Language Rules Are Back, and Drivers Are Getting Parked

|

|

|

The Market’s Not Broken – It’s Just Picking Sides

|

|

|

(A Quick Note From Us: You’ll notice the newsletter’s got a sharper look and tighter flow this week. We’re streamlining sections so it’s easier to read on the go, with the same depth you count on — just faster to digest. Let us know if you like the new format.)

|

|

|

Language Rules Are Back, and Drivers Are Getting Parked

|

The FMCSA’s renewed push to enforce English-language proficiency rules has quickly changed the landscape on U.S. highways. In just over a month since enforcement resumed on June 25, more than 1,500 truck drivers have been pulled off the road for failing to meet federal English-language requirements. And here’s the part that’s raising eyebrows — almost every single one of these drivers (99%) was working for a U.S.-based carrier.

Let’s unpack what’s going on. This isn’t a new rule. The requirement for drivers to be able to read and speak English well enough to communicate with the public, understand road signs, answer official questions, and make written entries in reports has been on the books for decades. But in 2016, active enforcement slowed after policy shifts deprioritized it. That changed in late May, when Transportation Secretary Sean Duffy announced that federal and state partners would begin testing for compliance again.

Since then, Commercial Vehicle Safety Alliance (CVSA) inspectors have been required to conduct initial roadside interactions in English. If there’s any indication a driver can’t understand instructions, inspectors move to a formal proficiency assessment, which may include reading road signs and answering inspection-related questions. Four violation categories cover everything from inability to converse with officials to not understanding traffic signage.

The numbers reveal some telling patterns. The Western region has seen the most violations (412), followed by the Southern (364), Midwestern (273), and Eastern (163) regions. These are not evenly distributed — certain states in these regions, particularly along major freight corridors, are emerging as hot spots for enforcement. In many cases, the violations are being written not against drivers from abroad, but against domestic carriers employing foreign-born drivers without adequate training in English.

For small carriers and owner-operators, this enforcement wave is more than a compliance headline — it’s an operational challenge. It also signals that regulators are moving toward stricter interpretations of existing safety rules — and that could extend into other areas of compliance.

Publicly, Duffy has framed this as a safety initiative. “If you can’t read or speak our national language — ENGLISH — we won’t let your truck endanger the driving public,” he said. Supporters see this as a commonsense safety measure, while critics question whether the industry is equipped to adapt without worsening the driver shortage in certain sectors.

Bottom line — the FMCSA is showing it’s willing to enforce long-standing rules that have been ignored for years. For carriers, this is a reminder to audit your own driver qualifications now, before you get caught short in an inspection. And for the industry as a whole, it’s another sign that enforcement priorities can shift quickly, reshaping the driver pool and tightening capacity in certain markets overnight.

|

|

|

Your feedback helps FreightWaves understand the needs of the market. By analyzing fleet size data, we can see trends and adapt our offerings to provide better tools, resources, and support for all our readers, from owner-operators to large carriers.

|

|

|

(Photo: Jim Allen/FreightWaves. Fuel taxes are inching up in states during a time when things are already tight for most.)

|

Fuel Taxes Shift in 13 States – Here’s What It Means for Your Bottom Line

|

July 1 brought mixed news at the pump. Ten states raised their fuel taxes, while three saw small decreases—proof that your cost per mile can change overnight depending on where you’re fueling.

For truckers running through Connecticut, Kentucky, and Maryland, there’s a little relief. Connecticut cut diesel taxes by 3.5 cents to 48.9 cents per gallon, Kentucky dropped 1.4 cents to 22 cents, and Maryland shaved a fraction off to 46.75 cents. Those changes won’t rewrite your budget, but they can stack up for carriers with regular lanes through those states.

Everywhere else, the trend is the opposite.

- California now leads the pack on diesel taxes—97.1 cents per gallon once you combine the excise tax and recent increases. Gas taxes there also jumped, and efforts to pause the hikes failed.

- Washington State made one of the biggest moves, raising diesel to 58.4 cents and gas to 55.4 cents, with the revenue aimed at covering transportation budget shortfalls.

- Illinois, Indiana, Missouri, Nebraska, Virginia, Rhode Island, Alabama, and Mississippi all saw smaller bumps—most tied to inflation adjustments, road construction funds, or multi-year tax increase schedules.

For carriers, this isn’t just about cents per gallon—it’s about where you buy fuel and how you plan routes. A run through California or Washington now comes with a much higher tax bill, while fueling in Kentucky before you cross state lines could save you real money over time.

Tactical takeaway:

- Keep a running list of states with the highest diesel taxes.

- Adjust your fueling strategy so you’re topping off in lower-tax states when possible.

- Factor these changes into your cost-per-mile calculations immediately—waiting until the monthly books are done means you’re already behind.

