In this edition: Breaking down the Convoy sale to DAT and the rail merger of the century.

|

|

|

In a striking move, digital freight forwarder Flexport has sold the core Convoy technology platform it acquired in late 2023 to DAT Freight & Analytics for approximately $250 million, less than two years after buying it for roughly $16 million . The transaction marks a dramatic return on a modest investment and highlights shifting strategic priorities within the logistics sector.

When Flexport originally acquired Convoy’s assets following the Seattle‑based brokerage’s collapse, the goal was preservation: to rescue the underlying technology and relaunch it as a neutral digital execution layer for shippers, brokers, and carriers . Over the subsequent 18 months, the platform was rebuilt, onboarding tens of thousands of carriers, reengaging brokers, and demonstrating its value as a broadly accessible freight execution infrastructure.

John Kingston wrote in his FreightWaves article, “What we realized is that a neutral platform is not neutral,” Ryan Petersen, CEO of Flexport said. “We have a brokerage. We’re a massive freight forwarding company.” The combination, he said, raised questions in the industry about whether the Convoy platform truly could be seen as neutral.

For DAT, the acquisition expands its offerings beyond its signature load board. It will join DAT’s recent acquisitions, including visibility provider Trucker Tools and payment startup Outgo, to give users an expanded suite of tools. DAT is offering the Convoy platform with zero upfront cost; users pay only transactional fees, lowering barriers to adoption and likely prompting demand to outpace onboarding capacity

Flexport, for its part, will continue to operate its residual digital brokerage business, which processes roughly 100,000 loads annually (98% mechanically executed). It remains DAT’s largest customer on the platform from day one, underpinning a continued commercial link between the two firms.

|

|

|

SONAR TRAC Market Dashboard

|

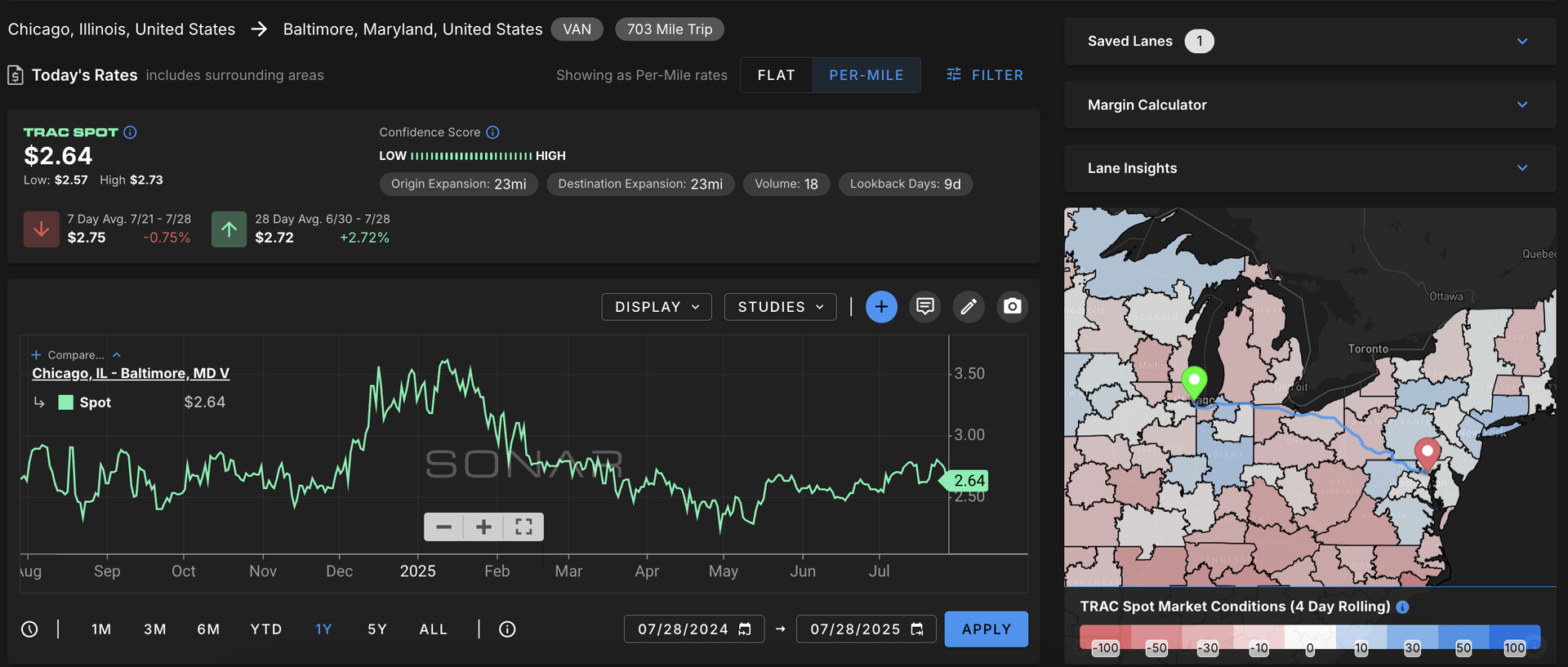

TRAC Tuesday. The lane from Chicago to Baltimore is a 703-mile jaunt averaging about $2.64 a mile and falling. Capacity is loosening in both markets as outbound tender rejections drop 0.96% week over week in Chicago and 0.8% in Baltimore. The excess capacity is compounded by falling outbound tender volumes, falling 6.3% in Chicago and 1.2% in Baltimore.

With capacity readily available in both markets, contract carrier compliance will be strong, while spot rates continue to drop, making outbound Chicago loads heading East less of a priority when it comes to coverage. Primary carriers will see strong volumes on routing guides, while secondary carriers will continue to hit the spot market or aim for the top spot on routing guides when possible.

|

|

|

Who’s with whom? Union Pacific and Norfolk Southern may be on the verge of creating the first true coast-to-coast freight rail network in the United States. The two rail giants are in advanced merger discussions, with a formal deal potentially announced as early as next week. The transaction, if completed, would represent one of the most significant consolidations in U.S. rail history, combining Union Pacific’s western operations with Norfolk Southern’s extensive 19,500-mile network in the eastern U.S.

The proposed merger would result in a company with a combined market value approaching $200 billion. It’s suggested Norfolk Southern could be acquired at around $320 per share, valuing the company’s equity near $72 billion. The move is being framed as a strategic effort to streamline freight operations by eliminating key interchange points, particularly in congested hubs like Chicago, and improving transit times across long-haul corridors.

Proponents of the merger argue it could unlock major operational efficiencies, reduce costs, and potentially attract more freight business from the highway to the rails. By creating a seamless east-west rail service, the combined company would be able to offer shippers more reliable service and better pricing leverage in an increasingly competitive logistics environment.

However, the deal is likely to face significant regulatory scrutiny. Any agreement would require approval from the Surface Transportation Board (STB), which oversees major railroad mergers and is expected to take up to 22 months to complete its review. Under current STB rules, Class I rail mergers must be shown to enhance, not harm, competition and serve the broader public interest.

Critics, including other major Class I railroads, shipping groups, and labor organizations, are expected to push back strongly. Concerns range from diminished competition and potential price increases to job cuts and disruption to regional short-line operations. A merger of this magnitude would reduce the number of major U.S. freight railroads from six to five, raising alarms among those already wary of rail consolidation.

|

|

|

Catch up on last week’s episode

|

|

|

See you on the internet,

Mary O’Connell

@MaryO_119

|

|

|

|