| • |

Revised Russia Sanctions Bill Could Impose Up to 100% Secondary Tariffs on China, India: A draft Senate bill introduced on July 14 would pair new sanctions on Russia with steep secondary tariffs on countries that continue buying Russian oil and natural gas. |

| • |

The bill surfaced just days after the death of Sen. Lindsey Graham, one of the sanctions push’s lead sponsors. |

| • |

Secondary tariffs on major purchasers of Russian energy, chiefly China and India, could reach as high as 100%. |

| • |

The measure is still in draft form; scope, effective dates, and exemptions have not been finalized. |

| • |

Importers sourcing from China or India should track the bill’s progress and use the Flexport Tariff Simulator to stress-test landed costs against a potential 100% secondary tariff scenario. |

| • |

DOJ Opens Another Trade Enforcement Unit, Publishes Trade Fraud Guidance: The Department of Justice (DOJ) added a new trade enforcement unit to its existing footprint and released a companion guide detailing how it plans to pursue customs and trade fraud cases. |

| • |

The guide lays out DOJ’s enforcement priorities, likely covering duty evasion, undervaluation, and transshipment schemes. |

| • |

The additional unit signals DOJ is scaling up trade enforcement capacity rather than treating it as a one-off initiative. |

| • |

Importers should revisit compliance controls now; Flexport’s Audit Your Customs Broker tool can flag entries with tariff stacking issues or overpaid duties before they draw scrutiny. |

| • |

BIS Signals ICTS Rule Could Expand Beyond Connected Vehicles: At a July 14 House Foreign Affairs Committee hearing, the head of the Bureau of Industry and Security (BIS) said the Information and Communications Technology and Services (ICTS) rule may extend to additional sectors once the agency’s connected-vehicles work winds down. |

| • |

Broader export control issues drew more committee attention than ICTS itself during the hearing. |

| • |

No specific new sectors or timeline have been named; further detail is expected as the connected-vehicles rule concludes. |

| • |

USTR: Current Tariffs Expected to Outlast the Trump Administration: The Office of the U.S. Trade Representative (USTR) indicated that existing tariff measures are likely to remain in place well beyond the current administration’s term. |

| • |

The comment reinforces that businesses should treat current tariff levels as a durable cost of doing business, not a temporary policy. |

| • |

CBP Advances System and Compliance Updates: U.S. Customs and Border Protection (CBP) rolled out several administrative changes this week. |

| • |

A new Automated Commercial Environment (ACE) function goes live July 16, allowing removal of inactive Importer of Record (IOR) numbers. |

| • |

CBP issued Harmonized System (HS) updates and posted new antidumping and countervailing duty (AD/CVD) case messages as of July 13. |

| • |

The Food and Drug Administration (FDA) separately issued new and revised import alerts on July 13, relevant to FDA-regulated importers. |

| • |

CBP also published several miscellaneous releases during the week; importers with inactive IOR numbers should confirm status before the July 16 change takes effect. |

| • |

AD/CVD Preliminary Determinations Span Aluminum, Cabinetry, and Chemical Sectors: The Department of Commerce issued a wave of preliminary AD/CVD results this week, alongside new case notices and fresh International Trade Commission (ITC) investigations. |

| • |

Importers in these product categories should review the preliminary rates for potential duty impact; Flexport’s Trade Advisory group can assist with comments or protests ahead of final determinations. |

| • |

Preliminary AD and CVD administrative review results for Bahrain aluminum sheet. |

| • |

Preliminary AD and CVD administrative review results for China wooden cabinets and vanities. |

| • |

Preliminary CVD administrative review results for India aluminum sheet. |

| • |

Preliminary AD administrative review results for Taiwan brightening agents. |

| • |

Preliminary AD and CVD administrative review results for Turkey aluminum sheet. |

| • |

Commerce also published new AD/CVD notices and the ITC opened new investigations, both dated July 14. |

| • |

Section 301 Tariffs Announced on Brazil: Last year’s 301 investigation on Brazilian unfair trade practices recommended a 25% tariff on goods of Brazilian origin. |

| • |

These tariffs are effective July 22nd, 2026 and will stack with existing 122 duties of 10% until July 24th. |

| • |

After July 24th, when Section 122 duties are expected to expire, the 25% Section 301 duties will remain. |

| • |

Exemptions exist for donations, informational materials, parts of civil aircraft, and naturally unavailable resources that are not found in sufficient quantities in the US. |

| • |

There is also an in-transit provision for goods that departed prior to July 22nd which arrive and clear customs before July 29th. |

