Cost of Operations Is Everything—ATRI Confirms It’s Getting Worse

|

|

|

|

|

NEWSLETTER BROUGHT TO YOU BY — SIRIUSXM

|

SiriusXM keeps truck drivers informed and entertained with 24/7 music, sports, and more. Hear all your SiriusXM favorites on every haul for $6.06/month. Sign up.

|

|

|

Cost Control or Cost Collapse – The Market’s Not Waiting

|

|

|

(Photo: Jim Allen/FreightWaves. FATRI’s latest report drops a harsh truth — the freight market isn’t just soft, it’s upside down. Operating costs are up, margins are negative, and for the first time in 16 years, truckload carriers are in the red. If you’re not tracking cost per mile like your business depends on it — it already might.)

|

|

|

Cost of Operations Is Everything—ATRI Confirms It’s Getting Worse

|

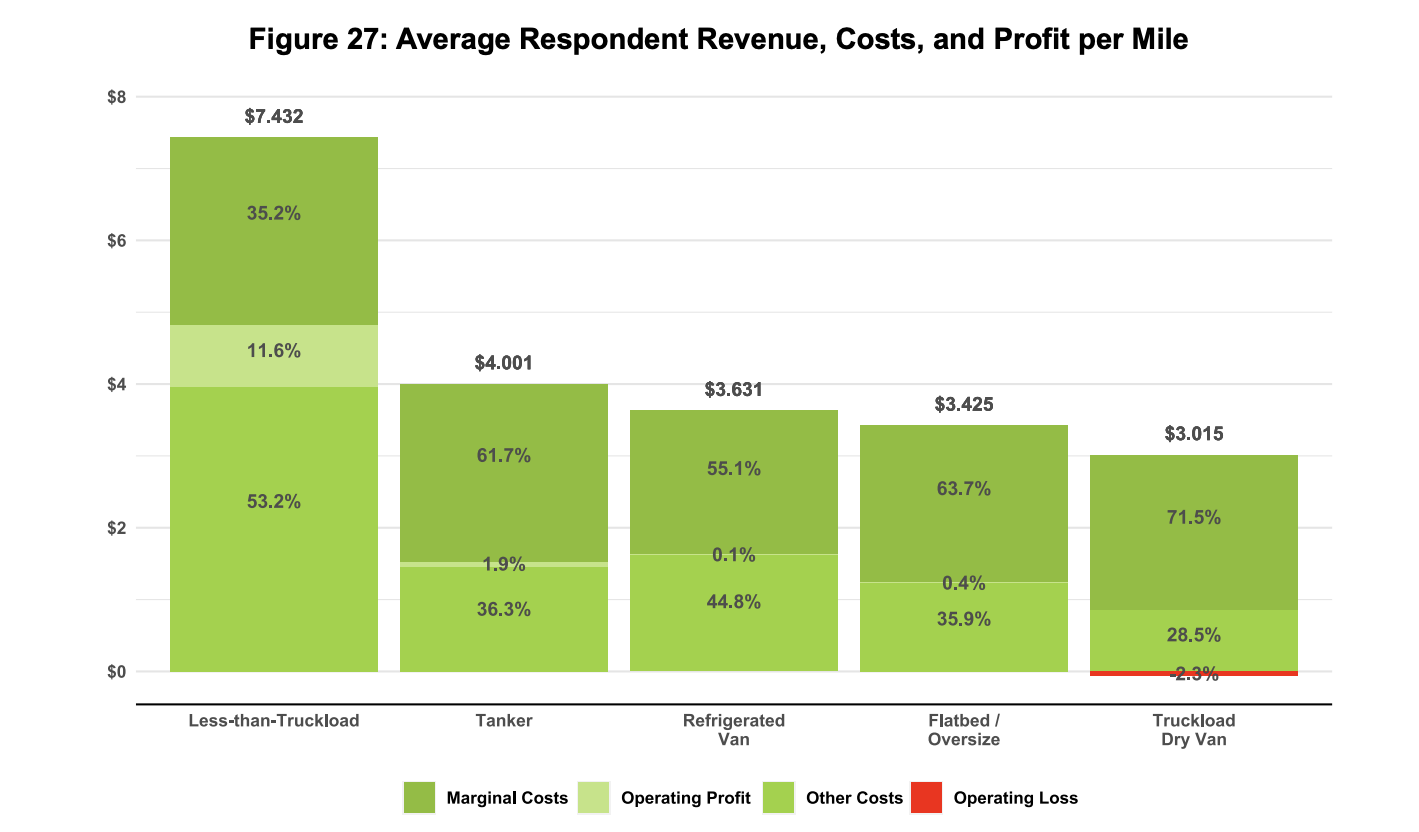

The new ATRI report just dropped, and the numbers are crystal clear: the truckload market is under serious pressure. Average operating costs clocked in at $2.26 per mile in 2024—only slightly down from 2023, thanks to lower fuel—but that masks the real problem. Without fuel, non‑fuel costs jumped a record-high 3.6%, reaching $1.779 per mile

Let’s unpack what ATRI found and what it means in plain language:

- Total Cost Per Mile landed at $2.26 in 2024. That’s only a 3-cent drop from the record high of $2.29 in 2023 — but that dip was entirely due to lower diesel prices. Strip out fuel, and you’ll find the core of your business is costing you more than ever.

- Non-Fuel Operating Costs surged to a new record: $1.779 per mile, up 3.6% year-over-year. For context, that’s a larger jump than we saw during the inflation-driven surge of 2022. And it’s hitting in the middle of a freight downturn, when revenue per mile is shrinking — not growing.