The fuel market itself is unpredictable right now, but tax hikes like these are baked in for the year. If you know where they are and plan for them, you keep more of your rate where it belongs—in your pocket.

|

|

|

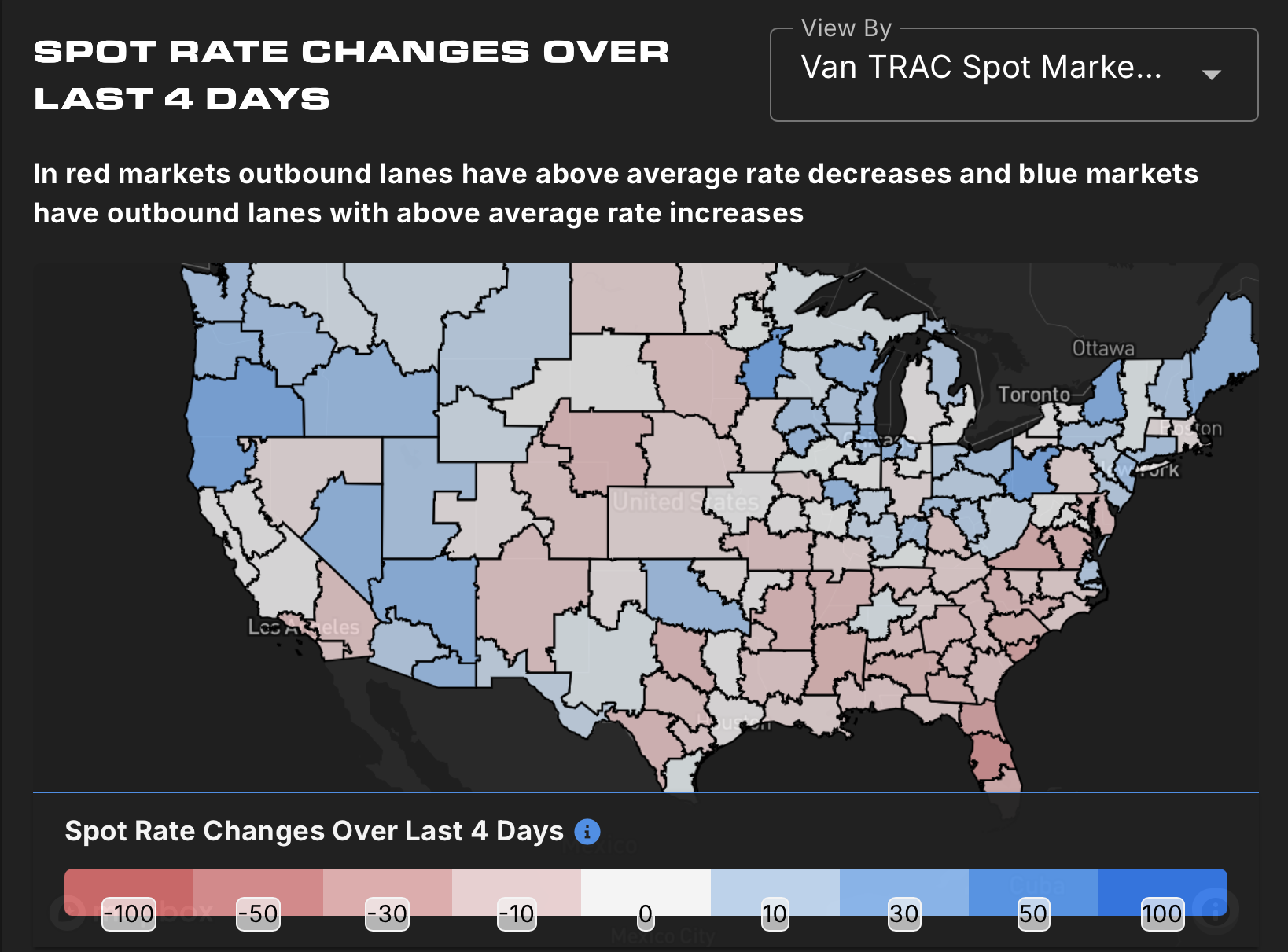

(Source: SONAR Spot Rate Changes Over Last 4 Days (Van TRAC Map). Red is bad news. Most outbound lanes across the Southeast, Midwest, and Central U.S. saw rate drops. Blue pockets are few and far between—know before you go.)

|

Market Conditions – What You Need to Know Before You Start Clicking

|

If you’re booking freight off the load board right now, you can’t just look at the posted rate and hit “book.” The market’s not dead, but it’s not feeding everybody either. Volumes are flat, rejections are only creeping up a little, and the rate map looks like a checkerboard—some spots are paying better, others are ice cold.

Fuel’s still sitting high enough to eat into your take-home, and we just had a bump in new carriers getting their authority. That means more trucks chasing the same freight you’re looking at. In plain English? The pie isn’t getting bigger—more folks are just cutting slices.

This is a week where you’ve got to be smart. Don’t waste half your day chasing loads in a dead market. Find the pockets where brokers can’t cover, hold your number, and don’t be afraid to deadhead if it gets you to a better-paying lane. Every mile you run without a plan is money you can’t get back.

