Operating margins fall below 2% while non-fuel costs reach record highs

|

|

|

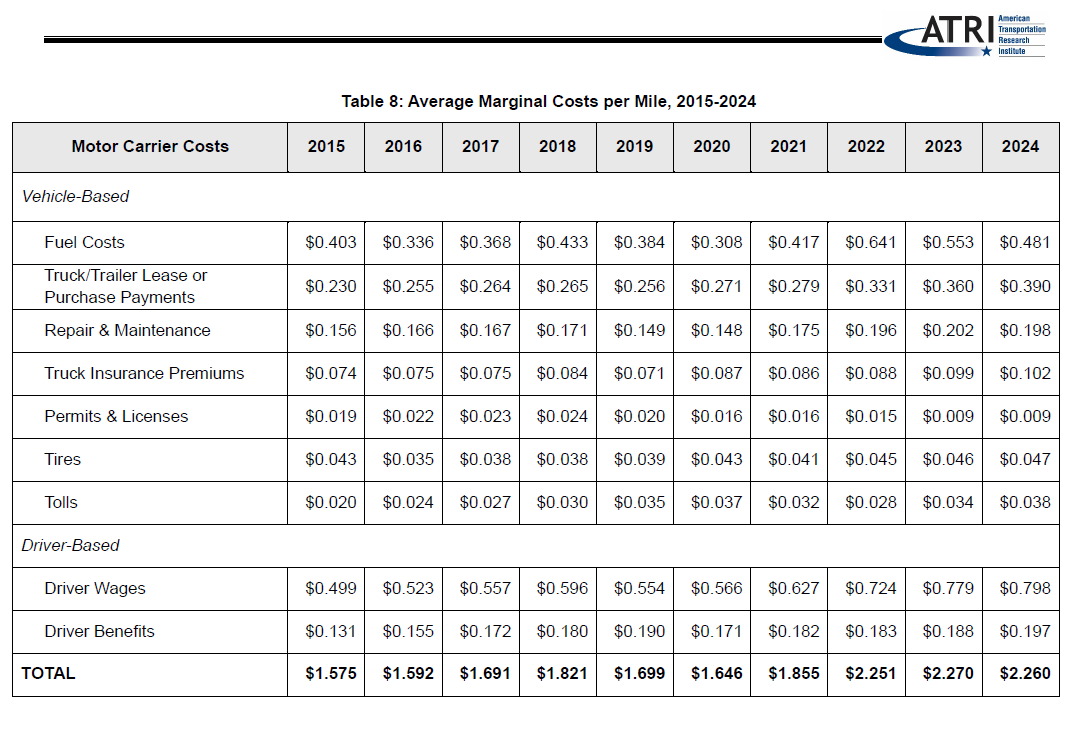

ATRI report: Rising costs continue to squeeze trucking industry

|

Rising costs collided with depressed freight rates, according to ATRI’s latest operational costs of trucking benchmarking report. According to the data, the industry’s average cost of operating a truck declined slightly by 0.4% to $2.260 per mile. That’s good news but the freight devil lies in the details. When removing lower fuel costs, marginal costs increased 3.6% to $1.779, the highest costs ever recorded by ATRI for non-fuel operating costs.

The report showed truckload carriers were hit hardest in operating margin (OR), operating at an average OR of -2.3% in 2024 compared to 3% in 2023 and 8% OR in 2022. Other modes saw operating margins continue to deteriorate, most sectors struggled with margins below 2%. Only the LTL sector maintained positive profitability at 11.6% OR. Reefer carriers fell from 6% OR in 2022, to 2% in 2023 before settling at barely above breakeven at 0.1%. Flatbed / Oversized saw a similar trend, OR fell from 7% in 2022 to 5% in 2023, then 0.4% for 2024.

“The trucking industry is facing the most challenging freight market in years, with loads down and costs increasing,” said Groendyke Transport, Inc. President and CEO Greg Hodgen in a press release.

Several cost categories saw increases, with truck and trailer payments rising 8.3% to a record-high $0.390 per mile, and driver benefits costs increasing 4.8% to $0.197 per mile. Driver wages, traditionally the largest contributor to cost increases following the pandemic, rose more modestly at 2.4%, slightly below the inflation rate.

The report saw numerous other operational adjustments made by carriers to weather the freight recession. Truck capacity dropped 2.2% as companies sold vehicles, empty miles increased to an average of 16.7%, and the drivers-per-truck ratio fell to 0.93 as carriers parked equipment. Many fleets also reduced non-driver staff by 6.8% as a cost-management strategy.