- Truck & Trailer Payments went up 8.3%, the largest increase across all cost categories. Equipment isn’t just expensive — it’s a long-term trap. Even as rates dropped, many fleets were still locked into high monthly payments from trucks bought during COVID highs.

- Driver Benefits rose 4.8%, and insurance premiums stayed elevated — partly due to nuclear verdict fears, partly because smaller carriers still get hit with higher per-truck rates.

- Toll Costs hit a new high. ATRI points out that this was driven by increased use of tolled lanes to avoid congestion — especially in the Northeast and Southeast. For long-haul carriers running up and down the I-95 or I-70 corridors, this can quietly bleed profit from your week.

And here’s the stat that should stop every owner-op in their tracks: Truckload carriers posted a negative –2.3% average operating margin in 2024. Negative. Not break-even. Not low. Negative. That’s the first time ATRI has reported red ink on the bottom line for the truckload sector in its 16-year history of this study.

|

So what’s really going on?

It’s not just that costs are rising — it’s that they’re rising while revenue falls.

Freight demand isn’t matching inflation. Rates are soft. Contract volumes are drying up. The spot market is flooded. And even though diesel cooled slightly in 2024, it’s now ticking back up again mid-year in 2025.

At the same time, ATRI found that carriers are running fewer miles with fewer drivers. The average driver-per-truck ratio dropped to 0.93 — the lowest since ATRI started measuring. Empty miles? Up to 16.7%, from 14.8% just a year prior. That means more trucks running partial or repositioning loads, burning fuel without making money.

Why this matters right now:

This isn’t just a “bad market.” This is structural.

The industry spent 2021–2022 building like we’d never see a downturn again. That freight boom covered up a lot of inefficiencies. Now that it’s gone, the skeletons are showing.

And for small carriers? You’re not operating with a safety net. You don’t have volume contracts, hedge fuel programs, or millions in retained earnings. Every penny matters.

What ATRI’s data proves is that most carriers who aren’t watching cost-per-mile down to the decimal are already losing money — they just haven’t realized it yet.

So no, this isn’t just another report. It’s a wake-up call.

If you’re dispatching yourself, running a fleet, or managing owner-ops — this report should sit on your desk. Not your inbox. It’s the scorecard. And if you’re not matching what it’s saying line for line, you’re flying blind in a storm that’s still brewing.

|

|

|

(Photo: Jim Allen/FreightWaves. A contract signed, a promise made — and now, a fight unfolding. As UPS floats early buyouts that the Teamsters call illegal, the freight world is watching. What happens next could redefine how labor deals are honored — or ignored — across the entire industry.)

|

UPS, Buyouts, and Broken Promises — The Battle Over Union Jobs Heats Up

|

When the Teamsters ratified their contract with UPS back in August 2023, it was being hailed as historic — a win that secured stronger wages, employer-paid health care, and a commitment to 30,000+ full-time union jobs. But fast forward to this summer, and the tone has shifted from celebration to confrontation.

According to the union, UPS is gearing up to offer early retirement buyouts under what it’s calling the Driver Voluntary Severance Plan (DVSP). The catch? The Teamsters say this move directly violates the national contract UPS signed just last year. They’re calling it what it is — a corporate attempt to sidestep contractual obligations and quietly downsize the union workforce.

Here’s what’s really going on:

- The contract promised at least 22,500 new full-time jobs for part-timers and 7,500 more full-time positions during the contract’s final three years.

- UPS, according to the Teamsters, is now offering buyouts instead — hoping some drivers will take a check and walk away before those new jobs are created.

- Healthcare is a sticking point too. Many long-tenured drivers are guaranteed health benefits into retirement under the contract. These buyouts, as proposed, wouldn’t carry those protections.

And that’s not all. UPS is also dragging its feet on key commitments like heat safety improvements. Under Article 18 of the agreement, the company is supposed to deploy no less than 28,000 air-conditioned delivery vehicles by 2028. The Teamsters say they’ve asked for data on that rollout — and got silence in return.

In their words, “UPS is trying to weasel its way out of creating good union jobs.” But this isn’t just a union issue — it’s a freight industry issue. Because when one of the largest logistics companies in the world starts violating its own agreements, it sends a message. And it sets a tone. Smaller carriers, warehouse workers, and the independent driver community are all watching this unfold. If the biggest players can break promises without pushback, others might try too.

So what now?

The Teamsters are digging in, threatening legal action, and calling on their members to reject any buyout packages that undermine the contract. They’ve made it clear: this isn’t about severance — it’s about standing firm on what was already won.

For the rest of the industry, it’s a reminder that contract protections only matter if you’re willing to enforce them. And whether you’re union or not, how this story ends could shape the future of labor expectations across all corners of trucking.

Stay tuned — this one’s just getting started.