OCEAN MARKET NEWS

| • |

A renewed military conflict between the U.S. and Iran has closed the Strait of Hormuz to normal commercial transit since July 10. Vessel tracking shows transits down roughly 60% versus the prior week, and under a realistic delay-adjusted scenario, roughly 200k twenty-foot equivalent units (TEU) of container capacity is now restricted or trapped in the region. One container ship was disabled by fire after an attack while transiting the strait. |

| • |

This is a separate event from the Red Sea disruption that has affected Asia-Europe and Asia-East Coast shipping since late 2023. That disruption remains active: after a period of relative calm and a partial return of some Suez Canal transits, a cargo vessel came under attack off Yemen’s coast on July 5. Threats of renewed attacks have raised route uncertainty again, even though there have been no confirmed strikes on container ships since 2025. |

| • |

Global schedule reliability sits near 65% as of May, still below pre-pandemic norms but the highest so far this year. Blank sailing activity remains modest industry-wide, at a 3% cancellation rate for the 5 weeks through early August, concentrated on Trans-Pacific Eastbound (63% of all blanks) and Asia-Europe (29%). |

| • |

Global container freight rates have risen for 5 straight weeks, up 9% week over week as of July 2, driven by an early and compressed peak season plus tightening capacity. Spot rates on Asia-U.S. West Coast lanes have risen roughly 120% since mid-May; Asia-U.S. East Coast rates are up about 85% over the same period. As of July 10, the Shanghai Containerized Freight Index (SCFI) showed subtle first signs of rate stability as we saw small rate drops on both Transpacific and Far East trades after steeply climbing through May & June. |

