McKinsey forecasts $230B robotaxi market by 2035 as costs plunge

|

|

|

Editor’s note: This week, I moderated a panel on trucking autonomy at the Ride AI 2026 event in San Francisco. Here are three summaries of my notes from a few of the sessions. Expect feature articles in the coming weeks after I clean up my transcripts.

|

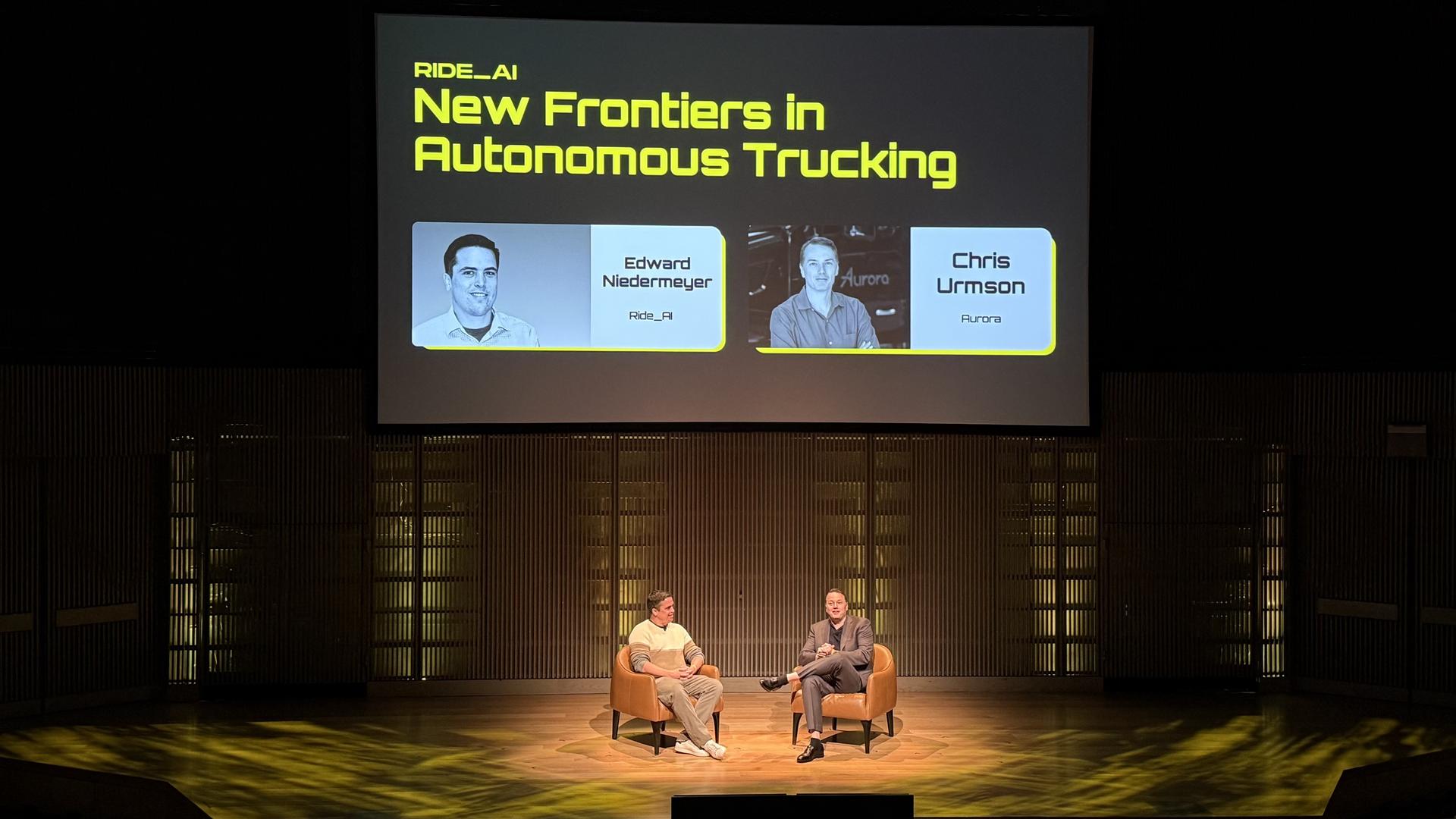

Aurora moves autonomous trucks from tech demos to commercial reality

|

(Photo: Thomas Wasson/FreightWaves)

|

Aurora Innovation is moving past the Gartner hype cycle that has defined autonomous vehicle development for the past decade. The company told attendees at Ride AI it’s deep in the grind of turning its cutting-edge technology into a product that delivers real customer value.

Aurora CEO Chris Urmson told Ride AI’s Ed Niedermeyer the technology works. It’s now about how to manufacture and scale it. Urmson emphasized the importance of moving past demonstrations and getting real customers with real feedback to improve operations.