|

|

|

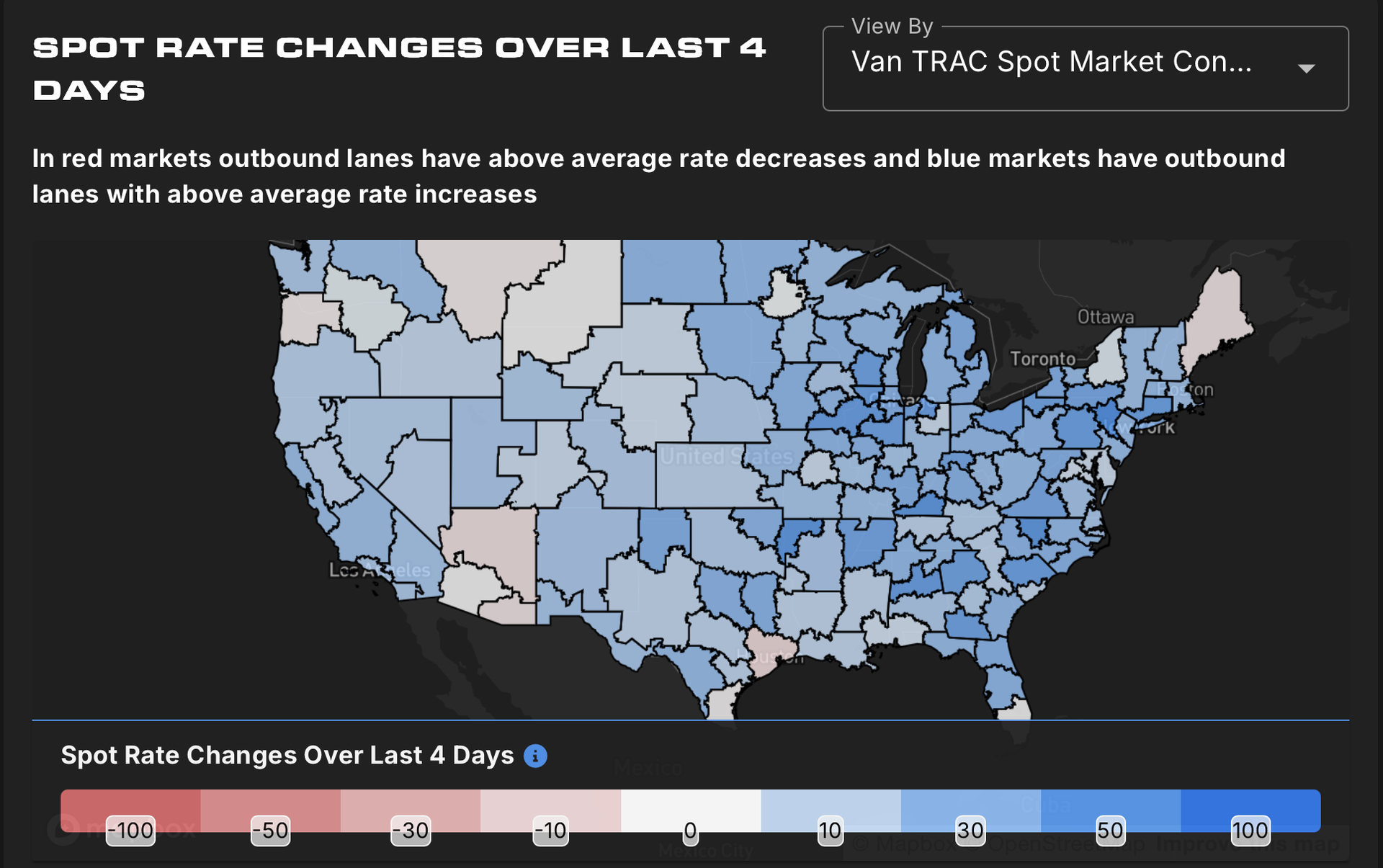

(Source: SONAR Spot Rate Changes Over Last 4 Days (Van TRAC Map). Blue means strength — and right now, most of the map is glowing. Spot rates climbed across much of the Southeast, Midwest, and Mid-Atlantic, signaling early July 4th pressure. Red zones? They’re cooling off fast.)

|

Freight Market Conditions – Week of July 3, 2025

|

If you were hoping the Fourth of July surge would send the freight market into full recovery mode, pump the brakes. There’s movement — yes — but it’s not a full-on breakout. Volumes are shaky. Diesel remains unpredictable. And spot rates are hovering, not spiking. This isn’t a "sit back and wait" moment. It’s a "check your positioning and play the next lane smart" moment.

We’re not in the ditch — but we’re definitely not cruising uphill yet either. So let’s break it down, chart by chart, and figure out how to read this week’s freight field.