Despite these challenges, there were some positive trends. Average truck age, dwell time per stop, and mileage between breakdowns all improved. Regarding dwell, the report notes, “Overall average dwell time decreased slightly in 2024, by 2 minutes, to 1 hour and 38 minutes per stop – just 22 minutes below the industry-standard threshold for excessive driver detention. The source of this improvement, however, was limited exclusively to the truckload sector.”

|

|

|

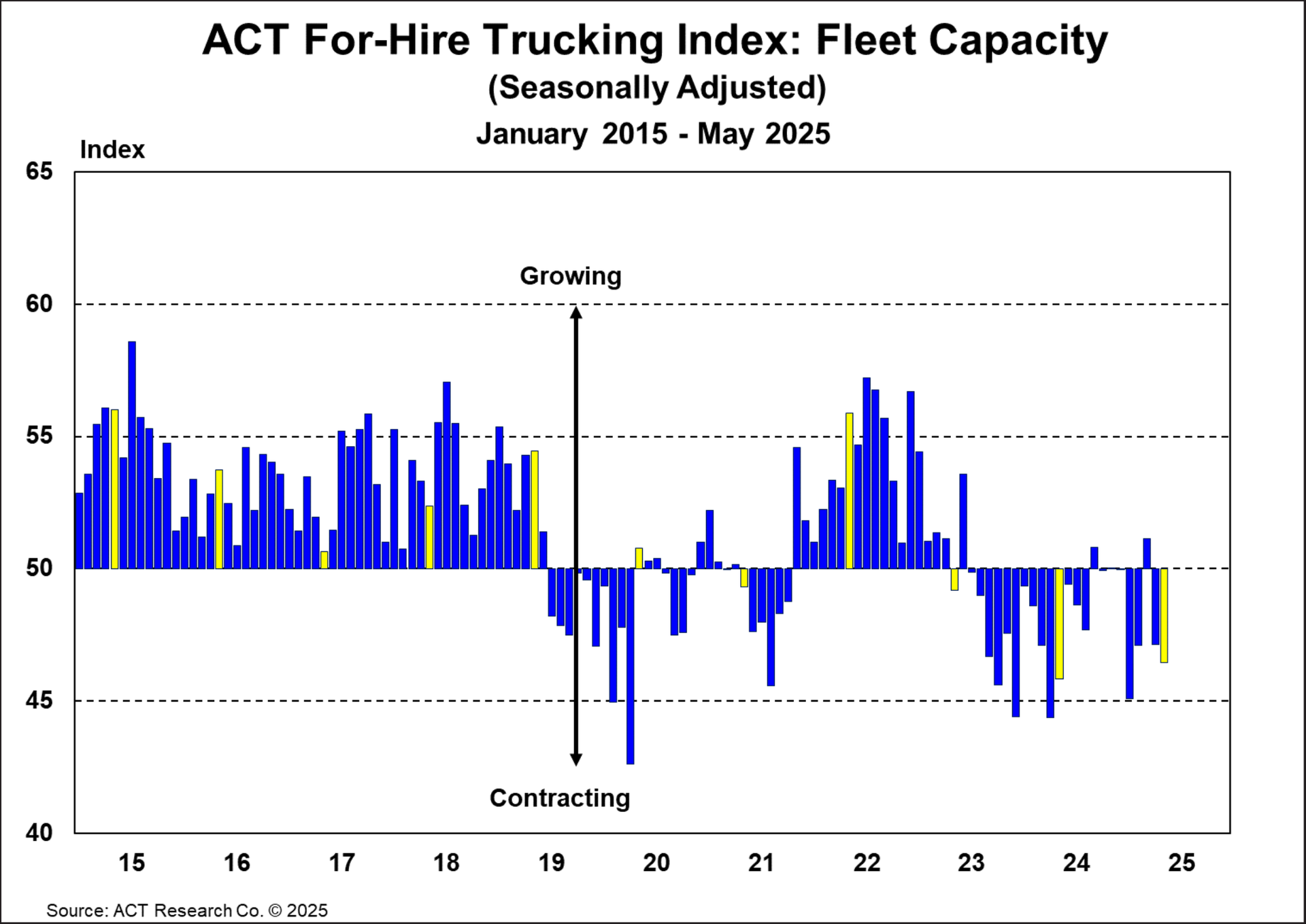

June For-Hire Trucking Index shows volume weakness amid capacity contraction

|

ACT Research recently released its June For-Hire Trucking Index, which showed continued deterioration in freight volumes alongside decreasing capacity. The diffusion index is based on a survey of carriers. A reading above 50 shows growth, while anything below 50 is degradation. The Volume Index saw its third consecutive month of softening, falling to 42.5 points (seasonally adjusted) in May, from 43.4 points in April.

“The myriad impacts of tariffs and opaqueness regarding future trade decisions have destroyed business planning and slowed economic activity,” according to ACT Research. “While we may see some improvement in trade volumes ahead of the August 9th China trade decision, the pull-forward of freight into Q1 has necessitated a payback later this year.”

