Labor Falls Flat, Freight Felt It First

|

|

|

Reading Between the Lines – Freight’s Quiet Warning Signs

|

|

|

(Photo: Jim Allen, FreightWaves. As freight rolls on, policy decisions made in Washington continue to shape what’s next for small carriers)

|

|

|

Labor Falls Flat, Freight Felt It First

|

The July labor market reversal wasn’t subtle—but its freight impact could be. With retroactive data revisions and a shrinking job gains trend, consumer caution is becoming freight suppression. The surveys show talk of spending hanging out on pause, especially among those most likely to drive truckload demand—retail and blue-collar households.

In trucking terms, that’s a double whammy: fewer goods moving into stores, and less movement once they’re in. Import-heavy lanes may lag. Final-mile and brick-and-mortar restocking routes may hold up—but only if shipping signals stay stable. Otherwise, slower labor and low confidence ripple through every freight node.

We’ve seen this pattern before—late-stage holiday pull-forwards, tariff-triggered overbuying, and inflation jammed into declines all feed short-lived bumps. But right now? It’s just belt-tightening, not bullish momentum.

Why Small Fleets Should Care

- Spot rate pressure rises: Carriers chasing freight face tougher competition—and shrinking rate power.

- Contract freight softens: With retailers cautious on inventory, contract lanes cool before rates heat.

- Regional demand matters: Regional metro freight (e.g. Atlanta holiday restocking) may show better signs early—but the patchwork recovery leaves most areas lean.

- Costs still climbing: Diesel, insurance, and rate negotiation margins remain sticky—so breakeven matters more than ever.

What to Do Now

- Lean into relationships that still matter: Whether it is a good broker you are working with or shipper you are contracted to. Grocery replenishment, light manufacturing, and specialized still have legs if demand stays steady.

- Work existing freight harder: Strong relationships with contract shippers and industry relationships are more valuable than ever.

- Track labor data as freight data: Jobs, unemployment claims, and consumer confidence are not background noise—they’re leading indicators.

- Run your numbers weekly: Run your operating ratio calculator, dead mileage, broker trends—don’t let random loads dictate your breakeven.

A weaker labor market isn’t a market signal—it’s a real tension. Where consumers pause, freight shrinks. Where jobs cool, rates dip. This is why you can’t rely on autopilot in July. Small fleets win when they see the shift coming—and plan through it. Demand might still be growing—but it’s peaking in places, and disappearing in others.

|

|

|

(Photo: Jim Allen/FreightWaves. Manufacturing took a tumble in July.)

|

Manufacturing Layoffs Hit Key Freight Corridors

|

Manufacturing took another hit in July, with the Institute for Supply Management’s PMI dropping to 48.0, marking the fifth straight contraction month. Factory jobs sank to the lowest level in five years, and new orders stayed below 47 for the sixth consecutive month.

This isn’t just unemployment—it’s fewer parts moving through the supply chain, slower restocking, and lasting weakness across lanes tied to factories and industrial freight hubs.

To make matters worse, over 8,700 jobs were recently slashed across freight-related sectors—trucking, warehousing, logistics, and food distribution companies all announcing mass layoffs. Stanley Brothers, Lacroix Electronics, Republic National Distributing—multiple big names cutting staff across the U.S. and Mexico.

Why This Matters for Trucking

- Fewer factory orders = fewer TL and LTL shipments. When factories slow, raw materials and outbound shipments drop before retailers feel the pinch.

- Carriers tied to industrial lanes now face leaner freight—that means more competition for the remaining volumes and constant downward pressure on rates.

- Ports and intermodal hubs see lagging volume. Import-heavy ports may hang on a bit longer, but domestic outbound freight tied to manufacturing zones is shrinking.

What Smart Fleets Are Doing

- Watch your lane heat maps—if your route ties to manufacturing zones, track demand signals closely and hedge with shorter runs in healthier lanes.

- Diversify equipment and capacity—consider all options including if you need to downsize equipment that is idle or run alternate areas where volume is more stable right now.

- Lean into contract freight—industrial lanes often slow before contract rates shift. Make sure your rates reflect true cost—even if volume lags.

- Run breakeven against a range of demand scenarios—not just best-case. If your margins get thinner, know where that break point sits.

The Playbook Check

Manufacturing layoffs aren’t a flashpoint—they’re a trend—and they tend to reverberate through freight in waves. When factories slow, loading docks idle. When loaders idle, so do trucks. That’s why keeping tabs on industrial data matters as much as the usual freight stats.