|

|

|

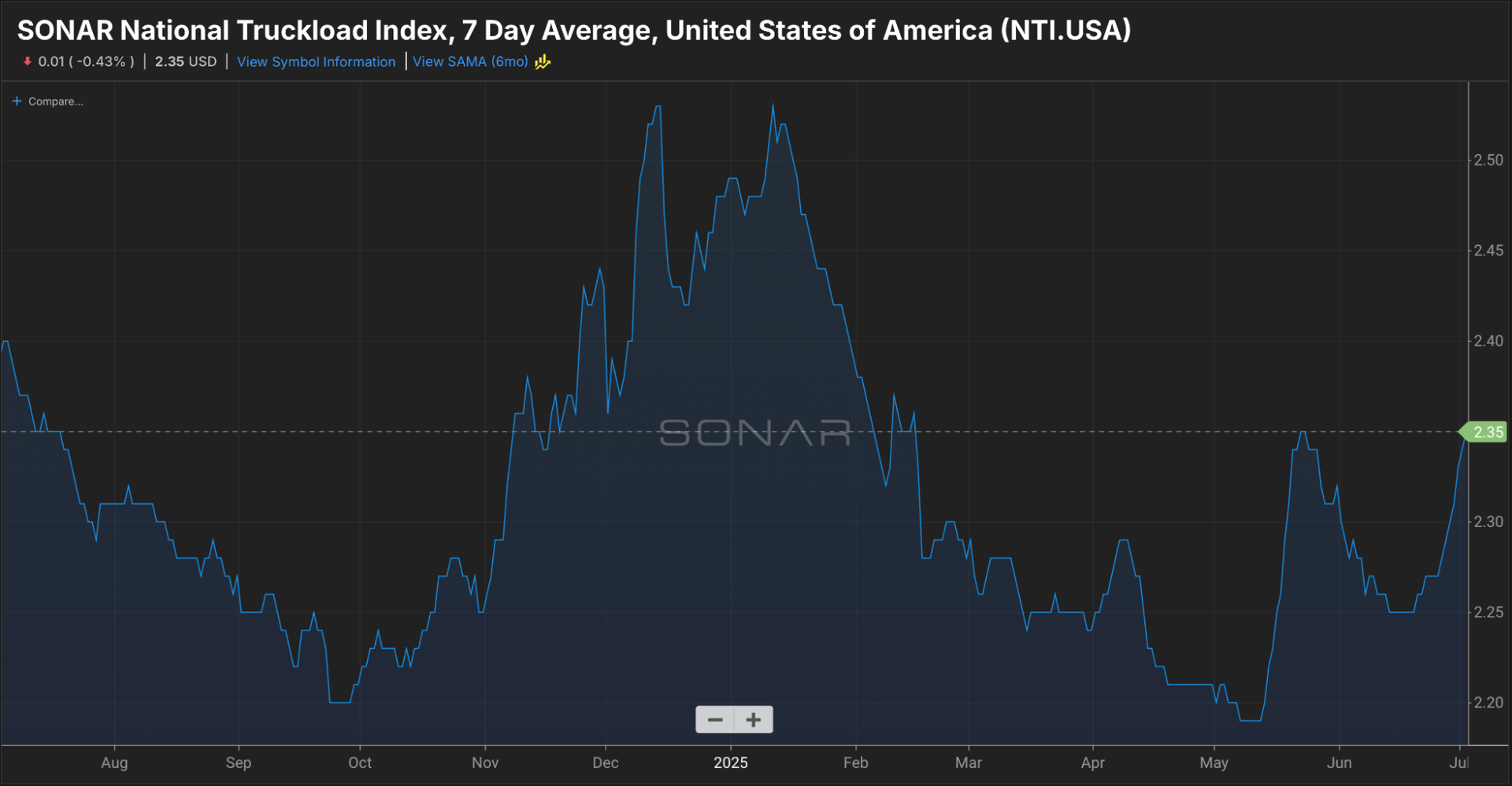

(Chart: SONAR National Truckload Index (NTI.USA). Spot rates are climbing—but just enough to make you pay attention, not enough to signal a full rebound.)

|

Spot Rates Inch Up, But Don’t Call It a Comeback – NTI at $2.35

The NTI just posted a clean $2.35 average per mile. That’s the highest we’ve seen since early June and a sign that freight pressure is showing up in price—but let’s not crown it a comeback just yet.

This latest bump likely stems from pre-holiday urgency. Shippers needed freight covered fast, especially in tight markets. But don’t miss the fine print: this number includes fuel. And with diesel jumping to $3.72 last week, some of that rate lift is already spoken for in rising operating costs.

Here’s the play: treat $2.35 as your reference, not your reward. If your breakeven is floating in the $2.50+ range with current fuel, you can’t afford to book blindly under this number. Use tools to price smarter. Focus on regions showing rate resilience and avoid soft lanes where brokers still have all the leverage.

