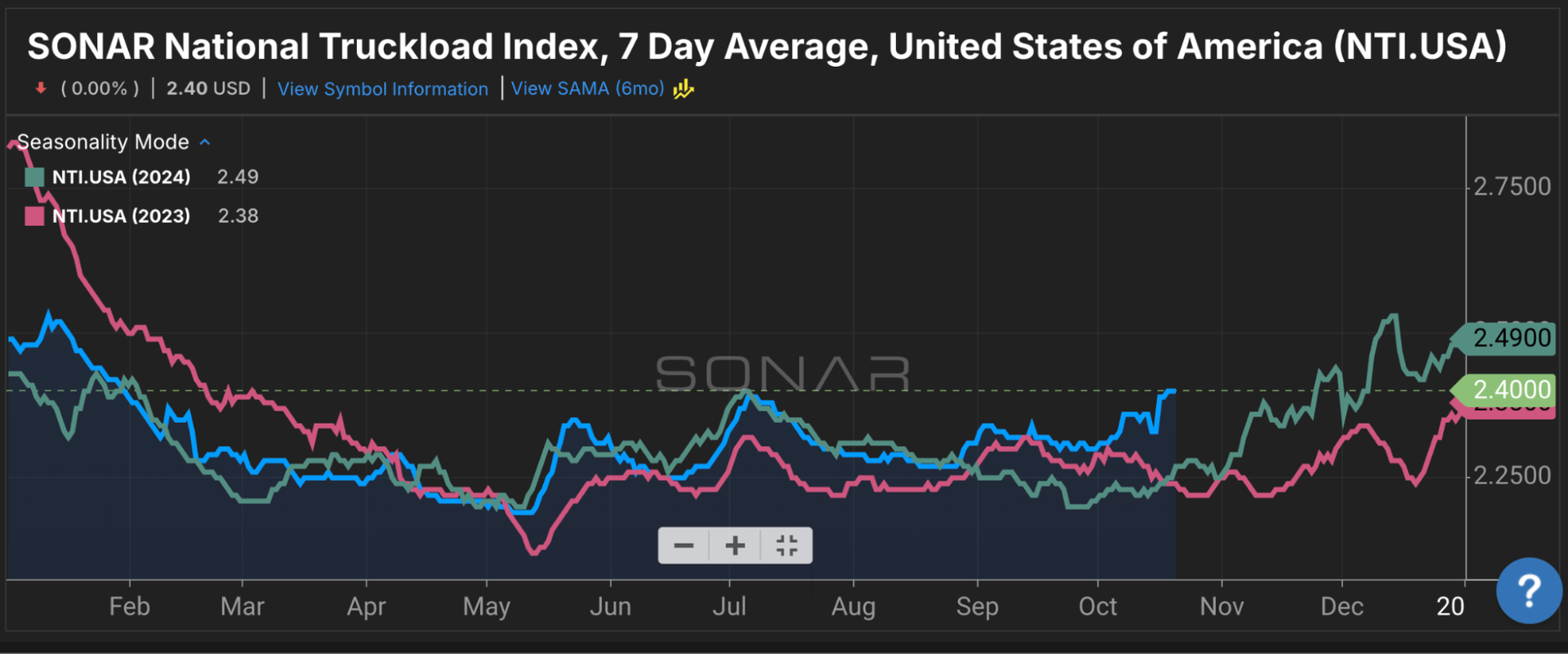

Summary: A rally in dry van spot rates continues as concerns over truckload capacity push rates to levels not seen since late January. The SONAR National Truckload Index 7-Day Average rose 4 cents per mile week over week from $2.36 on Oct. 13 to $2.40 all-in. This is the highest rate since Jan. 30. The NTI is now 13 cents per mile higher than $2.27 in 2024 and 16 cents per mile higher than $2.24 in 2023.

Dry van outbound tender rejection rates also saw week-over-week improvements. VOTRI rose 36 basis points from 5.40% to 5.76%. Compared to the previous two years, VOTRI is 123 basis points higher than 4.53% in 2024 and 221 basis points higher than 3.55% in 2023.

A challenge for peak season predictions remains that truckload capacity continues to decline in tandem with declining truckload demand via lower outbound tender volumes. This creates the potential for greater market volatility, especially in the more volatile spot market space.

One sign that current rates are outside of seasonal expectations comes from the SONAR seasonally adjusted moving average (SAMA) feature, which projects a rapid drop in spot market rates before a steady stair-step improvement through late November into late December. At this time it appears that spot market rates should continue to rise in the next week based on the daily movement in the National Truckload Index, which feeds the NTI 7-Day Average.