If you’re still relying on “factory-to-store” lanes or raw material routes, now’s the time to re-evaluate—not wait for the bounce. Freight isn’t dead. It’s reallocating. And the smart carrier will move with it, not behind it.

|

|

|

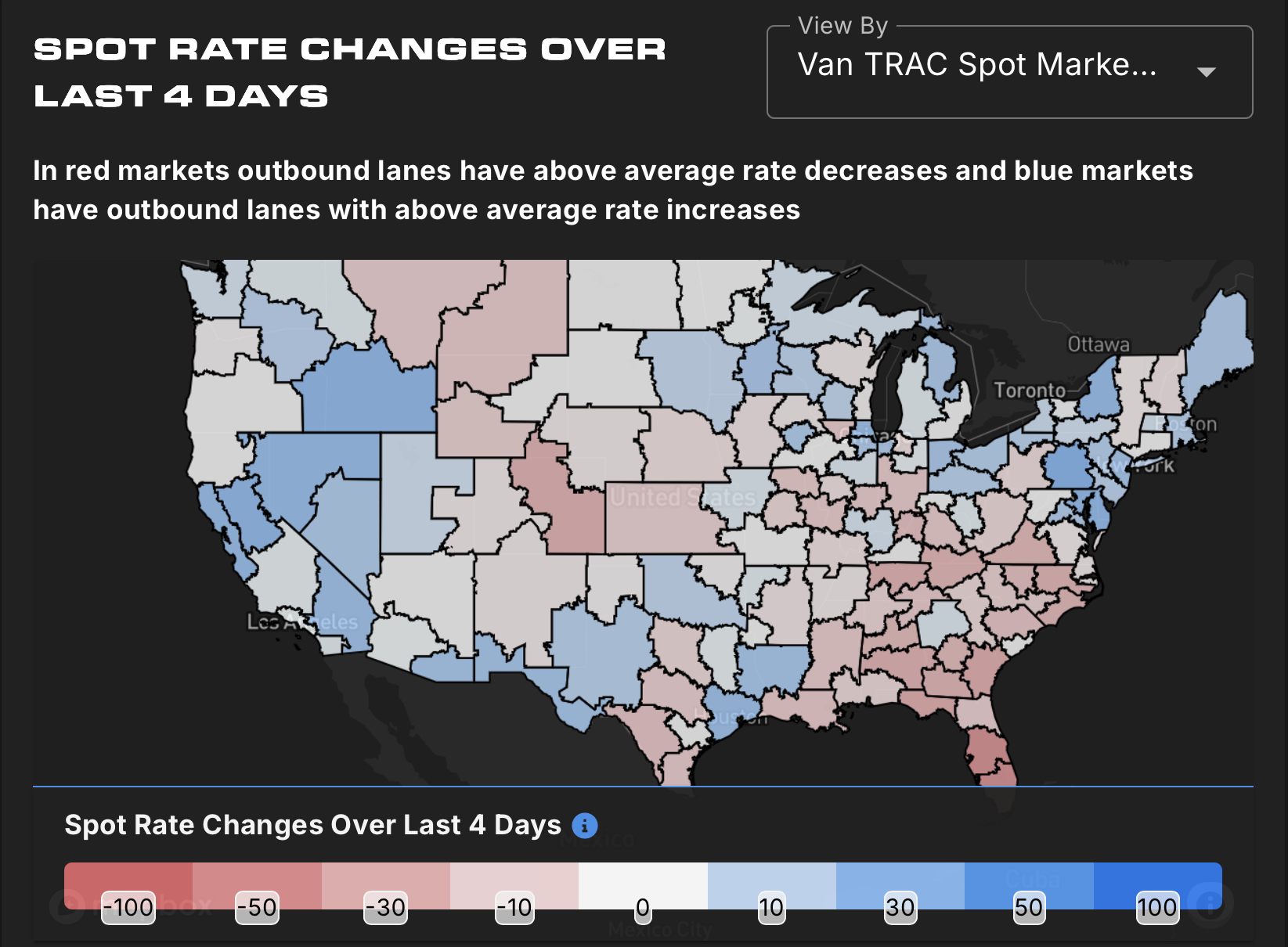

(Source: SONAR Spot Rate Changes Over Last 4 Days (Van TRAC Map). Red is bad news. Most outbound lanes across the Southeast, Midwest, and Central U.S. saw rate drops. Blue pockets are few and far between—know before you go.)

|

Market Conditions Roundup – When Data Doesn’t Lie, but It Doesn’t Shout Either – Week of August 1, 2025,

|

This week’s numbers don’t scream recession—but they don’t whisper recovery either. They sit in that uncomfortable middle ground where everything looks “okay” on the surface, but every chart tells a deeper story when you read between the lines.