The economic case is straightforward. Trucking operates as a pure total-cost-of-ownership business, and Urmson sees autonomous technology hitting several cost levers simultaneously: collision and injury rate reductions that drive down insurance premiums, fuel savings of 14% to 30% and doubled asset utilization on $200,000 tractors that currently sit idle half the time.

Aurora logged 250,000 driverless miles as of January 2026 and plans to scale from a handful of trucks to hundreds across the Sunbelt by year’s end. In one example, at 200 trucks, the company projects roughly 1 million miles weekly. Similarly, manufacturing can eventually ramp toward 20 trucks per week.

Regulatory barriers remain. California’s 2011 rules split autonomous vehicle regulations at 10,000 pounds. This explains why robotaxis roam Golden State streets while heavy-duty trucks cannot. The California Department of Motor Vehicles is now working on rulemaking for heavier vehicles, with new rules expected within the next month.

Urmson noted automation will be as transformative to the economy as the internal combustion engine was 100 years ago. He placed less focus on timelines and more on trust. “If it takes another quarter that’s fine, you have to build trust, gotta get it right,” said Urmson.

|

McKinsey forecasts $230B robotaxi market by 2035 as costs plunge

|

(Photo: Thomas Wasson/FreightWaves)

|

The autonomous vehicle industry is shifting from a building problem to a deployment and scaling challenge, with major implications for fleet operations and supply chain infrastructure, according to new data from the McKinsey Center for Future Mobility.

In its recently released report, consumer sentiment is turning a corner. Safety concerns as a primary barrier dropped to 38% of U.S. consumers, down from 53% in 2024. Meanwhile, robotaxi costs are expected to plunge 78% by 2035, creating economic pressure on personal vehicle ownership that fleet operators should watch closely.

The math also paints an interesting usage picture: For drivers logging under 7,500 miles annually, robotaxis become the cheaper option. For roughly 80% of the population driving under 13,500 miles, roboshuttles make economic sense. In large cities, about 50% of residents may find ownership no longer pencils out.

The ripple effects extend well beyond passenger mobility. Insurance markets would shift from personal products to commercial fleet coverage with fundamentally different risk profiles. Traditional repair shops would consolidate into specialized repair hubs where uptime — not oil changes — drives the business model.

Regulation remains the primary bottleneck. The market is currently supply-constrained, with deployed fleets unable to meet consumer demand due to city-level restrictions. Once those barriers fall, McKinsey expects rapid expansion to 40-plus cities covering most urban areas of more than 500,000 inhabitants. In one scenario the industry will likely consolidate from 10 to 15 players down to three to five major providers.

