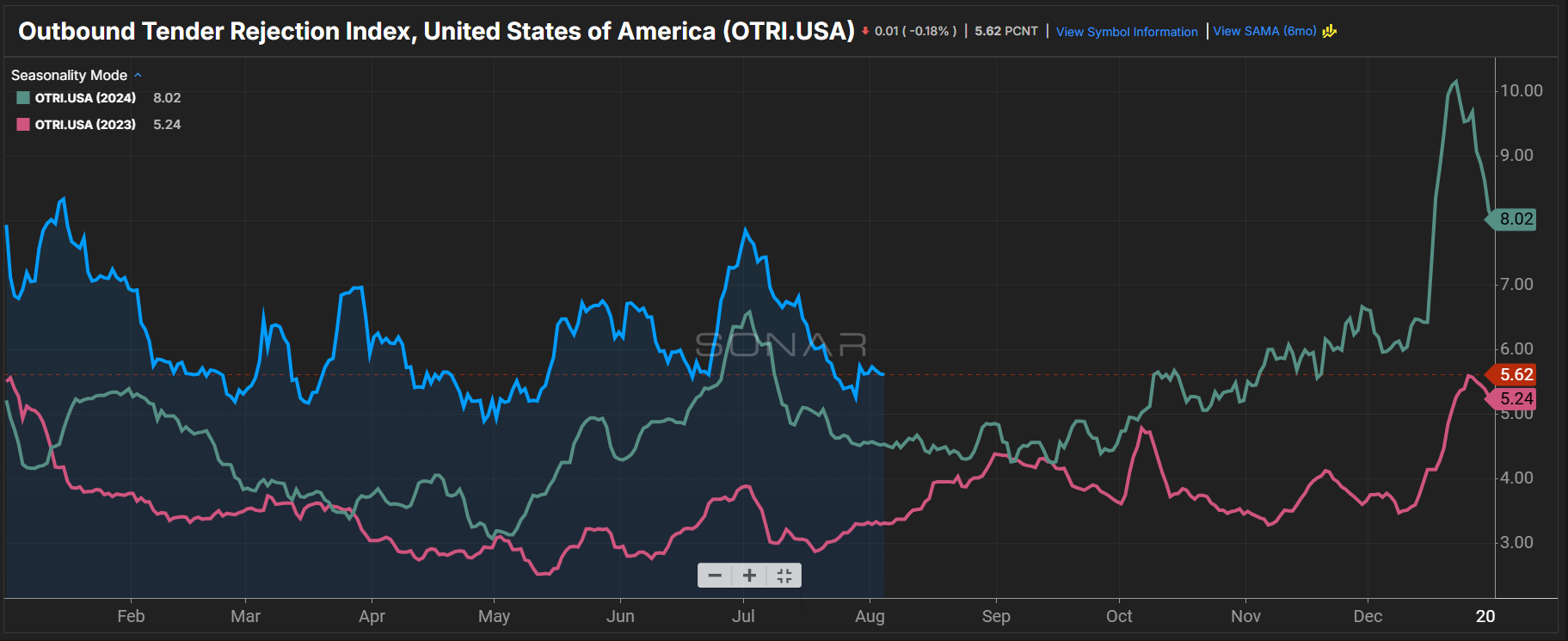

Summary: The first days of August saw a stabilization in nationwide outbound tender rejection rates following seasonal declines in the last week of July. OTRI rose 35 basis points in the past week from 5.27% on July 28 to 5.62%. Compared to the previous two years, carrier pricing power is in a more favorable position. In 2023, OTRI was 230 bps lower at 3.32% while in 2024 it was 108 bps lower at 4.54%.

Despite the positive year-over-year comps, when looking at outbound tender rejection rates by equipment type, the dry van segment continues to lag behind the reefer and flatbed segments.

Dry van outbound tender rejection rates rose 32 bps w/w from 5.14% to 5.46% and are 100 bps higher than 4.46% on Aug. 5, 2024. A challenge for the dry van space remains that despite better outbound tender rejection rates, there is significantly less outbound tender volume. Compared to the past two years, VOTVI is 1,346.02 points or 16.6% lower than 2024 and 1,188.31 points or 17.6% lower than 2023.

Reefer and flatbed outbound continue to outperform, but their total market share is both smaller and more volatile, due to their specialized equipment types. Reefer outbound tender rejection rates jumped 253 bps w/w from 10.18% to 12.71%. Notably, compared to the past two years, ROTRI is 463 bps higher than 8.08% in 2024 and 847 bps higher than 4.24% in 2023. The improvement in reefer tender rejection rates came as reefer outbound tender volume is much lower. Compared to the previous two years, ROTVI is 148.34 points or 11% lower than 2024 and 126.43 points or 9.5% lower than 2023.

The flatbed segment saw some softening following the July Fourth holiday but remains higher compared to y/y comps. FOTRI fell 218 bps w/w from 13.92% to 11.74%. Compared to the previous two years, FOTRI is 422 bps higher than 7.52% in 2024 and 365 bps higher than 8.09% in 2023. Interestingly, when looking at flatbed outbound tender volumes, the amount of capacity exits appears to be having an impact, as FOTVI is at its highest level in the past two years at 1,849.45 points or 7.8% higher compared to 2024 and 629.46 points or 2.5% higher than 2023.