We’ve got a labor market that stalled out in July, with hiring momentum cooling off just as back-to-school season starts to ramp. Manufacturing layoffs are quietly creeping up again, and containerboard production—an early signal for retail and shipping demand—just fell to a two-year low. Add in the fact that one of the most respected 400-truck fleets in the country just shut its doors, and it’s pretty clear: freight isn’t dead, but it’s definitely not well.

And here’s the kicker: all this is happening while diesel climbs back near $4 a gallon, tender rejections keep falling, and spot rates are slipping just enough to sting—but not enough to spark outrage.

This kind of environment isn’t defined by sharp crashes. It’s death by a thousand paper cuts. Volumes aren’t tanking—but they’re not growing either. Rates aren’t collapsing—but they sure aren’t bouncing back. And the cost of doing business? Still going up.

So if you’ve been feeling like something’s off even though the headlines say we’re stable—you’re not wrong. The data isn’t lying. But it’s not telling the full truth either… unless you know how to listen.

|

|

|

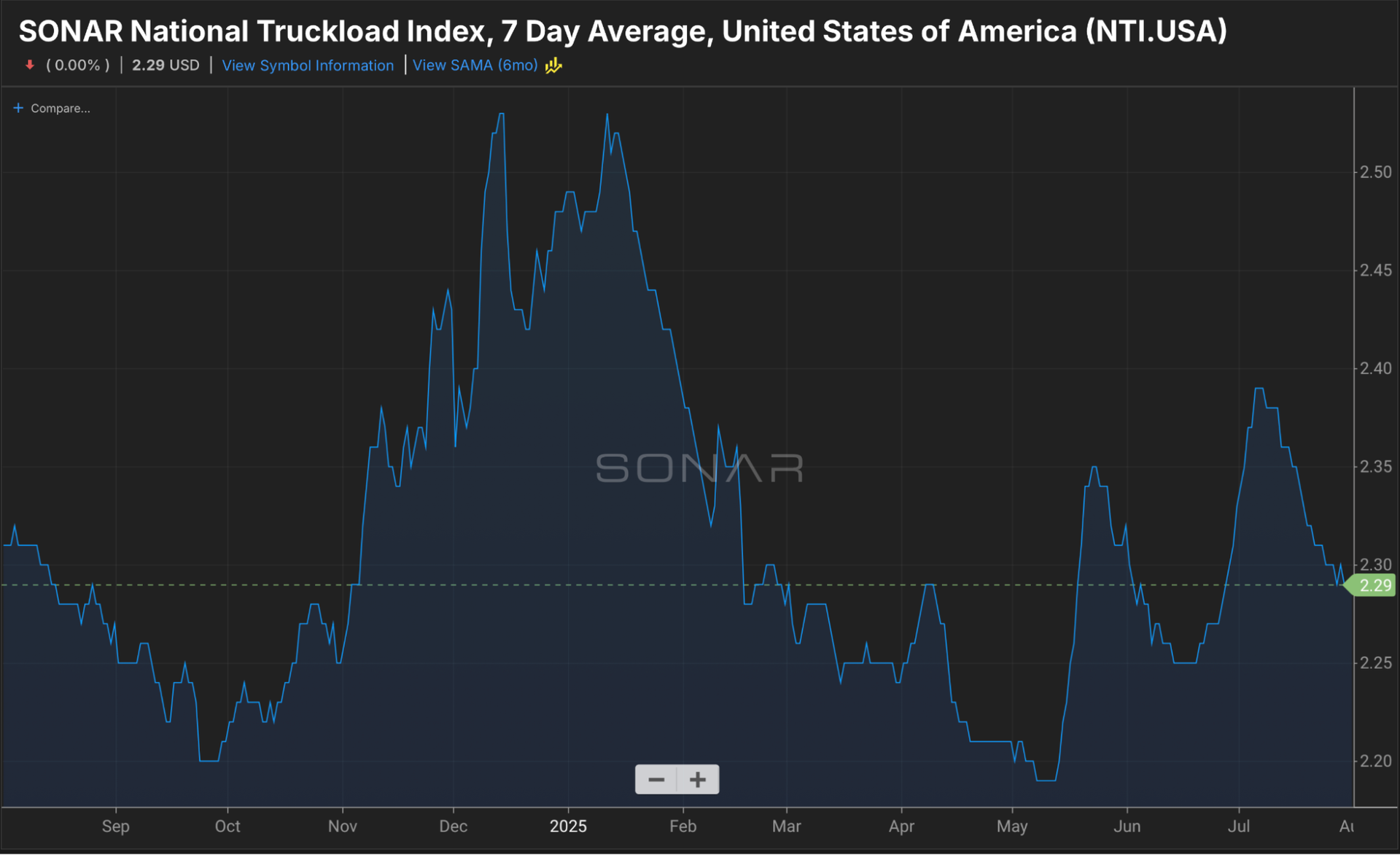

(Chart: SONAR National Truckload Index (NTI.USA). Spot rates dipped to $2.29/mile on average. That’s below breakeven for most owner-ops. The July bump is long gone—rate pressure is back on.)

|

Spot Rates Slip Again – NTI Drops to $2.29

The national average for spot van rates is $2.29/mile, which is below what most single-truck carriers need to stay profitable. While there was a small run-up in July, the correction came quickly. This week’s number means one thing: we’re back in a soft freight environment, and it’s going to take more than showing up to win.

Tactical takeaways:

- Run lanes you’ve built relationships on—not random one-and-dones.

- Use your TMS or other tools to track rate history before you pick up the phone.

- Don’t let the market dictate your rate. Let your numbers dictate your participation.