|

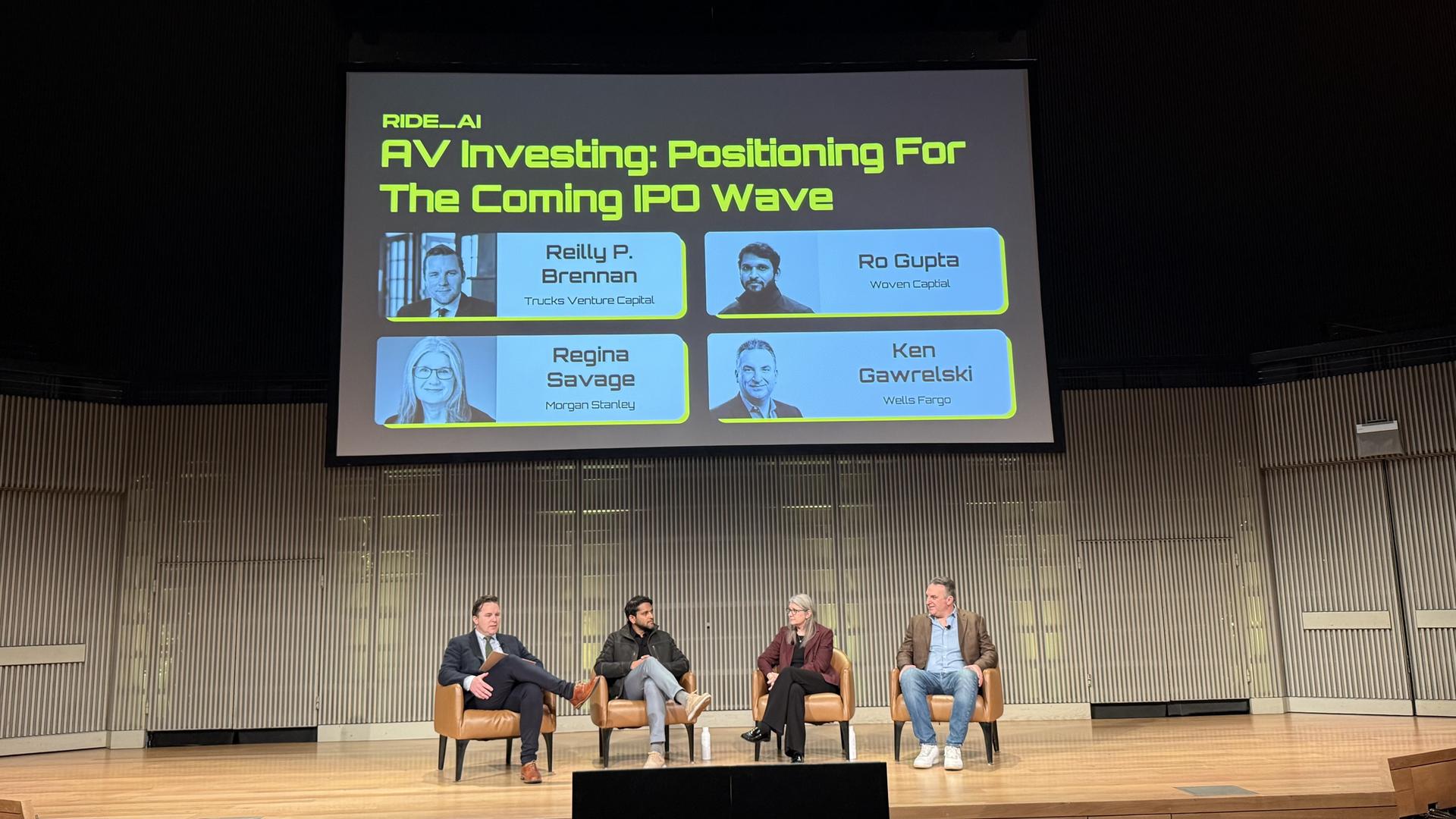

Investors eye next wave of autonomous vehicle deals after SPAC bust

|

(Photo: Thomas Wasson/FreightWaves)

|

The autonomous vehicle investment landscape looks dramatically different from how it did four years ago. The 2020-2022 SPAC boom left five to six pure-play autonomy companies diminished or exited entirely, pushing most AV developers outside Tesla into private markets. Now, with public perception shifting thanks largely to Waymo’s visible success, investors are eyeing a new wave of opportunities — but with far more scrutiny.

The timeline for Level 4 autonomy feels closer than ever. “It feels like we’re two to three years out on L4 but it’s getting closer for public investors to underwrite,” one panelist noted during a fireside chat at the Ride AI event.

The IPO process has fundamentally changed. Companies must now engage sophisticated investors far earlier through “testing the waters” approaches, proving survival and scaling capabilities before seeking public capital. The days of fear-of-missing-out investing are also over.

Investors are willing to pay higher entry prices if the derisking is done well.

Unit economics remains the critical gatekeeper. Uber averages $22 per ride but earns just $3, while Waymo is estimated to break even or lose about a dollar per trip. Chinese manufacturers are showing the path forward. One analyst points to $75,000 as the “Goldilocks” all-in vehicle cost to make the business model work.

For OEMs, strategies are diverging sharply. Large manufacturers view AV as a standard vehicle feature rather than a proprietary network play, while smaller players lacking capital are betting on partnerships as the technology commoditizes. The benchmark for market viability? Several hundred vehicles deployed with proven ability to scale.

|

|

|

IN PARTNERSHIP WITH ACT EXPO

|

Connected vehicles, ADAS safety tech, autonomous advancements and software-defined vehicles drive innovation. Learn More.

|

|

|

Ascend Elements filed for Chapter 11 bankruptcy on April 10, a blow to investors who had sunk nearly $900 million into the battery recycler. The Trump administration canceled a $316 million grant for its Kentucky facility, and the softening EV market compounded financial pressures. (TechCrunch)

San Francisco International Airport approved Waymo for pickups and drop-offs in January 2026 but confined it to the Rental Car Center — a 10-minute AirTrain detour from terminals. Uber and Lyft retain exclusive access to the main Domestic Garage. Garry Tan writes in his Substack there’s no safety rationale. Instead it’s pure incumbent protection. (Garry’s List)

California Air Resources Board has begun enforcing dormant transport refrigerated unit regulations without formal announcement, pressuring warehouses to verify TRU compliance. Non-compliance carries fines reaching $10,000 per day. All TRU owners, including those outside California, must register and obtain CARB Identification Numbers. (FreightWaves)

Aurora Operations is seeking a five-year exemption from the Federal Motor Carrier Safety Administration (FMCSA) to use cab-mounted warning beacons instead of reflective triangles on its Level 4 autonomous trucks. The company plans to expand from 109 to 200 trucks by year’s end. Comments are due May 15. (Landline)

|

As always, thanks for watching and reading.

Thomas Wasson

twasson@firecrown.com

|

|

|

|