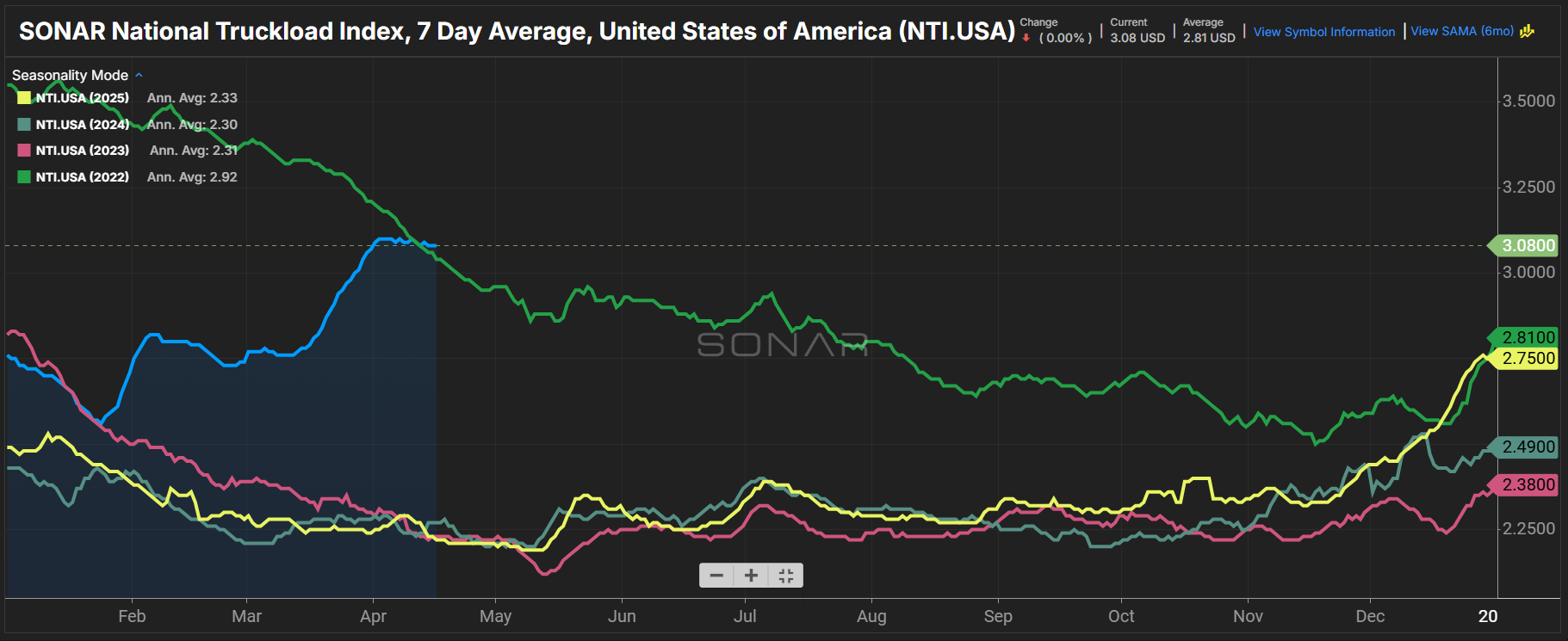

Summary: Spot rates continued to hold steady into the first half of April, remaining at levels not seen since 2022. Notably, the past week saw all-in dry van spot rates reach an inflection point, outperforming 2022 levels. This milestone was achieved not through improving market conditions but rather because spot rates have remained relatively flat while 2022 rates stair-stepped downward during the early days of the Great Freight Recession.

The SONAR National Truckload Index 7-day average (NTI) fell 1 cent per mile, all-in, week-over-week from $3.09 on April 9 to $3.08 per mile. The NTI is 27 cents per mile, or 9.6%, higher than $2.81 last month. Versus last year, the NTI is 86 cents per mile, or 38.7%, higher than $2.22 last year.

Dry van outbound tender rejection rates also showed relatively little movement, changing little over the past week and slightly lower compared with last month. The SONAR Truckload Rejection Index-Van (STRIV) fell 3 basis points week-over-week from 11.62% to 11.59%. The STRIV is 68 basis points lower than 12.27% last month and 747 basis points higher than 4.12% last year.

Interestingly, outbound tender rejection rates during this time in April 2022 were similar to those in April 2026. The difference is that the 2026 rate is 56 basis points higher than the 11.03% recorded on April 18, 2022.

Looking ahead, geopolitical moves are causing sharp changes in energy prices, impacting the cost of diesel at the pump. One theme to watch will be whether declining fuel prices prompt freight brokers to push down prices or whether carriers can continue to wield considerable pricing leverage. At the moment, the upstream contract space seems to suggest that elevated rates are here to stay despite energy prices.

There is an ongoing debate on the impact of spot market transactions and fuel prices. One camp argues that the market is driven purely by truckload supply and demand, and carriers can charge only as much as the market dictates. If prices go up or down, it is because of competition between available capacity and not because of decisions such as attempting to recoup fuel costs.

Another camp argues that fuel does have a tangible impact on small-fleet and owner-operator decision-making. While they often cannot secure a fuel surcharge, their pricing strategies are affected by energy costs, influencing choices on the type of freight, its weight and location — as states like California have notably higher fuel costs compared with the middle of the country.

The next few weeks may provide more insight into which argument holds up. If the ongoing Iran conflict finds a solution and energy markets stabilize, will rates rise or fall? Additionally, would an increase in new entrants from a rise in unique operating authorities push rates down, or will the ongoing crackdown on less regulatorily compliant motor carriers balance things out?

Finally, the coming weeks will be worth watching from a regulatory perspective, with the upcoming surface transportation bill — renewed once every five years — expected to tip the scales toward a stricter trucking regulatory operating environment. If enforcement continues to improve and technology enhancements at regulatory agencies crack down on bad actors, the market may see a higher barrier to entry, keeping trucking capacity limited and sustaining this nascent freight market upcycle.