|

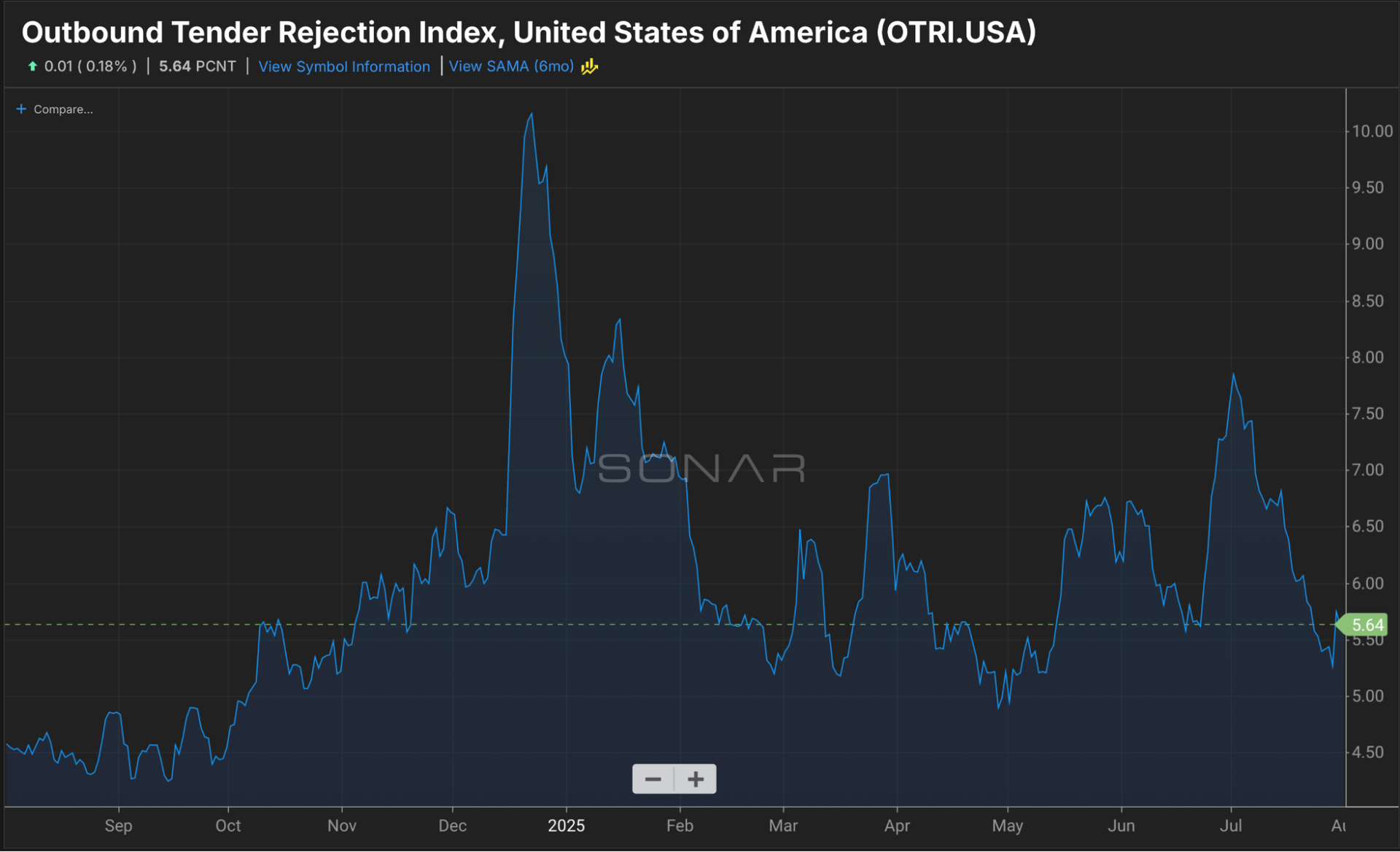

(Chart: SONAR Outbound Tender Rejection Index (OTRI.USA). Rejections slipped to 5.64%—a clear sign brokers still hold the power. Contract freight is moving without much pushback, so don’t expect spot market miracles unless you’re in a high-demand pocket.)

|

Rejections Pull Back – OTRI Falls to 5.64%

After a quick spike in early July, rejection rates cooled back down, landing at 5.64% this week. That’s not rock-bottom, but it tells a clear story: contract freight is still getting covered without much resistance. In plain terms—brokers aren’t struggling to move loads. If they aren’t fighting for trucks, it means they’ve got options. That’s not what you want to hear as a carrier.

Now, here’s what you do with that: keep a close eye on regions where rejections are rising. That’s your leverage. Look at areas in the Southeast and Midwest—if rejection rates tick up in those pockets, it means trucks are turning down contracted freight, which forces brokers into the spot market. That’s your chance to get paid more.

Don’t haul cheap out of habit. Haul smart based on rejection movement.