In spite of sustained driver availability, fleets continue to struggle with profitability. The Driver Availability Index tightened 3.1 points in May to 50.9 points, the 37th consecutive month at or above 50. The report adds, “Struggling owner-operators turning in their operating authorities have also provided a steady supply of experienced drivers for fleets. But after three years of weak rates/profitability, investments in driver training are under pressure. Roadcheck may have contributed to the still positive, but lower level of driver availability in May too.”

The Capacity Index decreased to 46.4 in May from 47.1 in April, as carriers reduced their fleet tractor counts. Fleet purchase intentions remained significantly below historical norms, with only 27% of respondents planning to buy new equipment in the next three months, compared to the 54% long-term average. ACT describes fleet reluctance as “generationally weak profits, economic uncertainty, and regulatory uncertainty.”

The Pricing Index showed some improvement, rising 8.4 points to 47.8 in May from 39.4 in April, though this was largely attributed to the temporary tightening effect of the annual Roadcheck inspection event rather than fundamental market improvements.

Private versus for-hire fleet dynamics remain a factor to watch. The report adds, “The supply-side should contract as private fleets decelerate fleet growth and for-hire fleets remain on the sidelines. Rising equipment costs due to tariffs further that case, but the flip side to tariffs is slower freight market growth, which will prolong the recovery in the for-hire sector.”

|

|

|

Werner Enterprises Wins Texas Supreme Court Reversal of $100 Million Nuclear Verdict

|

(Photo: Jim Allen/FreightWaves)

|

The Texas Supreme Court overturned last week a $100 million verdict against Werner Enterprises. The ruling reverses a 2018 jury decision that held Werner responsible for a fatal accident that occurred during hazardous winter weather conditions near Odessa, Texas.

The case stemmed from a 2014 crash when a pickup truck driven by Trey Salinas lost control on icy roads, crossed a 42-foot median on Interstate 20, and collided with a Werner truck driven by Shiraz Ali. The collision killed a seven-year-old child, left another child quadriplegic, and caused serious injuries to two other passengers in the pickup.

In its decision, the court determined that Ali’s actions were not the proximate cause of the accident. Chief Justice Blacklock wrote that “the sole proximate cause of this accident and these injuries was the sudden, unexpected hurtling of the victims’ vehicle into oncoming highway traffic, for which the defendants bore no responsibility.”

FreightWaves John Kinston notes that the court distinguished between “but-for” causation and “substantial-factor” causation, ruling that while Ali’s presence on the highway was a “but-for” cause, it was not a substantial factor in causing the harm.

“After seven years navigating the appellate process, we are thankful the Texas Supreme Court reached the same conclusion as law enforcement – that the Werner drivers and our company did nothing wrong,” said Nathan Meisgeier, Werner president and chief legal officer, in a prepared statement.

Bank of America Merrill Lynch transportation research analysts described the decision as “good for Werner, good for trucking,” noting that “this is an important win for Werner and the trucking/broader transportation industry.” The analysts also observed that the 2018 initial verdict “began to set a trend of truck company exposure to landmark verdicts that continues to loom over the industry.”

Following the legal victory, Werner acknowledged the tragedy faced by the victims. “We have not and will not lose sight of the tragic loss the Blake family suffered because of this accident. Our continued thoughts and prayers are with the Blake family,” Meisgeier stated.

Regarding the impact of the reversal on Werner’s balance sheet, Kingston writes, “While there will be an outward impact on the company’s balance sheet from the end of the litigation that went back more than seven years, the financial steps to be taken will simply just reverse charges and credits already made by the company previously in anticipation of a large payout.”