| • |

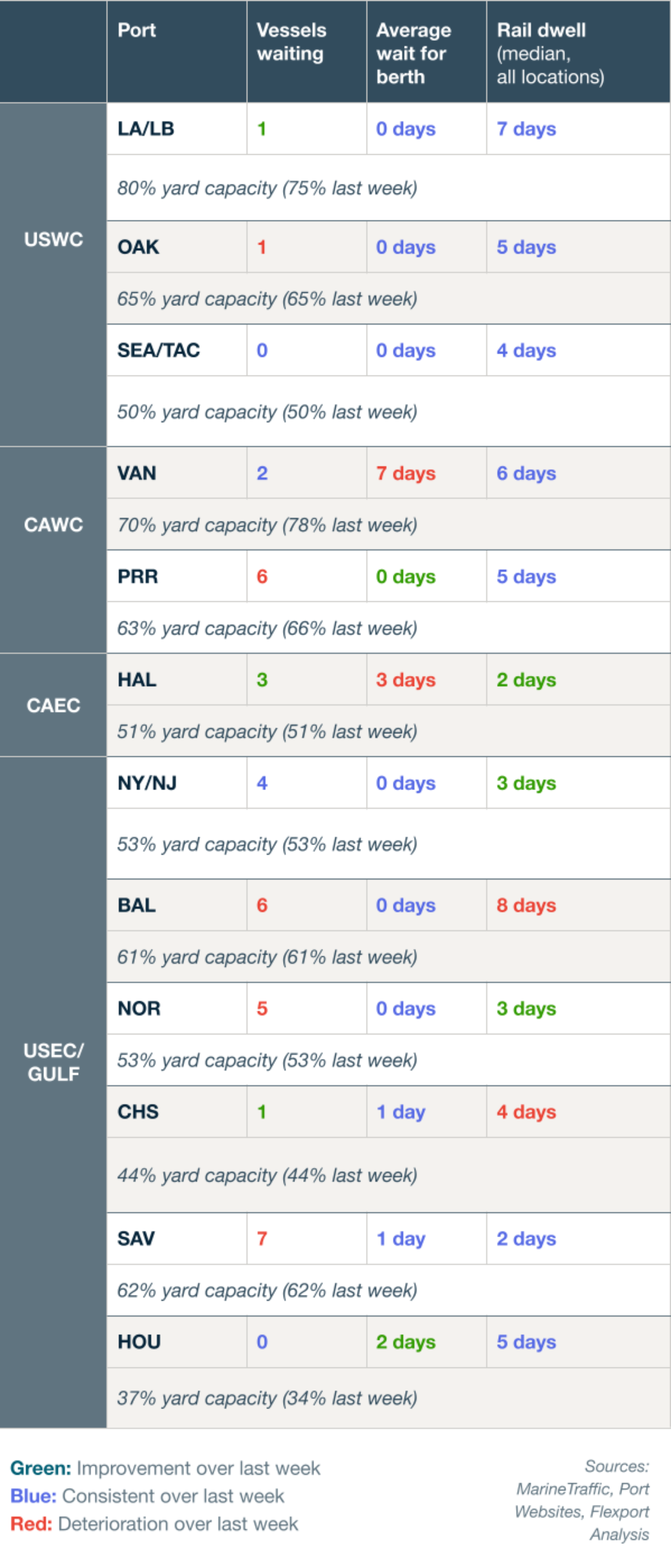

Port congestion has added to the pressure. Close to 11% of the global container fleet sat at anchor awaiting a berth in late June, the most since 2022. The Panama Canal reduced its maximum allowable draft to 49.5 feet effective July 1, ahead of an El Nino weather pattern expected to affect water levels later this year. |

TRANS-PACIFIC EASTBOUND (TPEB)

| • |

Blank sailings on this lane dropped to just 0.4% of scheduled capacity this week, down from 0.8% last week and well below the 5.0% seen two weeks ago. Carriers continue to prioritize Asia-Europe fleet deployment over the Pacific, as Middle East transit routes remain unavailable. West Coast capacity is expanding through extra loaders and additional services, while East Coast capacity holds steady. |

| • |

Retailers pulled imports forward ahead of new tariffs and possible fuel cost increases, pushing June import volume to an early but brief peak. Import forecasts call for a step down in volume later in summer and into early fall as consumer demand cools and inflation weighs on spending. |

| • |

The West Coast rate increase originally set for July 15 has been scaled back, as added capacity and steadying demand ease upward pressure. East Coast rates remain near previous highs, with only modest easing. |

| • |

Space is tight and rates are elevated, so secure capacity and equipment now for August and September cargo. |

| • |

Avoid locking into long allocations past September, since demand forecasts point to a shorter peak season than usual. |

FAR EAST WESTBOUND (FEWB)

| • |

Blank sailing activity held at 8.8% this week, down slightly from 9.4% the prior week, but still well above the other three lanes in this update. Elevated blanking reflects continued Cape of Good Hope routing tied to the Red Sea disruption. This lane absorbed more new vessel capacity over the past year than any other trade, as carriers added tonnage to cover the longer Cape routings. |

| • |

Underlying demand signals are steady, but the July 5 attack off Yemen has renewed uncertainty over Suez Canal transit, after some carriers had begun testing a return to that route. |

| • |

Rates on this lane have peaked and are beginning to stabilize at their current level. Moving into the coming week, demand will be the key factor driving the direction of the market. |

| • |

Plan for continued Cape of Good Hope transit times through the third quarter. Build extra schedule buffer into bookings, given industry reliability remains below pre-pandemic norms and Red Sea routing risk has increased again. |