|

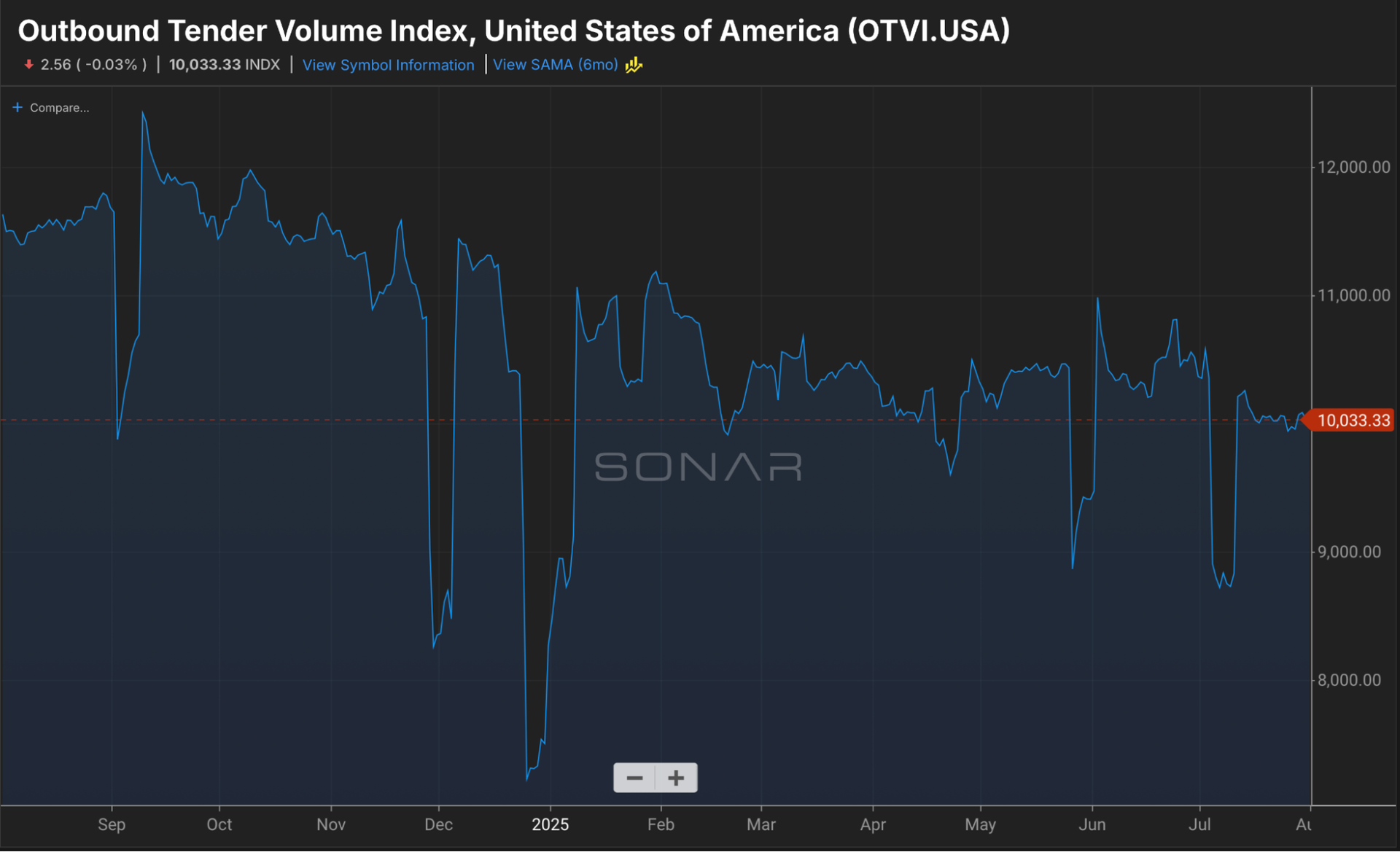

(Chart: SONAR Outbound Tender Volume Index (OTVI.USA). Volumes are stuck in neutral. At 10,033, we’re barely clinging to healthy contract levels—and spot freight remains razor thin. More trucks, fewer loads…do the math.)

|

Volume’s Holding Steady—But That Doesn’t Mean It’s Good

The Outbound Tender Volume Index (OTVI) ticked down again, resting at 10,033. That’s just a hair above the psychological “line of health” we watch (10,000), but don’t let the number fool you—volume has been bouncing in a tight range all summer, and it ain’t trending upward.

When freight volume doesn’t grow, it’s not just a neutral signal—it’s a weight on your rate power. You’re still competing with the same amount of trucks for the same—or fewer—loads. And with more large fleets chasing contract freight, the leftovers on the spot market get leaner.

So what’s the move?

- Don’t chase “leprecaun” freight—if a market looks active but rates are trash, it’s not worth it.

- Pair volume data with rejection rates. Volume alone doesn’t mean you’ll get paid.

- Know your weekly breakeven. Don’t book just to stay busy—book to stay in the black.