|

|

|

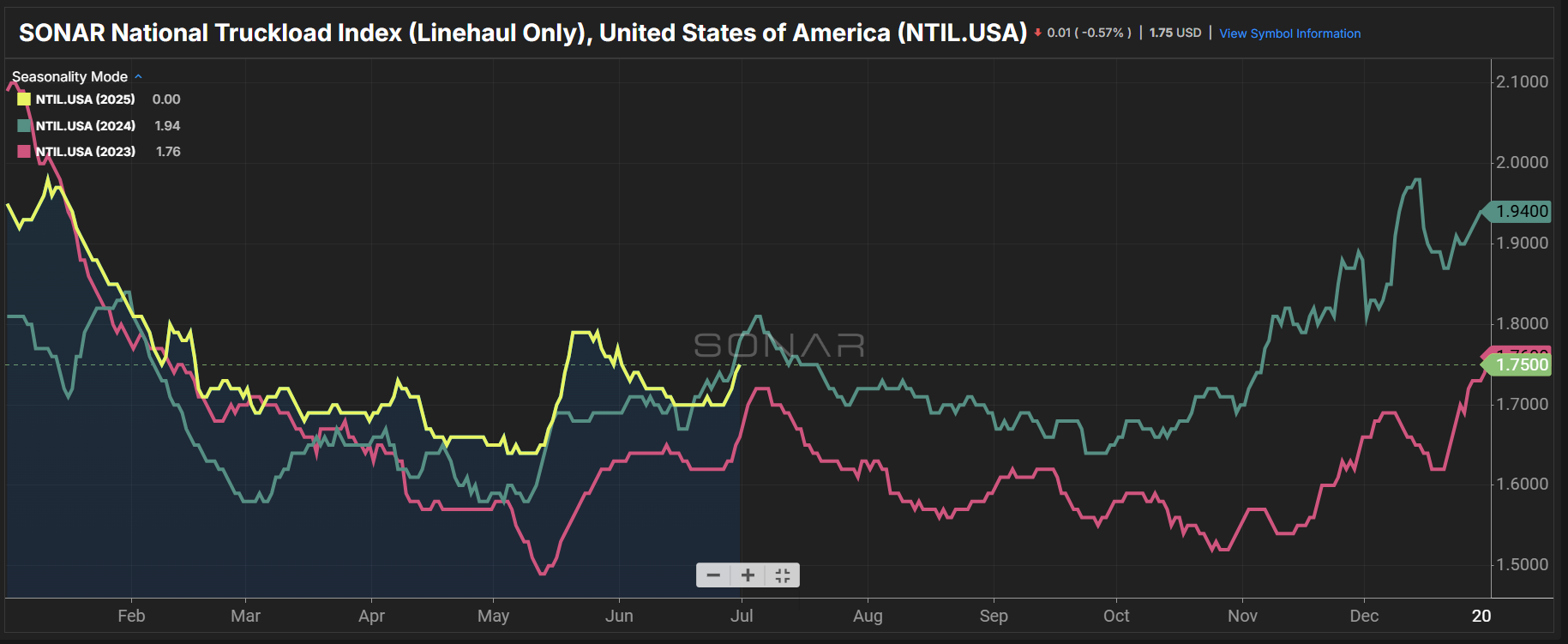

SONAR spotlight: Spot market linehaul rate’s seasonal rate rally continues

|

Summary: A seasonal rally in dry van spot market linehaul rates continues leading up to the Fourth of July, according to the SONAR National Truckload Index (Linehaul Only). NTIL rose 5 cents per mile in the past week from $1.70 on June 23 to $1.75 per mile. Linehaul rates are now at the same level as last month, where the NTIL was at $1.70 on June 1. Fuel costs are based on the average retail price of diesel fuel and fuel efficiency of 6.5 miles per gallon. The formula is NTID – (DTS.USA/6.5).

Compared to the last two years, linehaul rates have more ground to gain, leading up to July 4. One reason being is NTIL having risen more during the Memorial Day weekend than previous years.

Looking upstream to contract rates shows a more favorable pricing power environment for truckload carriers. Dry van outbound tender rejection rates remain elevated based on y/y comps. VOTRI at 7.61% is 116 basis points higher than 2024, where van outbound tender rejection rates were at 6.45%. When looking at now compared to 2023, VOTRI is 386 bps higher versus 3.75%.

One question that remains following the Fourth of July holiday is the impact of English Language Proficiency enforcement. While it’s too early to tell what the numbers will be following its rollout on June 25th, Avery Vise, vice president of trucking at FTR Transportation Intelligence gave some numbers regarding the last time ELP rules placed truckers out of service using data from 2013 to 2014.

Vise wrote in May, “CVSA noted when it dropped ELP as an OOS violation that 83,000 ELP violations were cited in 2013, of which 3,700 were OOS violations. FTR identified nearly 100,700 ELP violations in 2014 – the final year before CVSA dropped ELP as an OOS violation. Of those violations, more than 3,900 were OOS violations.”

|

|

|

Routing Guide: Links from around the web

|

|

|

Registration Now Open for Supply Chain AI Symposium in Washington, D.C.

The future of freight is intelligent. Are you ready?

The Supply Chain AI Symposium, which will be held at the International Spy Museum in Washington, D.C., on July 30, is your exclusive opportunity to delve into the transformative power of artificial intelligence. Join business leaders, pioneering technologists and leading supply chain companies to explore how AI is revolutionizing transportation, logistics and supply chain management.

Whether you lead a Fortune 100 supply chain, build AI models or sling freight for a living, this symposium offers a unique opportunity to explore how AI is being implemented in the world of the supply chain. Gain insights into cutting-edge advancements, practical applications and trends shaping the freight industry.

Space is limited, so register now to save your spot!

|

|

|

FWTV EVENT | JULY 23, 2025

|

|

|

WASHINGTON, DC | JULY 30, 2025

|

|

|

DALLAS, TX | SEPTEMBER 2025

|

|

|

Like the content? Subscribe to the Newsletter!

|

|

|

Loaded and Rolling Podcast links:

|

|

|

Download the FreightWaves App

|

|

|

|