|

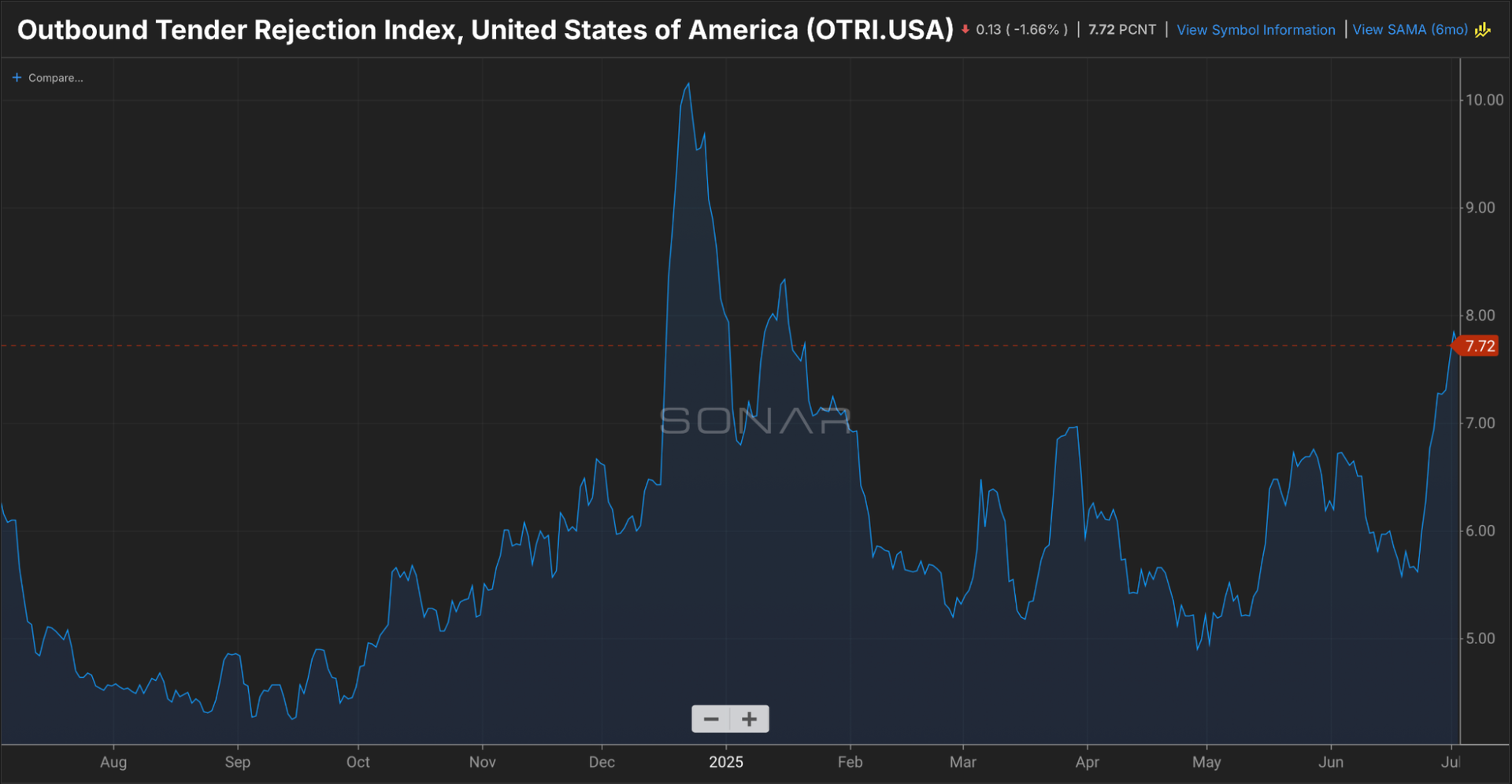

(Chart: SONAR Outbound Tender Rejection Index (OTRI.USA). Carriers are slowly regaining leverage — rejections are up, and spot opportunity is following.)

|

Rejections Keep Climbing – OTRI at 7.72%

Tender rejections are now sitting at 7.72% — a steady rise from recent weeks and the highest we’ve seen since February. That means more carriers are turning down contract freight, and brokers are having to hustle harder to cover loads.

Here’s what that really means for you: the spot market is gaining some leverage back. Carriers aren’t just saying yes to everything anymore, and that opens the door to higher-paying loads — but only in the right markets.

The rise is notable, but we’re still not at the 10%+ zone that triggers broad-based rate spikes. So use this intel tactically. If rejection rates are climbing in your region, that’s your window to renegotiate. If they’re flat, don’t expect much sympathy when you ask for more per mile.

|

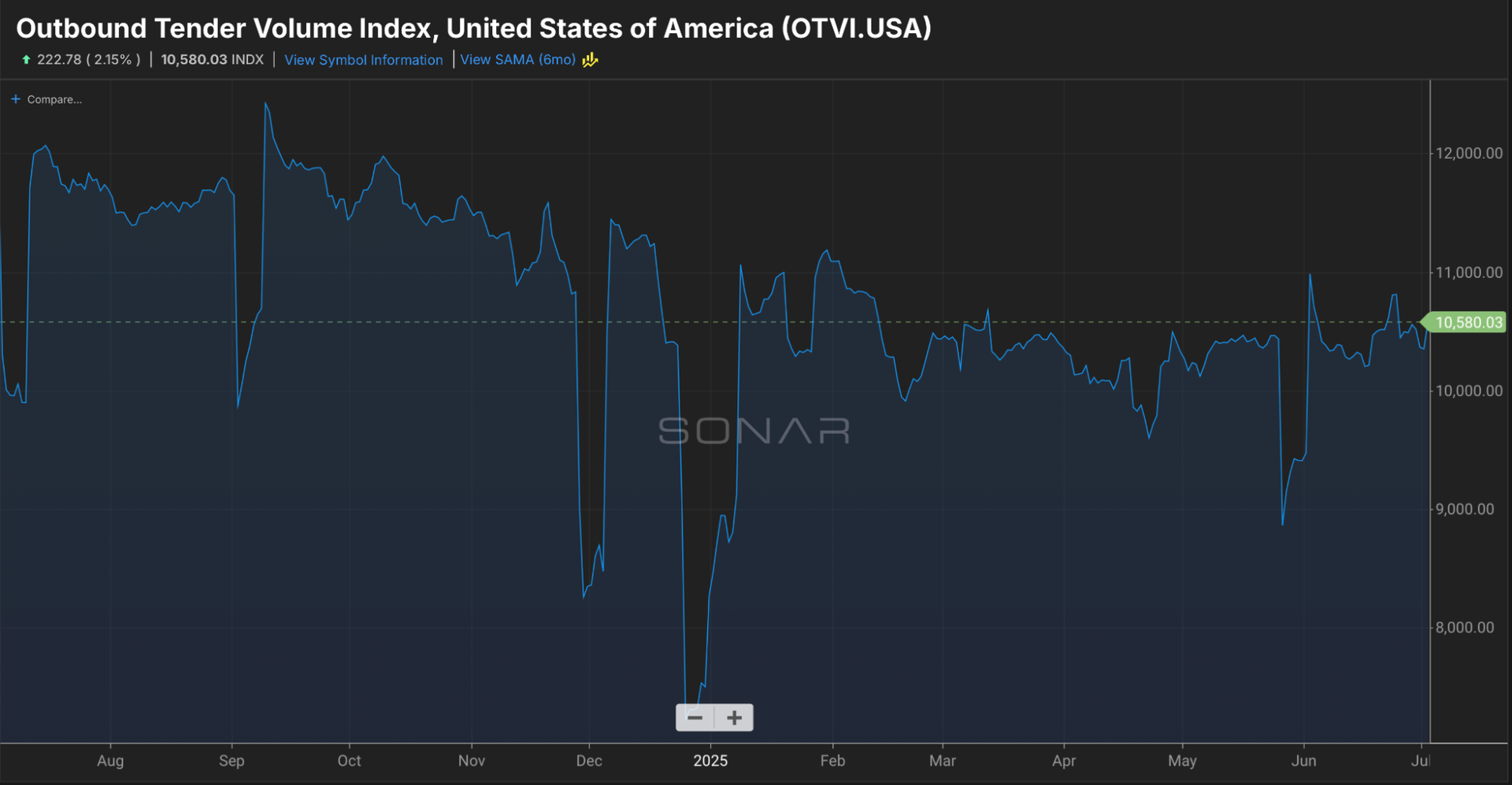

(Chart: SONAR Outbound Tender Volume Index (OTVI.USA). Demand isn’t booming, but it’s not falling off a cliff either — and that stability matters.)

