Cass TL Linehaul Rates Advance in June as Volume Inflection Slips

|

|

|

|

|

|

NEWSLETTER SPONSORED BY – TRUCKSTOP.COM

|

Whether you’re booking loads or hauling them, Truckstop gives you the tools, the rates, and the network to keep moving. Visit Truckstop.com.

|

|

|

|

This week’s top stories in trucking

|

|

|

|

SBTC Faces Uphill Battle in Bid to Strip New York, California of CDL Authority

|

The Small Business in Transportation Coalition sharpened its arguments in July 10 filings to the D.C. Circuit, asking the court to compel FMCSA to decertify the CDL programs of New York and California and to suspend both states’ licensing authority until they reach substantial compliance. The core question is whether 49 U.S.C. §31312 makes decertification mandatory once the transportation secretary finds a state substantially noncompliant. Transportation attorney Greg Reed of Hanson Bridgett says the case hinges on one word — "shall" — and that DOT retains broad discretion, including withholding highway funds, with no requirement of immediate decertification. Reed called the petition strangely postured, since the APA typically reviews agency action rather than inaction, and suggested it may function more as political pressure than litigation. The stakes aren’t small: CVSA says a decertification order would restrict new issuance, renewals, transfers and upgrades, while previously issued CDLs stay valid to expiration.

|

|

|

|

Cass: TL Linehaul Rates Advance in June, Volume Inflection Delayed

|

Cass Freight Index shipments fell 4.1% year over year in June, an acceleration from May’s 1.2% dip, and slid 3.1% month over month. Expenditures ran the other way, surging 11.2% y/y on higher rates and a 40% y/y jump in retail diesel. The TL linehaul index — rates excluding fuel and accessorials — rose 5.5% y/y, its 18th straight monthly gain, though it came in 0.9% below May. Cass attributed soft volumes partly to declining capacity, noting double-digit growth in the comparatively small domestic intermodal sector doesn’t move a trucking-weighted index, and flagged higher fuel as a drag on goods demand. A May projection of 1.8% y/y back-half volume growth wasn’t repeated. Cass says the recovery looks delayed by a brief bout of inflation, with tighter supply still the main driver of accelerating rates; many shipper bids taking effect July 1 make the June dip likely temporary.

|

|

|

|

Trucking Costs Outpaced Consumer Inflation in ’25: ATRI

|

Average operating costs across all fleet sizes rose to $2.336 per mile in 2025 from $2.260 in 2024, a 3.4% increase, per the American Transportation Research Institute’s annual survey. Strip out fuel — which carriers commonly pass through via surcharge — and the figure went to $1.854 from $1.779, up 4.2%, or 1.5 percentage points above inflation and 0.6 points above the prior year’s increase. No single line item ran away from the pack: lease and purchase payments hit 40.4 cents per mile, repair and maintenance 21.5 cents, insurance 10.6 cents, tires 5 cents. Driver wages rose 2.5%, a sub-inflationary rate, while benefits jumped 6.6% — the second straight year benefits outpaced wages. Average starting bonuses fell to $1,733 from $2,122. Turnover dropped to 44.2% from 48%, but split hard by size: 70.7% at truckload fleets above 1,000 trucks versus 32% at fleets under 26.

|

|

|

|

Navistar Defeats $16.5M Lawsuit Over Delayed Truck Deliveries

|

A 10-person Michigan federal jury found Monday that GLS LeasCo and Central Transport failed to prove breach of contract and fraud claims against Navistar, awarding nothing on a $16.5 million demand. The dispute traced to a 2022 agreement under which GLS committed to 1,100 model-year 2023 International tractors after waiving a trade-in arrangement — a concession GLS said it made because Navistar promised an accelerated build schedule that would let it sell used equipment into a historically hot market. GLS alleged only 18 tractors arrived by the end of May 2022 with deliveries stretching into September 2023, dropping the value of its 2018 tractors more than 75% and costing roughly $15.7 million in resale value plus $1 million in maintenance. Navistar argued the letter agreement set production slots rather than delivery dates and pointed to supply-chain disruption, including Bendix Fusion component shortages. No appeal has been indicated.

|

|

|

|

Tesla, Paper Transport Partner on Electric Semi Evaluation in Chicago

|

De Pere, Wisconsin-based Paper Transport Inc. is evaluating the Tesla Semi Long Range in dedicated operations in the Chicago market, the carrier said in a Monday blog post. PTI is testing the truck inside its dedicated model, where predictable lanes and consistent mileage make for a cleaner read on battery-electric performance. CEO Tyler Ellison framed the partnership as an extension of a portfolio that already includes renewable natural gas and intermodal, giving customers additional paths to cut Scope 3 emissions without giving up service or economics. PTI has logged more than 87 million miles on compressed and renewable natural gas across a 15-year sustainability push. The pilot lands as Tesla ramps volume production of the Class 8 electric truck; Elon Musk told investors on the Q1 call to expect a slow start following an S-curve, with supply chain complexity capping early output before scaling into 2027.

