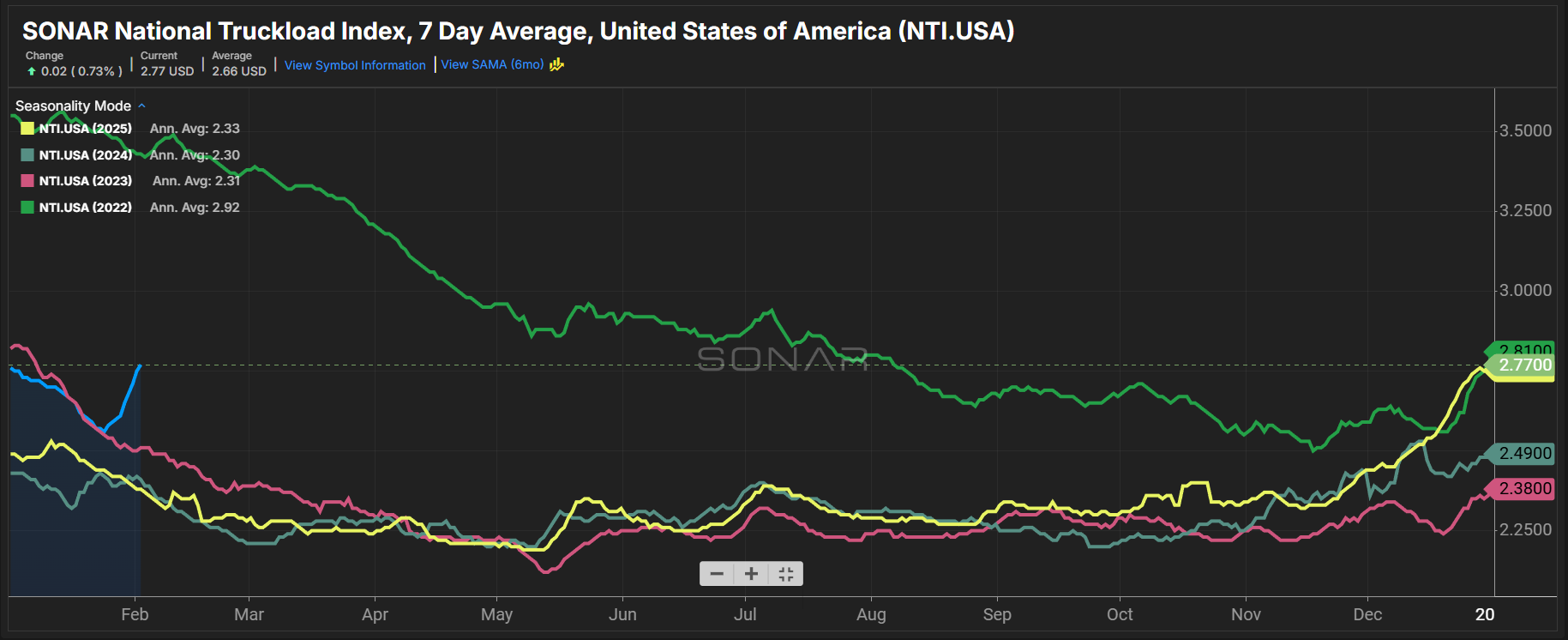

Summary: The spot market rally continues, with dry van spot rates reaching their highest levels since January 2023. The rally, which began in anticipation of Winter Storm Finn, has extended into the first week of February.

The SONAR National Truckload Index (NTI) 7-day average rose 18 cents per mile week over week, from $2.59 per mile all-in to $2.77 per mile. The NTI is 2 cents per mile higher than last month’s $2.75 and 40 cents, or 16.9%, higher than last year’s $2.37.

Dry van spot rates are being buoyed by a similarly rapid increase in dry van outbound tender rejection rates. The SONAR Truckload Rejection Index Van (STRIV) jumped 283 basis points week over week, from 9.85% to 12.68%. The STRIV is 290 basis points higher than last month’s 9.78% and 704 basis points higher than last year’s 5.64%. The STRIV is at its highest level since April 2022.

Other transportation metrics also showed capacity tightening in January. The January Logistics Managers’ Index reported a 47.1 reading for transportation capacity, indicating contraction. However, this second consecutive month of transportation capacity contraction was less severe than December’s 36.9 reading. That December reading was the fastest drawdown in transportation capacity since October 2021.

FreightWaves’ Todd Maiden writes, “Public truckload carriers and 3PLs reporting fourth-quarter results have consistently pointed to increased regulatory pressure on the driver pool — English-language proficiency requirements, non-domiciled CDL restrictions, and ELD and driver school crackdowns — as a factor forcing truck capacity out of the market. Severe winter weather has also been a catalyst behind the market tightening.”