|

Outbound Tender Volume Index (OTVI) – Volume Holds the Line at 10,580

The Outbound Tender Volume Index (OTVI) just took a notable dip, down over 3% week-over-week. That means fewer loads are being offered into the market compared to recent averages. OTVI is our proxy for shipper demand — when it falls, it means the pie is shrinking and there are fewer loads to go around. And that can get real uncomfortable, real fast, especially if you’re relying solely on spot freight.

To give you a sense of scale: volumes today are sitting right around 10,451 — a far cry from the 11,000+ range we saw earlier in the year. That drop means more carriers are now chasing fewer opportunities, and that’s when brokers get bold. Expect more “that’s all I got in it” phone calls and tighter rate spreads on apps.

Here’s how to play this: don’t just chase volume blindly. Pair this with OTRI data — if volume is dropping but rejections are climbing in certain markets, that’s where brokers are most desperate. Target those zones. And don’t forget, slow volume means longer booking windows, so book smarter, not faster.

|

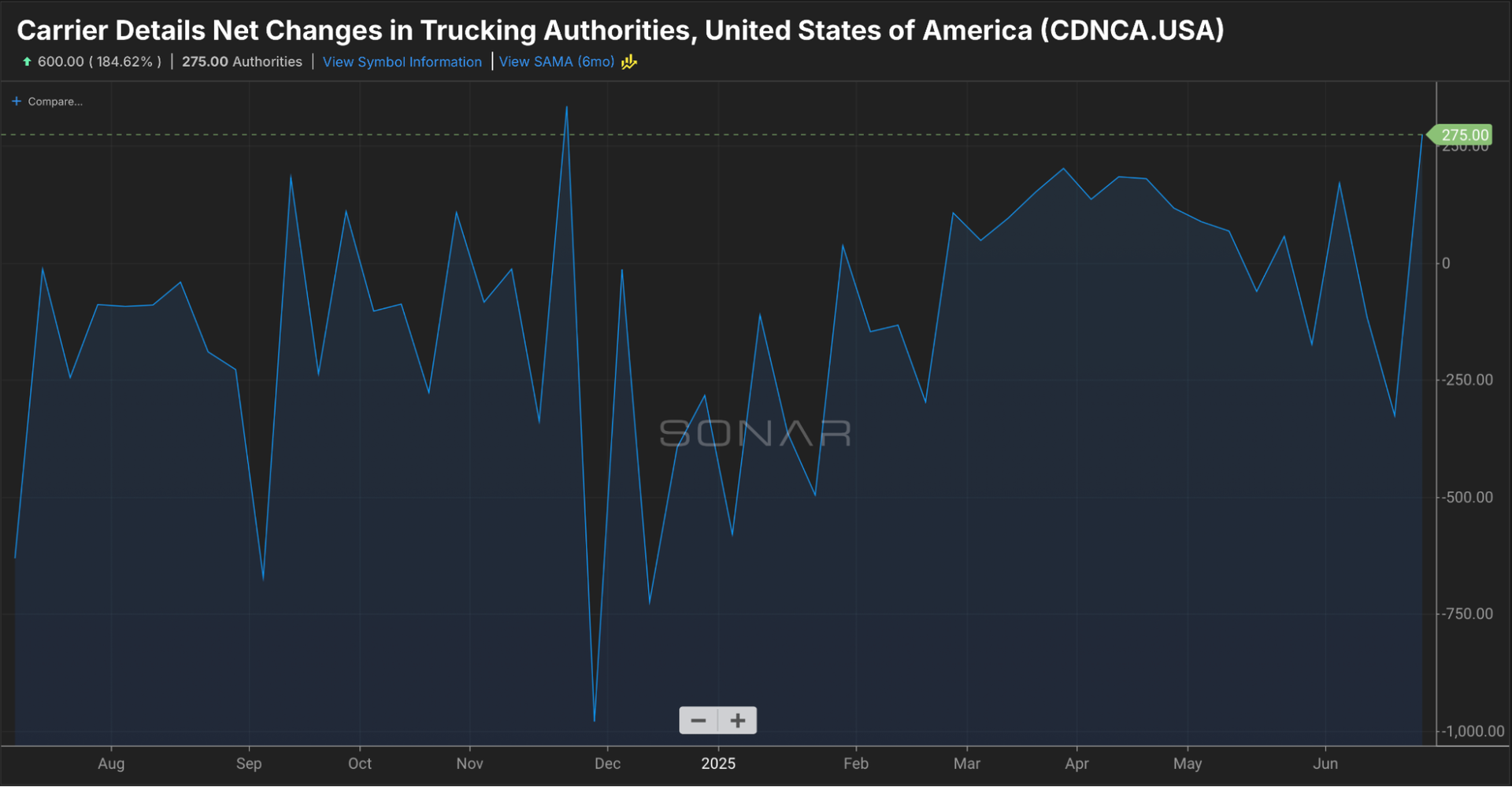

(Chart: SONAR Carrier Details Net Changes In Trucking Authorities (CDNCA.USA). New carriers are still entering the market — and that could signal misplaced confidence.)

|

Carrier Count Jumps – Net Gain of 275 Authorities

Here’s the wildcard: last week saw a net gain of 275 active carrier authorities — one of the biggest weekly increases this year. It’s a head-scratcher considering where rates and fuel are sitting.

