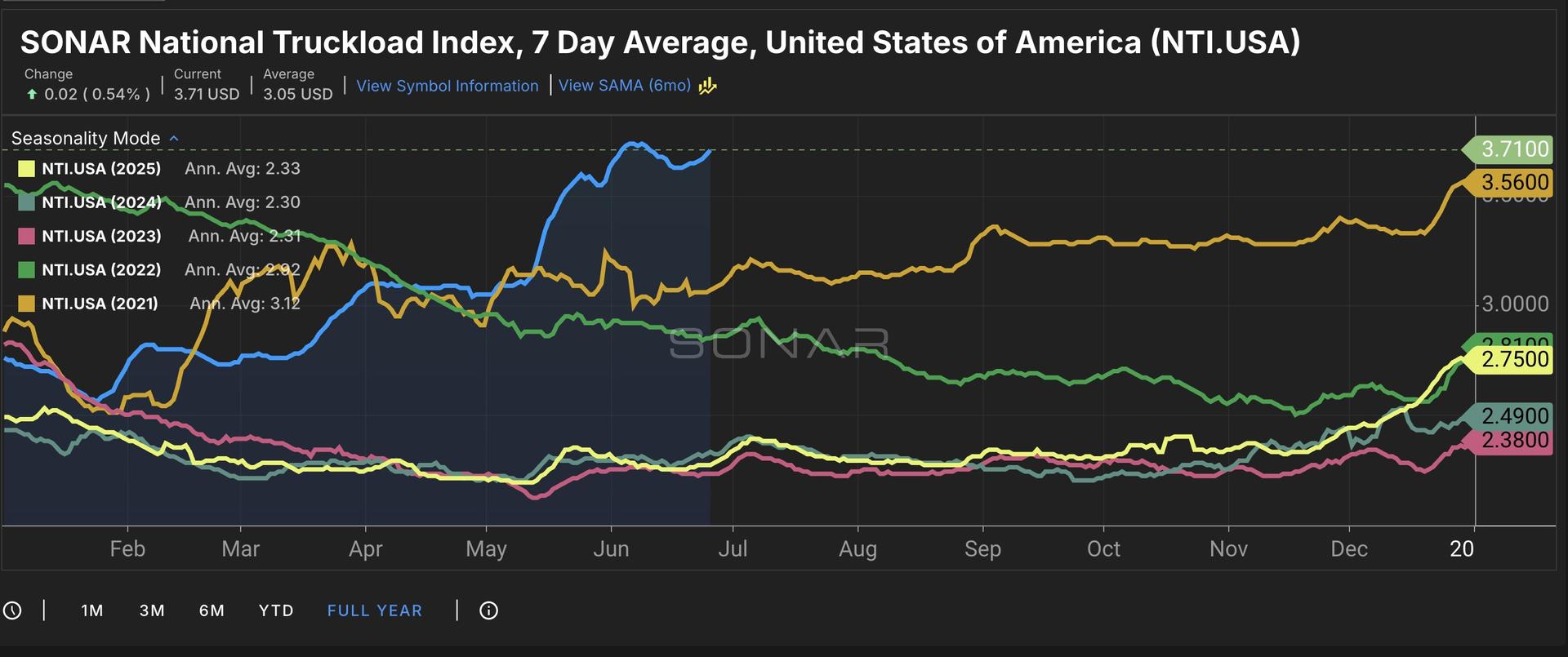

Summary: As June draws to a close, spot rates have resumed their climb, approaching levels not seen since Memorial Day. The SONAR National Truckload Index seven-day average (NTI) remains at record levels, at its highest in five years. All-in spot rates suggest that trucking capacity continues to benefit from reduced competition, partly due to a government regulatory crackdown and partly from carrier exits amid the impacts of previous years’ cost inflation.

The NTI gained 8 cents per mile week over week, rising from $3.63 on June 18 to $3.71. That’s 12 cents per mile, or 3.3%, higher than $3.59 last month and $1.43 per mile, or 63%, higher than $2.29 per mile last year.

For spot market rates, expect continued increases leading up to the Fourth of July weekend, when trucking capacity typically wanes as drivers take time off to spend with their families during the extended holiday weekend. Fleets’ working tractor percentages will similarly face struggles in both the contract and spot markets due to reduced driver availability.

For drivers or owner-operators who stay out, there is an opportunity to take advantage of higher rates, but there are risks, as some facilities may have limited hours or be closed before or after the holiday weekend.

Another positive sign for cash-strapped carriers has been falling fuel costs related to the Strait of Hormuz conflict and the tentative ceasefire. A key development to watch is whether the ceasefire holds and fuel costs continue to fall — and, if so, whether spot market rates will decline. All-in spot rates include fuel. However, carriers are more beholden to all-in rates when quoting spot market transactions than in the contract market, which typically includes dedicated fuel surcharges.

While carriers are securing higher rates, they face some possible headwinds. Competition for qualified and skilled drivers will continue. Fleets traditionally offer incentives such as sign-on bonuses or opportunities to drive newer equipment to attract drivers. Whether a similar arms race of sign-on bonuses will emerge remains to be seen. The last time this behavior was meaningfully observed was during the COVID freight boom. This upcycle will be different. It is much harder to recruit new drivers due to greater regulatory oversight. What this means for hiring and retention goals remains to be seen.