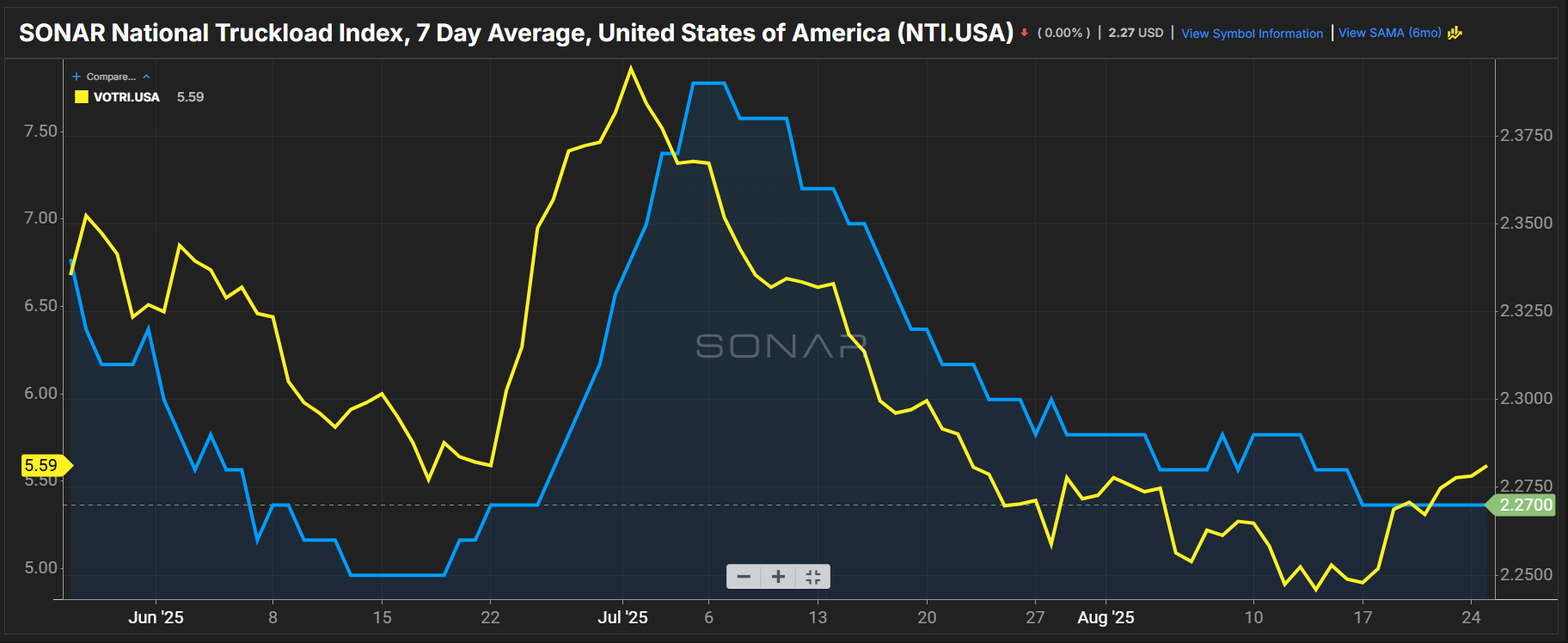

Summary: The dry van doldrums continue, with the upcoming Labor Day weekend doing little to change a sluggish spot rate environment. The SONAR National Truckload Index 7-Day Average was flat week-over-week at $2.27 per mile. Compared with last month, dry van all-in spot rates are 3 cents per mile lower than $2.30 on July 26 and 1 cent per mile lower than last year’s value of $2.28 per mile.

The contract space saw dry van outbound tender rejection rates rally, with VOTRI gaining 59 basis points week-over-week from 5% to 5.59%. Carrier pricing power remains more favorable, but only slightly. Compared with last year, VOTRI is 140 basis points higher than 4.19% in 2024.

Regulatory attention toward truckload capacity that lacks English language proficiency so far has not shown up in the data. Additionally, moves toward pausing all new commercial truck driver work visas may be an upstream development to watch, but given resource challenges for state and federal regulatory agencies, adequate enforcement remains to be seen.

An added challenge is compliance and how safety scores are calculated. For a carrier that may be running a large pool of unqualified drivers, if its safety score is above a certain threshold, the likelihood of being stopped for a roadside inspection diminishes.

Additionally, according to the most recent FMCSA data for 2025, roadside inspections yield far higher equipment issues than driver ones. When looking at inspections that result in a carrier being put out of service, driver OOS rates are only 6.83% while vehicle inspections yield a much higher OOS rate of 23.55%. Theoretically, one out of every four trucks on the road would need to be shut down to address a safety or equipment-related issue. Finding those trucks is easier said than done.