June data shows a trucking market struggling with tariff effects and overcapacity

|

|

|

For-Hire Trucking Index shows fourth month of volume declines

|

The for-hire trucking industry faced its fourth consecutive month of declining volumes in June, according to ACT Research’s For-Hire Trucking Index. The diffusion index is based on a survey of carriers and measures the degree and direction of changes in their operational statistics. A reading above 50 shows growth; below 50 is degradation.

The Volume Index posted a seasonally adjusted 41.5 in June, down from 42.5 in May. This downturn stems from tariff-related effects, particularly the early April tariffs and persistent overcapacity, extending the current freight market downcycle.

Volumes are expected to improve, with the release noting, “Volumes should improve in July and August following the tariff reprieve, but the pull-forwards in freight demand in the first half of the year will result in paybacks.”

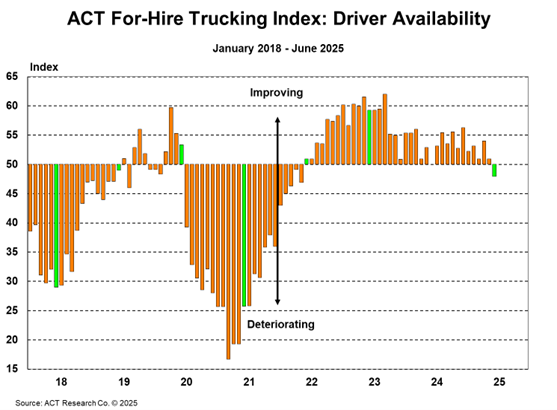

Particularly noteworthy is the Driver Availability Index, which tightened to 47.9 from 50.9, the first deterioration in driver supply in 38 months. “Given the duration of the downturn, current uncertainty, and a weaker freight outlook due to tariffs, we would expect the driver market to continue to tighten in the near term,” the report notes. “While a tighter driver supply is a potential catalyst for a new cycle, demand is needed too.”

Other causes of tightening driver availability include cost-cutting measures, which are beginning to take drivers and driving schools out of the market.

Fleet purchase intentions rose 15.6% month over month in June, with 43% of respondents planning equipment purchases in the next three months. However, this remains significantly below the 54% long-term average as fleets deal with financial constraints and rising equipment costs.

The report adds, “Overall, buying sentiment is expected to remain below the long-term average as we enter the 13th quarter of a for-hire downturn, compared to the six- to eight-quarter historical average. Fleets are cash-strapped, and many are delaying or forgoing new equipment purchases altogether.”

The Pricing Index fell 3.6 points to 44.2 in June from 47.8 in May. The persistent overcapacity remains evident in soft spot trends during typically strong seasonal months. While volumes should improve following the tariff reprieve, multiple pull-forwards in freight demand earlier in the year will likely result in payback periods.

The Capacity Index increased slightly to 46.8 in June, up 0.4 points from May, but capacity continued to decline overall as publicly traded TL carriers’ profit margins remain near their lowest levels since 2009.

The Productivity Index showed a substantial 16.3-point decrease to 47.6 in June, as the loosening capacity returned following May’s temporary tightness during Roadcheck week.

With tariff impacts expected to weigh on volumes through 2025, recovery prospects remain limited despite ongoing capacity attrition.

|

|

|

Averitt Express announces largest regional driver pay hike in company history

|

(Photo: Noi Mahoney/FreightWaves)

|

Averitt Express recently announced a significant pay increase for its regional drivers with hazmat endorsement, raising rates from 60 cents to 64 cents per mile in what the company calls the largest such increase in its 54-year history.

FreightWaves’ John Kingston writes the announcement stands out in an industry where pay increase announcements have become rare compared to the flurry of wage hikes during the post-pandemic freight boom.

The LTL carrier’s move affects multiple driver categories, including regional drivers without hazmat endorsement, who now earn 54.5 cents per mile. According to an Averitt spokeswoman, pay increases for LTL associates, including pickup and delivery drivers, shuttle drivers, and dock associates, were “significant but not as historic as the increases for our regional drivers.”

“More fleets are reporting pay increases in our surveys this year than last year, and those increases are a little more ambitious,” said Leah Shaver, president of the National Transportation Institute, in comments to FreightWaves. “The data does not point to any type of inflationary cycle, but we are seeing upward movement in the rate of growth and have seen that since last summer.”

These wage increases are occurring despite poor freight market conditions, with spot linehaul rates lower than at the start of the year according to SONAR data. The American Transportation Research Institute reports that driver wage gains averaged just 2.4% last year, compared to 10.8% in 2021 and 15.5% in 2022.

Meanwhile, Bureau of Labor Statistics data shows steady gains in the truck transportation sector, with hourly wages for non-supervisory and production employees reaching an all-time high of $31.11 in May 2025, up from $29.88 in October 2024.