|

|

|

|

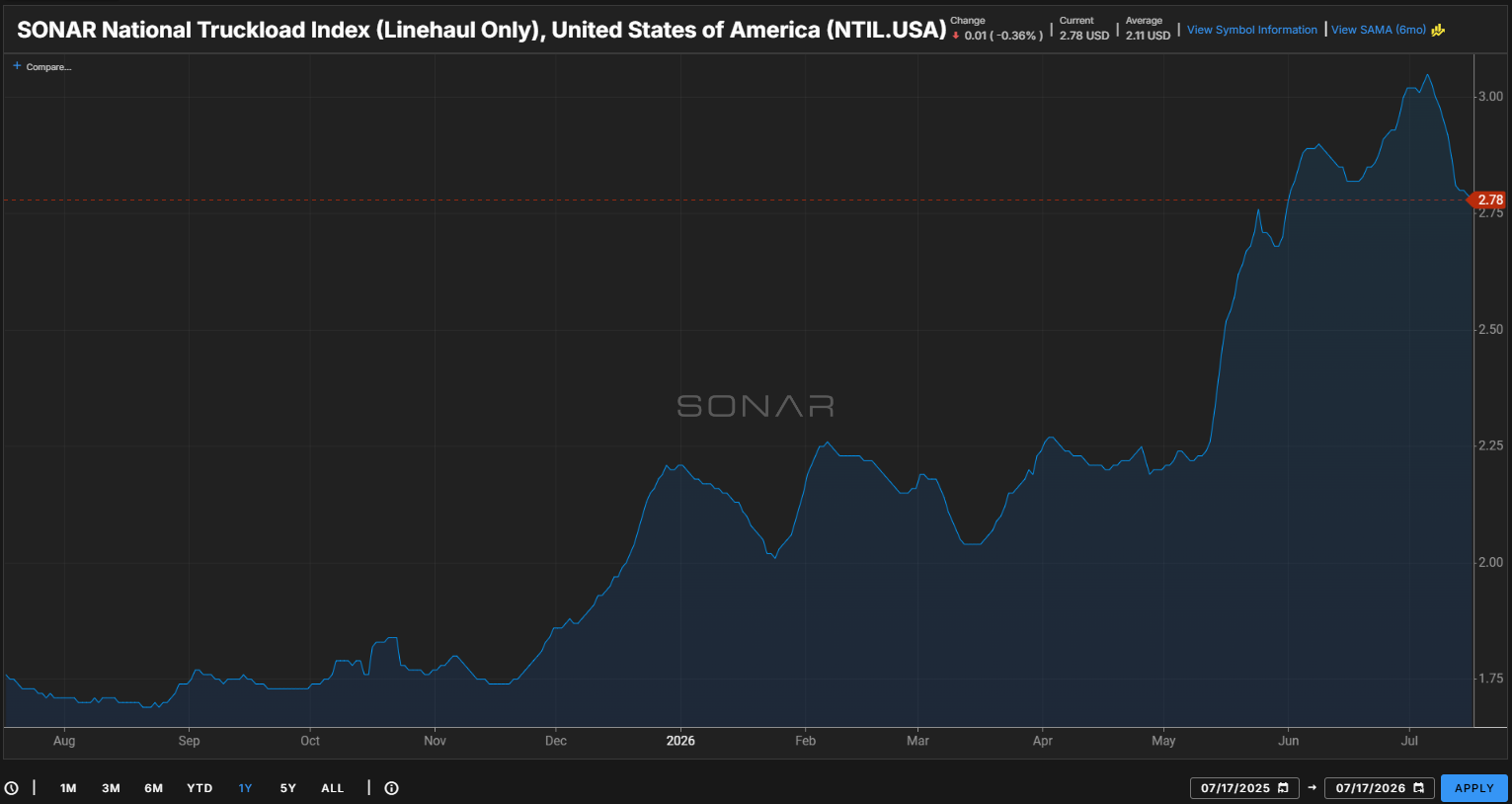

SONAR spotlight: Spot rates party like it’s the Fourth of July

|

Summary: The National Truckload Index (Linehaul Only), NTIL.USA, sits at $2.78 per mile, off 0.36% — about a penny — on the day, and roughly 27 cents below the early-July peak just above $3.05. Even after the slide, linehaul spot rates remain 67 cents above the $2.11 trailing-year average and far above where the market sat a year ago. The move reads as a rollover off an overheated top rather than a return to the old range: the index is still nearly a dollar above last summer’s floor.

Diving into the data, the NTIL held near $1.75 from August through late November before its first real leg up, running to about $2.20 by mid-January. It chopped between $2.00 and $2.25 through the winter and spring — a false start in February, a pullback to $2.05 in March — then broke hard in May, adding roughly 80 cents in six weeks to crest above $3.00 in late June and peak in early July. The reversal since has been the sharpest single move on the chart, but it has retraced only about a third of the May-June run.

To calculate the NTIL, fuel costs are based on the average retail price of diesel and an assumed fuel efficiency of 6.5 miles per gallon. The formula is NTID – (DTS.USA / 6.5).

Looking ahead, the supply story that drove the run-up hasn’t changed — Cass tied June’s 4.1% year-over-year shipment decline partly to capacity leaving the market, and its TL linehaul index has now been up y/y for 18 straight months. What’s changed is the top. Watch whether $2.75 holds as support or the index keeps bleeding toward the mid-$2.50s. With many shipper bids taking effect July 1 and contract rates lagging spot by a couple of weeks, carriers repricing off the July peak may find the market has already moved under them.

|

|

|

|

The Routing Guide: Links from around the web

|

|

|

|

THE OLD POST OFFICE, CHICAGO | JULY 15, 2026

|

|

|

|

FWTV EVENT | JULY 28, 2026

|

|

|

|

Like the content? Subscribe to the Newsletter!

|

|

|

Loaded and Rolling Podcast links:

|

|

|

Download the FreightWaves App

|

|

|

|

|