This could be seasonal (folks betting on a July bump) or delayed paperwork from earlier applications. But either way, it’s new capacity in a market that’s already struggling with too much of it.

For the carriers already running lean and smart, this is your reminder: not everyone entering the game has staying power. Keep your lanes tight. Let the market shake out. The ones chasing “easy money” without a solid strategy won’t last long.

The Real Talk

This week isn’t about hope or hype — it’s about awareness.

You’re looking at a market with subtle shifts, not seismic ones. Rates are climbing — barely. Volume is stable — for now. Diesel is unpredictable — again. The only thing that’s consistent? The need to stay data-driven and dialed-in.

This week proves that there’s still opportunity for the carriers who can stay disciplined, read market patterns, and price their lanes with intention. That means understanding what rejections tell you about leverage, knowing when volume dips are just noise, and factoring fuel into every single move.

If you’re still operating with guesswork, you’re driving blind. But if you’re reading this, chances are you’re the kind of carrier who’s sharpening the playbook every single week.

Let’s keep doing what others aren’t — thinking ahead, planning smart, and staying in control.

This market may not be booming, but the smart ones are still winning. Stay sharp.

|

(Photo: Jim Allen, FreightWaves. Del Monte’s Chapter 11 filing sends ripples through the freight world — with frozen, canned, and shelf-stable food shipments grinding to a halt, small carriers depending on food and grocery freight could see fewer loads and tighter competition in the weeks ahead.)

|

Cans, Contracts, and Collapsing Freight – What Del Monte’s Bankruptcy Really Means for the Market

|

Another day, another big brand filing bankruptcy — but this one hits different. Del Monte Foods, a name most of us grew up seeing in our kitchens, just had all three of its operating divisions file for Chapter 11 bankruptcy. While the headlines might focus on canned veggies and frozen meals, the freight story hiding underneath is what small carriers can’t afford to ignore.

This isn’t just about one company. It’s about what happens when legacy brands start crumbling — and what that means for freight volumes in a market already stretched thin.

Let’s Start With the Facts:

- Del Monte Foods’ divisions, including Sager Creek, Fieldbrook Foods, and Contessa Premium Foods, are all under Chapter 11 protection. Combined, they cover a wide spectrum of shelf-stable, frozen, and ready-to-eat products that move via dry van, reefer, and multi-stop retail delivery.

- The company is sitting on more than $500 million in liabilities, citing inflationary pressure, supply chain disruptions, and weak consumer demand as key drivers of the collapse.

- Operations have already been cut. Facilities in multiple states have shut down, and manufacturing volumes are expected to drop even further as the company attempts to restructure or sell assets.

Why This Should Matter to Carriers

Del Monte’s freight footprint was massive — thousands of shipments annually to grocery distribution centers, warehouses, cold storage facilities, and port locations. When a company like this hits pause or scales back, those loads don’t just get reassigned — they disappear. That’s a real hit to load boards, brokers, and carriers who were moving that freight directly or indirectly.

If you’re a small carrier or dispatcher working in the food and beverage space, this is a direct shot across the bow.

- Fewer outbound loads from shuttered plants = lower regional volumes, especially in rural areas where those facilities once pumped out dozens of truckloads per week.

- More competition for remaining food freight = tighter margins, slower turn times, and more brokers low-balling rates as excess capacity floods the system.

- Ripple effects through third-party logistics = if you were hauling for a 3PL that had a contract with Del Monte, you might already be feeling delayed payments, if not outright load loss.

What’s Driving This Collapse?

This isn’t just bad business — it’s a sign of broader economic strain. According to the filings and reporting, Del Monte’s downfall boils down to a few key freight-relevant issues:

- Costs went up, demand went down. The post-pandemic consumer buying patterns shifted hard. People aren’t stockpiling canned goods like they were in 2020. That means warehouses filled up, shelf space shrank, and retailers ordered less — directly reducing outbound volume from Del Monte’s plants.

- Private label dominance. Retailers like Walmart and Kroger are pushing their own store brands harder than ever. That eats into Del Monte’s share and forces them to fight for shelf space with fewer SKUs — and fewer truckloads.

- Too many assets, not enough liquidity. With manufacturing operations spread out and raw material costs ballooning, Del Monte simply couldn’t keep up. Every penny spent on equipment and facilities needed to return freight-generating revenue. It didn’t.

What Small Carriers Should Watch For

Del Monte’s downfall is part of a trend — legacy brands underperforming, consolidating, or disappearing. That matters because they represent repeatable, predictable freight, not one-off spot market scraps. And when that kind of freight dries up, it forces more carriers to chase less volume.

Here’s what you need to do now:

- Start tracking food and beverage brands in your lanes. If one of your key customers or brokers hauls for a name-brand food client, keep tabs on that client’s financial health. Bankruptcy filings often have a domino effect.

- Watch distribution center volumes. If a major shipper like Del Monte was feeding product into hubs in Indiana, Arkansas, or Georgia, those regions may see short-term load loss — and a dip in rates.

- Check your exposure. Were you relying on reefer freight tied to frozen or shelf-stable food? Now’s the time to diversify into other segments or prepare for rate drops as capacity shifts.

This Is a Freight Forecast, Not Just a Bankruptcy

When names like Del Monte file for bankruptcy, it’s not just bad news for canned corn. It’s a real-world indicator that freight demand from the consumer goods sector — already wobbly — is weakening even more.