In addition to the pay increase, Averitt highlighted other compensation benefits, including a profit-sharing plan that directs 20% of company profits into employee 401(k) plans, along with health insurance, company-provided life insurance, holiday pay after 30 days, and paid time off after 90 days.

|

|

|

Werner reports strong Q2 earnings buoyed by used equipment sales

|

(Chart: John Kingston/FreightWaves)

|

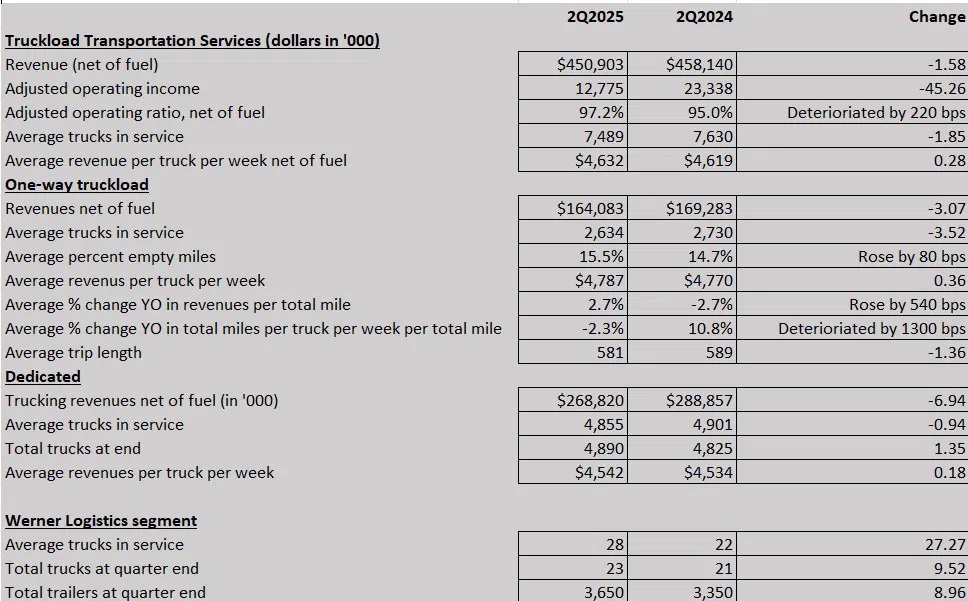

Werner Enterprises posted multiple sequential improvements in Q2 2025, with used equipment sales standing out. The truckload carrier reported $5.9 million in gains on sales of property and equipment in Q2, more than doubling the $2.7 million recorded in the same period last year.

“Used truck and trailer values have accelerated since March, benefiting from tariff and other macro uncertainty,” CEO and chairman Derek Leathers said during the company’s earnings call. FreightWaves’ John Kingston wrote that the carrier achieved these gains despite selling 54% fewer tractors and 60% fewer trailers compared to previous periods, with profits rising due to significantly higher unit prices.

The company’s logistics segment also saw growth, with Q2 operating income surging to $4.3 million from just $550,000 a year earlier. This performance was boosted by a 7% year-over-year load growth resulting from successful new business acquisition.

“We generated solid results during the second quarter and are encouraged by the sequential improvement in financial performance relative to Q1,” Leathers noted. He also highlighted the company’s adjusted operating margin improvement from negative 0.3% in Q1 to 2.2% in Q2.

Werner’s quarterly results also benefited from a favorable Texas Supreme Court decision that reversed a $90 million jury award from a 2018 case. “This ruling led to the reversal of a $45.7 million net liability, including interest and benefiting GAAP operating income,” explained executive vice president, treasurer and chief financial officer Chris Wikoff.

Looking ahead, Werner executives expressed confidence in continued sequential improvement in Q3, driven primarily by new customer additions in the company’s dedicated division, which represents approximately 65% of the revenue in its combined truckload transportation services sector.

English language proficiency also made an appearance, with Kingston noting that Leathers doesn’t see any impact on Werner’s fleet from enforcement. “We’ve always kept our English language proficiency test in place throughout the time that the rule wasn’t being enforced,” Leathers said.