TRANS-ATLANTIC WESTBOUND (TAWB)

| • |

Vessel utilization remains elevated across Northern Europe and West Mediterranean origins, exceeding 93%, with carriers holding 10-15% network capacity cuts via string removals, though blank sailings have paused since mid-May. |

| • |

No material shift in demand was identified this week. |

| • |

No lane-specific rate action was identified this week beyond the broader market increase. |

| • |

Critical container and chassis shortages persist across Germany, Benelux, Austria, Hungary, and Slovakia into Week 31. |

| • |

Capacity here remains the most stable of the four lanes. Continue standard booking practices — no near-term action is needed based on current trends. |

INDIAN SUBCONTINENT TO NORTH AMERICA (ISC)

| • |

With recent news of ONE concluding the WIN service, that means weekly direct services from Northwest India to the U.S. East Coast has been reduced from 6 on June 1st to 4 on August 1st. |

| • |

Maersk MECL service has announced it is returning to standard routing via Red Sea, Suez Canal. This service is the first on the ISC to USEC corridor to do so since Gulf War escalation began in March. |

| • |

Capacity remains constrained at levels not seen on the trade since Summer 2024, during frontloading for potential International Longshoreman’s Associate (ILA) labor action. |

| • |

The combination of reduced weekly capacity due to service changes, clusters of structural blanks, and port congestion has created backlogs of cargo at origin. |

| • |

India, ISC demand to global markets remains high, especially to the U.S. In the middle of a Peak Season as demand has steadily increased in June and July after a sharp increase of 40% from April to May. |

| • |

Peak season is expected to remain through August. |

| • |

U.S.-Iran ceasefire collapse re-introduces disruption risk while EU de minimis rule cuts Asia-Europe ecommerce volumes. |

| • |

Air freight demand contracted this week on both China-U.S. and China-Europe lanes, with ecommerce volumes leading the pullback. |

| • |

On China-U.S., Los Angeles and New York gateways saw the steepest rate declines with space broadly available; Chicago held firmer, supported by general cargo demand. |

| • |

On China-Europe, the EU’s new handling charge on low-value imports, which took effect July 1, has removed a material portion of parcel volumes. Industry analysts describe this as a policy-driven structural shift rather than a seasonal dip, with both ecommerce and general cargo demand now contracting simultaneously on this lane. |

| • |

Typhoon Bavi disrupted PVG operations July 10-13; the storm has since passed and operations have normalized. |

| • |

Trans-Pacific Eastbound (TPEB) demand fell week over week, driven by a shortfall in ecommerce cargo; rates edged lower in response. |

| • |

HKG-to-Europe tonnages dropped 12% week over week in the week of June 29 to July 5, pulling volumes back to late-March levels, following the EU de minimis change on July 1 (Source: WorldACD). |

| • |

Cathay Pacific announced a peak season program for North America destinations, effective August 9 through December 13. |

| • |

TPE suspended freighter operations July 10-13 due to Super Typhoon Bavi; flights have since resumed. |

| • |

Despite the temporary disruption, Taiwan-to-Europe tonnages rose approximately 20% over the past 3 weeks, driven by AI-related computer equipment shipments moving in volume to European markets. |

| • |

Some airlines now carry open capacity on Taiwan lanes; 5 to 7 days advance booking is sufficient to secure space. |

| • |

Demand softened compared to recent weeks and rates have begun to decline. |

| • |

Space availability has improved; 5 to 7 days advance booking is recommended to secure preferred flight options. |

| • |

Demand increased this week and rates remain at elevated levels relative to other Southeast Asian origins. |

| • |

Space is constrained; shippers should book 7 working days in advance. |

| • |

Demand softened overall, though rates have not moved proportionally; pricing is holding broadly steady, with room for negotiation depending on cargo type. |

| • |

Airlines report a slight softening in demand; space availability on TPEB lanes is expected to improve around July 16. |

| • |

Spot rates have not yet moved materially lower despite the easing of capacity pressure. |

| • |

Demand is softer and airlines report more open capacity as volumes from China and Hong Kong decline. |