|

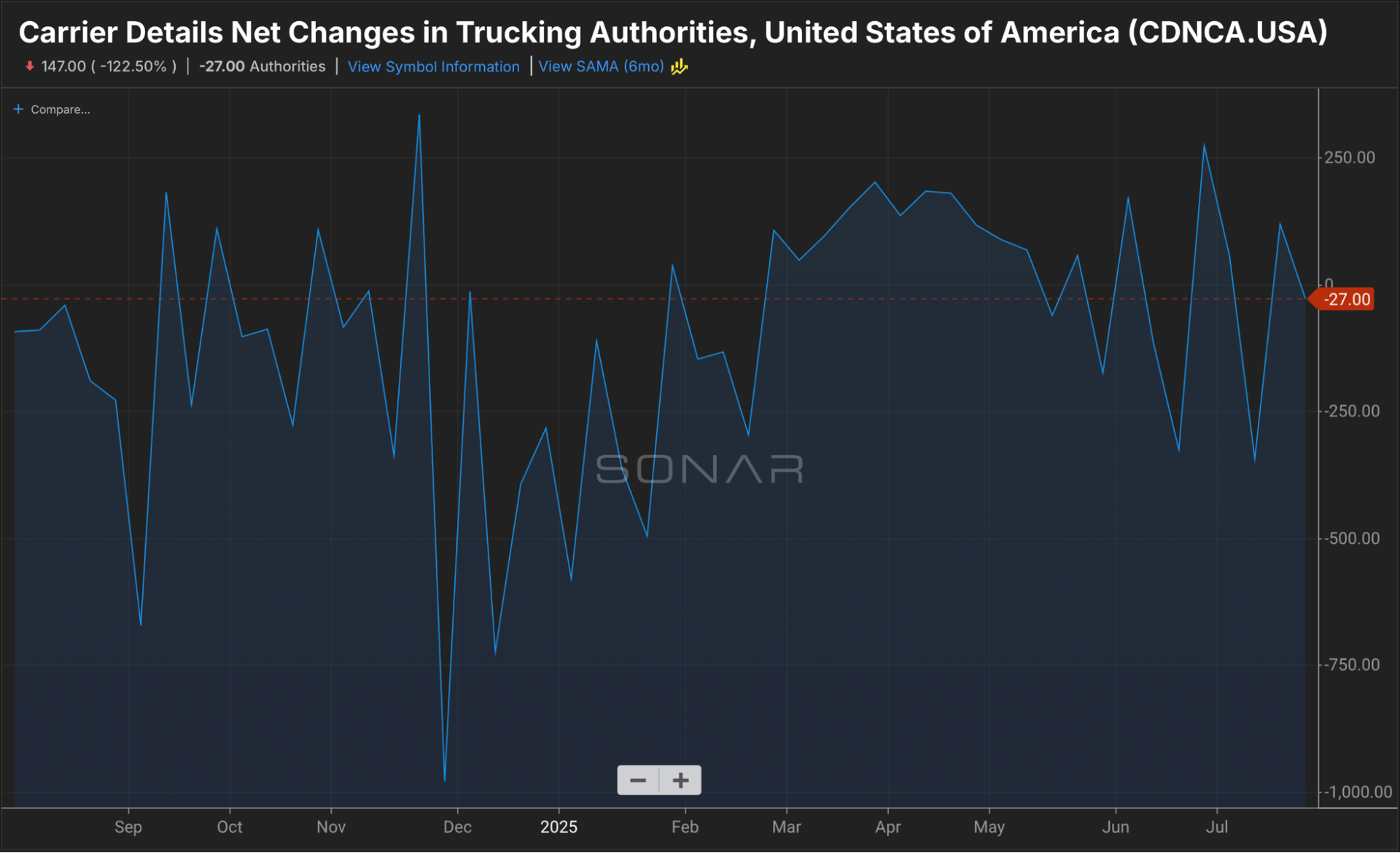

(Chart: SONAR Carrier Details Net Changes In Trucking Authorities (CDNCA.USA). More exits than entries this week—net loss of 27 authorities. Capacity’s thinning, but the shakeout ain’t over. Survive now to thrive later.)

|

Authority Changes Dip Negative – Net -27 This Week

We saw a net loss of 27 trucking authorities this week. That might sound small, but it’s part of a bigger trend—more carriers are tapping out than jumping in.

That’s a good thing for the survivors. Fewer trucks means less competition over time. But the key is to stay solvent long enough to see the shift. Surviving isn’t about suffering—it’s about adapting.

The Real Talk

The market’s not dead—but it’s cautious. If you’re hoping for a “snapback,” don’t. Build your game around what’s in front of you, not what you wish was there.

- Rejections are low, which means contract freight is being covered.

- Volume is flat, so competition is fierce.

- Diesel is up, so every mile needs to count.

- Spot rates are dipping, so margins are tight.

- Most markets are cooling off, so pick your battles wisely.

This is a process market. The ones who win are the ones with a system. Build yours around numbers, not noise.

Track your lanes. Know your breakeven. Protect your fuel costs. And don’t haul for less than you’re worth.

Keep your head in the data, and your foot on the gas—but only when it’s profitable to roll.

|

(Photo: Jim Allen/FreightWaves.Carroll Fulmer Logistics, a Florida-based trucking company that has operated for more than 70 years, is shutting down.)

|

Florida Carrier Shuts Down—400 Trucks Gone, 600 Jobs Lost