Carriers who ignore this will keep chasing yesterday’s loads. But those who recognize the signs early? They’ll pivot, shift capacity, and avoid the dead zones that are forming around failing shippers.

This isn’t fear — it’s foresight.

The question isn’t if more volume will vanish.

It’s who will be ready when it does.

|

|

|

After a week where reefer rates jolted up, driver shortages stayed sticky, and small carriers kept asking how to break into better freight—this week’s podcast takes a cold, hard look at an opportunity that’s heating up fast: fresh freight.

Adam sat down with Clay and Nick, co-founders of FreshX, to dig into what they’re building—and why small fleets have more power in cold chain than most people think. Clay brings the experience of a reefer operator who knows the pain points firsthand, and Nick brings the strategy, tech, and vision behind a platform that’s helping owner-ops and small fleets plug into steady, contract-quality loads.

In this episode, the FreshX duo breaks down how the produce and cold chain markets actually work, why direct shipper access is broken, and what it takes to build real consistency in one of trucking’s most volatile segments. Spoiler alert: It’s not about chasing California lettuce in July. It’s about understanding regional rhythms, planning seasonal pivots, and showing shippers you can deliver more than just a clean trailer.

If you’ve ever thought, “I’d love to run reefer, but I don’t have the network,” this episode is for you. Clay and Nick lay out the roadmap—from onboarding to load planning to working smarter with brokers who understand your capacity and equipment.

Cold freight isn’t just for the megas anymore. And if you’re ready to play the long game, FreshX is showing how small fleets can win in a big way

|

(Photo: Jim Allen/FreightWaves. The fatal I-20 crash in Kaufman County wasn’t just a tragic accident — it exposed major cracks in safety enforcement and vetting. A young driver, admitted fatigue, and a carrier with multiple crash reports highlight how overlooked compliance puts lives at risk.)

|

When Loose Safety Oversight Becomes a Tragedy

|

By now, many in trucking have heard about the devastating crash on I-20 in Kaufman County, Texas, where an 18-wheeler plowed into multiple vehicles, killing five people. The details are hard to stomach. A young driver, just 27 years old, told authorities he fell asleep at the wheel. The truck? Registered to a small carrier based out of Florida. And when you pull the curtain back—when you really look at the carrier’s public safety profile—it becomes clear: this wasn’t just a tragedy. It was predictable.

The FMCSA’s own data tells the story. This carrier had five reportable crashes in a short span across 2023 and 2024—two with injuries, one in poor weather, and most involving tow-aways. Even more concerning: a driver behind the wheel of an 80,000-pound machine, running overnight through construction zones, with no co-driver, no fatigue monitoring, and—based on his own words—no business being on the road at that moment.

This is what happens when our industry keeps ignoring the enforcement gap. We don’t have a shortage of rules. We have a shortage of accountability.

The crash logs for this carrier show a pattern: incidents across several states, multiple contributing factors (including rain, construction zones, and other vehicles), and no meaningful drop-off in operations afterward. No revocation. No red flag in the system that stopped them from running. And so they did—until it ended in lives lost.

What This Means for the Industry

We’ve got brokers sourcing freight without knowing what these carriers really look like on paper. We’ve got shippers turning a blind eye to safety scores because they need freight moved fast. And we’ve got dispatchers—some knowingly, some not—booking loads for fleets that shouldn’t be rolling.

And the ripple effect? Small carriers with clean records get lumped in with the bad actors. Trust erodes. Insurance premiums go up. The public sees another “trucker crash” headline and never asks about the dispatch, the vetting, or the fact that a carrier that showcased inconsistencies in registration data provided, wasn’t flagged for further review.

This Isn’t a Carrier Size Issue. It’s a Compliance Culture Issue.

It’s not about mega fleets vs. small carriers. It’s about whether or not you’re doing things right. Vetting drivers. Monitoring hours. Tracking fatigue. Training people on when to stop—not just how to drive. Every carrier, big or small, has a duty to the people they share the road with.

And here’s the ugly truth: as long as enforcement is weak, as long as shippers and brokers don’t do their due diligence, and as long as we keep looking the other way when red flags show up on SMS or SAFER, we’ll keep having more of these headlines.

The Ask Is Simple

FMCSA, enforce what’s already in place. Brokers, vet your carriers like lives depend on it—because they do. And small carriers? Don’t cut corners. Your reputation, your insurance, and your future depend on keeping your safety record clean.

This tragedy wasn’t just an accident. It was a failure of oversight, discipline, and accountability. And unless we change how we operate, it won’t be the last.

|

Final Word – The Squeeze Is On

|

This week didn’t bring a sudden market jolt—but it did bring patterns into clearer view. Rates are sitting still. Volume is sluggish. And enforcement—across safety, language proficiency, and labor—just got louder. From courtrooms to crash sites to carrier spreadsheets, the message is simple: accountability is coming.

The pressure isn’t just economic anymore. It’s structural. Carriers are being asked to run leaner, safer, and smarter all at once—and those who can’t adapt will get squeezed out, not just by fuel or freight, but by the weight of poor systems and shortcuts.

So how do you stay in the game?

You sharpen your numbers. You stay ahead of regulation. You pick your lanes with intention. And you treat every week’s data not as a wall—but as a map.

Because in a market like this, it’s not about waiting for the rebound. It’s about building the muscle to operate—profitably, compliantly, and consistently—while others burn out. That’s the edge. That’s the Playbook.

Let’s move forward with clarity, not noise. And let’s make every mile count.

|

|

|

|