| • |

Rates edged down slightly; 5 to 7 days advance booking is recommended. |

| • |

The market is well-balanced with no reported space constraints; a booking lead time of approximately 7 days is standard. |

| • |

Vessel processing backlogs at major U.S. ports are pushing shippers to air freight for time-sensitive India-to-U.S. cargo, keeping capacity on this lane tight. |

| • |

Booking 1 week in advance is recommended. |

| • |

Broader Indian subcontinent (Bangladesh, Sri Lanka, Pakistan): |

| • |

Sri Lanka: Carrier schedules have normalized following earlier disruptions. Middle East-based carriers are reporting space constraints due to rising perishable volumes. |

| • |

Bangladesh: The Europe lane is operating reliably with space available; the U.S. lane remains tighter, with space running short on some flights. |

| • |

Pakistan: The tightest market in the subcontinent. Capacity is fully committed across all lanes, with airlines quoting rate validity of 1 to 2 days only. Schedules remain reliable. |

| • |

Renewed U.S.-Iran fighting this week has put at risk the regional capacity recovery that had been underway since the initial conflict began. |

| • |

The MESA capacity deficit had narrowed to 10% below pre-war levels as of the week ending July 5, down from a 30% deficit in early June; this trajectory may reverse if hostilities intensify. |

| • |

Air France KLM Martinair resumed service to Dubai on July 8, currently operating 3 weekly flights with a plan to scale to daily. Riyadh and Tel Aviv service were restored earlier in the summer. Beirut remains suspended through July 21. |

| • |

Although jet fuel rates had begun to decrease since late April and airlines lowered their fuel surcharges in their latest round, renewed U.S.-Iran fighting in the first week of July reintroduced upward fuel price cycle. Any return to Hormuz closure would immediately affect a material share of global aviation fuel supply. |

(Source: Flexport)

Please reach out to your account representative for details on any impacts on your shipments.

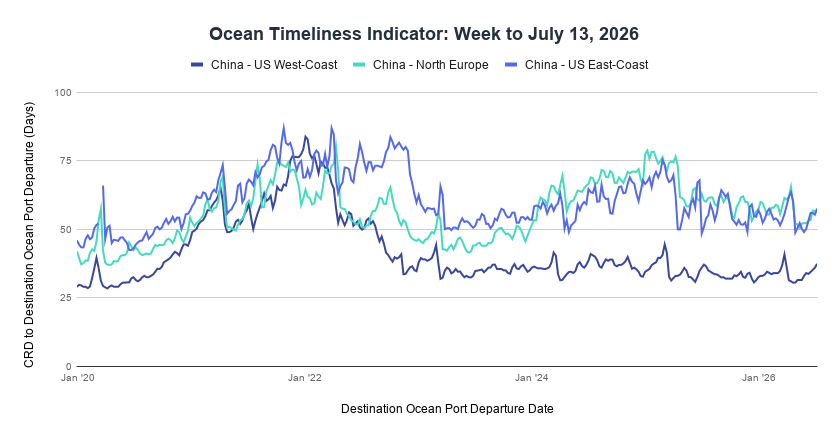

Week to July 13, 2026

Transit time from China to the US West-Coast increased by 1.4 days, rising from 36.0 to 37.4 days. The China to North Europe route saw a 1.5-day decrease, falling from 68.0 to 66.5 days.

Transit times from China to the US West-Coast experienced a modest increase, while the route from China to North Europe saw a notable reduction in transit time.

Thanks for tuning in. Catch you next week! Sign up here to get this newsletter in your inbox. Stay in the loop—read past newsletters here. For more information, connect with one of our logistics experts here.

| Follow us for more updates: |

|

|

©2026 Flexport, Inc. – All Rights Reserved. 100 California Street, FL 5, San Francisco, CA 94111.

This email was sent to your address because you’re opted into Flexport’s Global Logistics Updates. Want to change what communication you receive? You may update your email preferences or unsubscribe below.

|