|

Carroll Fulmer Logistics, a family-owned trucking business that had been operating for 71 years with roughly 400 trucks and 1,700 trailers, abruptly ceased operations this week. About 600 employees are being laid off, with 60 days of severance promised.

The company attributed its closure to the ongoing “Great Freight Recession,” multiple costly injury lawsuits, and unrelenting pressure on margins. Despite receiving a $27 million credit line in May aimed at sustaining operations, Carroll Fulmer couldn’t recover.

Why This Matters to Small Fleets

- A 400‑truck exit is more than a data point. When a mid‑size fleet folds, it tightens freight supply in its core lanes—but can also trigger downward pressure on rates in adjacent corridors.

- It’s a warning shot. If well‑capitalized, regional legacy fleets can’t survive today’s cost environment, the squeeze on owner‑ops is even more acute.

- Insurance risk is real. Litigation costs were cited as a key factor—underscoring that one big verdict can sink a business, no matter how established.

“If the public companies are struggling with 100%+ operating ratios, many private ones are likely in far worse shape.”

What Small Carriers Should Do Now

- Track your lanes. If Carroll Fulmer served areas you frequent, expect volatility in volume or pricing as shippers find new providers.

- Vet the risk landscape. Make sure your insurance compliance, liability coverage, and MCS‑150 data are solid—big court wins hurt everyone.

- Lean in on freight relationships. Contract carriers that survive downturns have strong shipper bonds and pricing discipline baked in early.