|

|

|

SONAR spotlight: Tender rejection rates take a Summer vacation

|

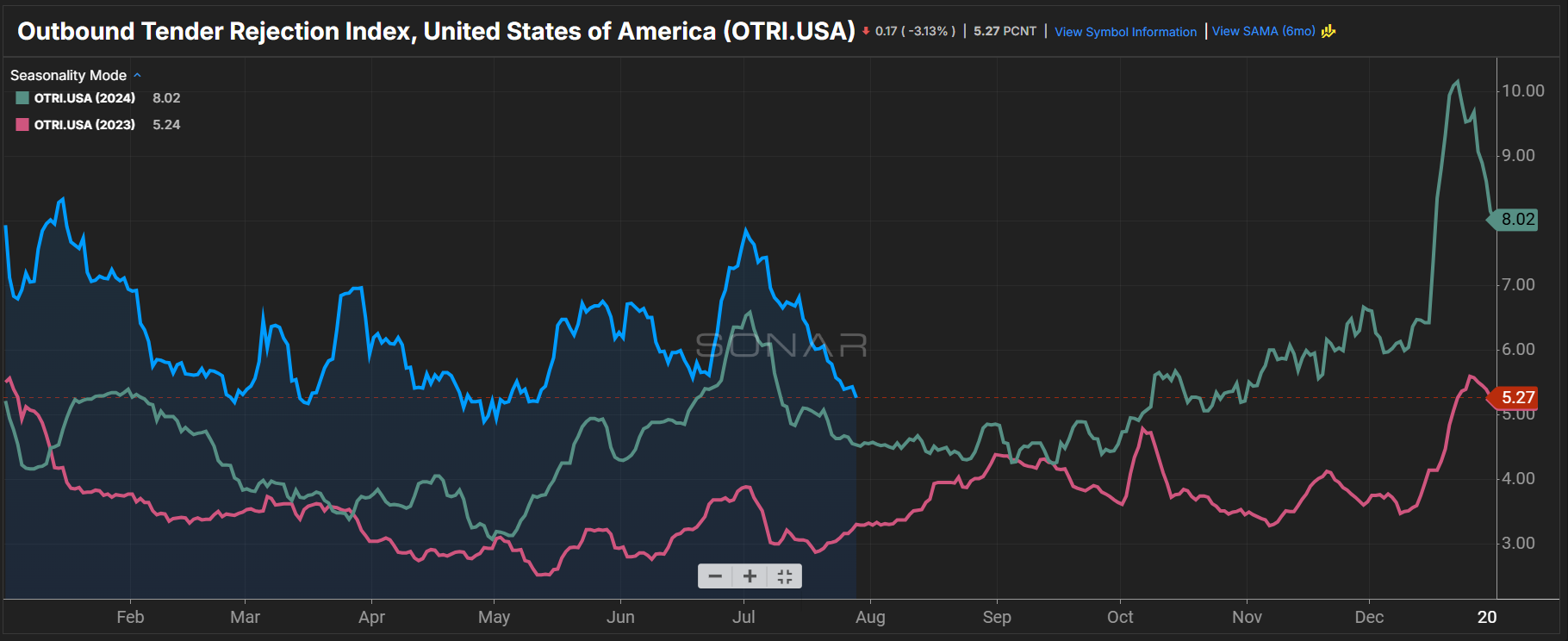

Summary: A holiday boom gave way to a seasonal bust in nationwide outbound tender rejection rates as the last week of July heralded a return to the summer freight doldrums of August. OTRI fell 57 basis points in the past week from 5.84% on July 21 to 5.27%. While the rate of decline lessened compared to previous weeks, bottoming out remains elusive. Compared to last year, OTRI remains 75 bps higher than 4.52% on July 29, 2024.

Breaking down by segment, the dry van segment fell 66 bps week over week from 5.80% to 5.14%. Reefer remains volatile but in a more favorable pricing power position. ROTRI fell 50 bps week over week from 10.68% to 10.18% and is 254 bps higher year over year than 7.64%. Flatbed was the only mode that posted a gain, up 215 bps week over week from 11.77% to 13.92%. Despite concerns over homebuilding and its impact on open deck freight, compared to last year, FOTRI is 817 bps higher than 5.75% on July 29, 2024.

Looking ahead, next week is projected to see nationwide outbound tender rejection rates level out when looking at a two-year seasonally adjusted moving average. OTRI is forecast to bottom out around 5.28% before reaching 6% by the end of August. The next time OTRI will clear 7% is predicted to be the middle of December.

Another development to watch will be if there is a bifurcation between the contract and spot markets. Despite ongoing declines in spot rates in the flatbed and reefer segments, their outbound tender rejection rates remain at or above 10%, a positive sign compared to the larger and more commoditized dry van segment. Overcapacity in the spot market remains, while contracted capacity continues to decline based on recent second-quarter earnings calls, which saw many large fleets continue to shrink their tractor count in response to higher costs and poor rates.

|

|

|

Routing Guide: Links from around the web

|

|

|

DALLAS, TX | SEPTEMBER 10, 2025

|

|

|

CHATTANOOGA, TN | OCTOBER 21-22, 2025

|

|

|

FWTV EVENT | DECEMBER 10, 2025

|

|

|

Like the content? Subscribe to the Newsletter!

|

|

|

Loaded and Rolling Podcast links:

|

|

|

Download the FreightWaves App

|

|

|

|