- Calculate your exact breakeven. If even big carriers can’t operate profitably right now, you need to know your margins down to the penny.

The Bigger Bottom Line

This isn’t a ripple—it’s a wake-up. Carroll Fulmer’s shutdown is a case study in cost leverage exhaustion—from fuel and maintenance to legal exposure. If a decades-old operator can’t weather today’s market, there’s no room for optimism without action.

The restructuring of mid‑size carriers continues, and the fallout falls hardest on freelancers, small fleets, and solo operators. But small carriers with clean books, lean operations, and freight discipline can outlast turbulence.

Stability isn’t guaranteed. But for those who plan, adapt, and execute—resilience can become an advantage.

|

|

|

This Week on The Long Haul: Mid-Year Wake-Up Call – Grit, Goals, and Getting Back on Track

|

If you’ve been feeling like 2025 has been running you instead of the other way around, this one’s for you.

This week, Adam sits down with Nick Klingensmith—a seasoned freight pro, endurance athlete, and author of Selling, Inspired!—to have a no-fluff, straight-talk conversation about resetting your mindset and realigning your goals for the back half of the year.

Nick knows the grind. He’s built freight teams, crushed personal milestones, and pushed through both business and physical walls most folks would run from. And in this episode, he shares how that same discipline translates to small business leadership, carrier sales, and staying mentally sharp through the chaos.

We cover:

- Why discipline > motivation

- How to rebound from goal drift mid-year

- The mindset shift that separates leaders from passengers

- And how to sell (your service and yourself) with purpose in any market

Whether you’re running solo or managing a growing team, this episode is a gut check and a gear shift all in one.

Hit play and get back to leading from the front.

|

(Photo: Jim Allen, FreightWaves. Highway, a FreightTech company specializing in carrier identification, is entering the loadboard market with a new platform aimed at combating fraud.)

|

Highway Launches Trusted Freight Exchange – A New Era for Digital Load Boards

|

Today, Highway is officially launching its Trusted Freight Exchange (TFX)—a secured digital load board that’s only open to identity-verified brokers and carriers. This is according to an email obtained by the Playbook. If you’ve ever been stung by double brokering, ghost carriers, or bait-and-switch loads, this is the platform they say is designed to shut that all down.

Highway built its name by focusing on carrier identity and tightening the gaps where fraud likes to slip in. With TFX, they’re taking that mission a step further—building a freight ecosystem that operates on real accountability and not just DOT numbers and check calls.

What TFX Actually Is:

- A closed-loop digital exchange where only vetted brokers and verified carriers can post or book freight.

- Built-in identity protection for both sides—reducing fraud risk and protecting relationships.

- Focused on speed, control, and transparency in load transactions.

Why It Matters:

Load boards have been the Wild West for years—and small carriers usually take the bullets. This move could signal a shift away from the chaos of mass posting and toward curated, trust-based freight matchmaking. It also means brokers can stop playing detective, and carriers can stop getting punished for the bad actors in the system.

What You Need to Know:

If you’re already verified through Highway, you may start seeing new load access via TFX. If not, now’s the time to tighten your digital identity game—because platforms like this are where the industry’s heading.

In a market where who you are matters as much as what you haul, this kind of shift could finally give legit small fleets the edge they’ve been waiting for.

|

Final Word – Clarity Over Chaos

|

You don’t need a headline to tell you the market’s tight—you’re living it every day. What we’re seeing right now is a freight market that’s doing just enough to keep folks guessing. Rates hold steady just long enough to make you second guess your next move. Volume flirts with 10,000 but won’t commit. Diesel quietly creeps up week after week. And behind the curtain? Layoffs. Closures. Demand erosion.

This is where most folks get caught slipping—waiting for a loud signal that never comes. But the smart carriers, the ones who’ve lasted this long? They move on patterns, not noise.

Now is the time to double down on what matters:

- Run lean.

- Stick to profitable lanes.

- Watch the regional shifts.

- And don’t let “stable” fool you into complacency.

The ones who are still standing after the last two years didn’t survive because they got lucky—they survived because they got clear. This market isn’t going to reward hustle without a plan. It’s going to reward discipline, data, and sharp execution.

So read the signs. Trust your gut, but check the numbers too. And as always, sharpen your playbook—because the game’s still on.

That’s the mindset we bring here every week. And that’s why the Playbook isn’t about hype—it’s about readiness.

Let’s keep building that edge. Mile by mile. Strategy by strategy.

We’ll see you out there.

|

|

|

|