The country’s split right now. Blue zones are seeing some life in rates, red zones are cooling off. If your home base is sitting in a red market, don’t waste your time trying to squeeze blood from a stone — get yourself to a blue market before you burn your week running cheap.

Think like this:

- Start in a blue market, grab a solid outbound.

- Take a light-paying backhaul just to get you back to the blue.

- Keep repeating.

That’s how you keep your weekly average up instead of running four “meh” loads in a row.

|

|

|

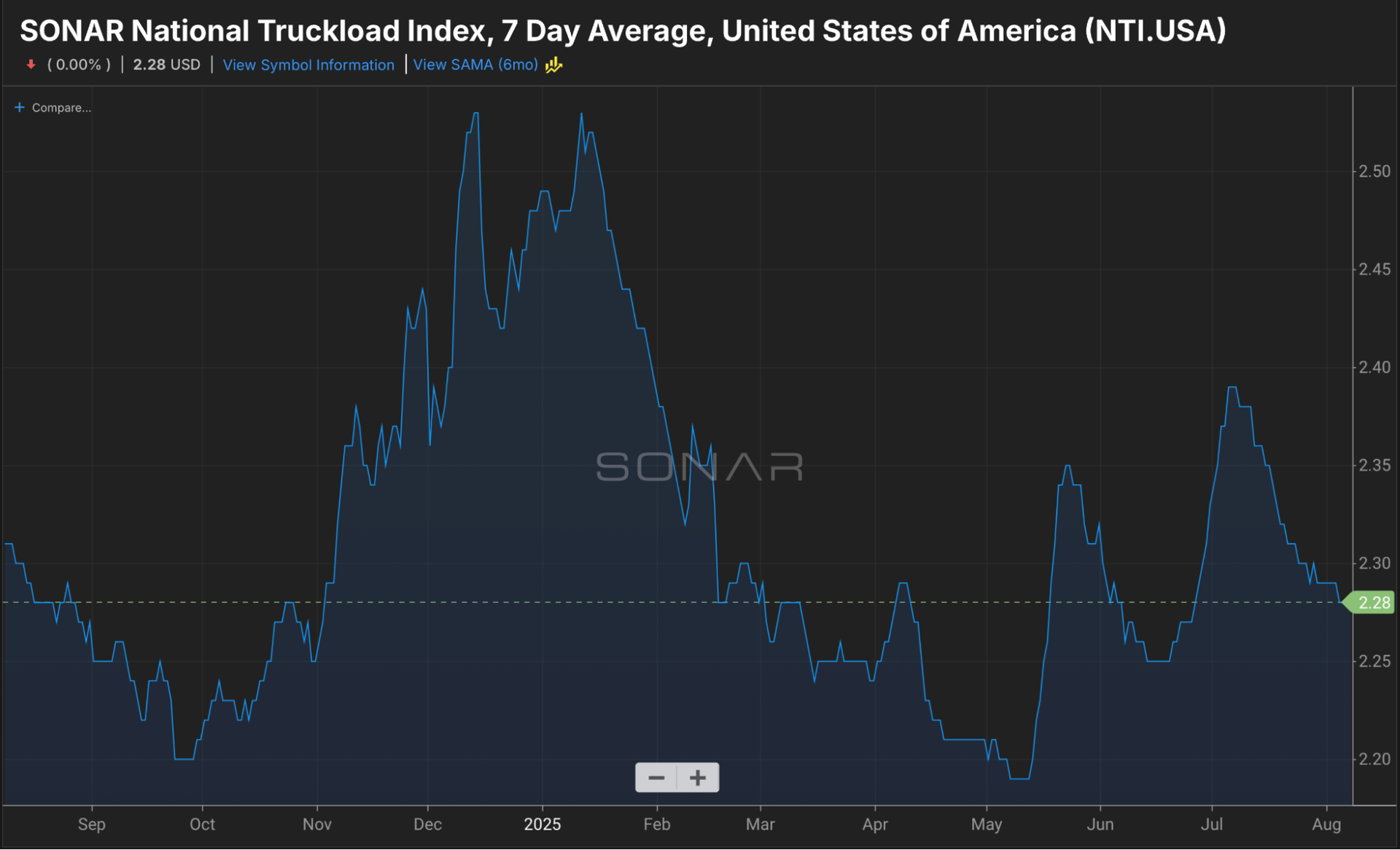

(Chart: SONAR National Truckload Index (NTI.USA). Spot rates are stale at $2.28/mile on average.)

|

National Truckload Index (NTI) – Holding at $2.28

We’re sitting at $2.28 on the national average. That’s not a bad number if you’re keeping your miles tight and fuel efficient. But here’s the reality: if you’re booking out of the wrong market, you’ll be staring at $1.80s real quick.

The play? Don’t chase freight that looks busy but has no rate power. Pair the NTI with the spot rate map — if the average is $2.28, you should be aiming for $2.50+ in your lanes to cover fuel and still take something home.

|

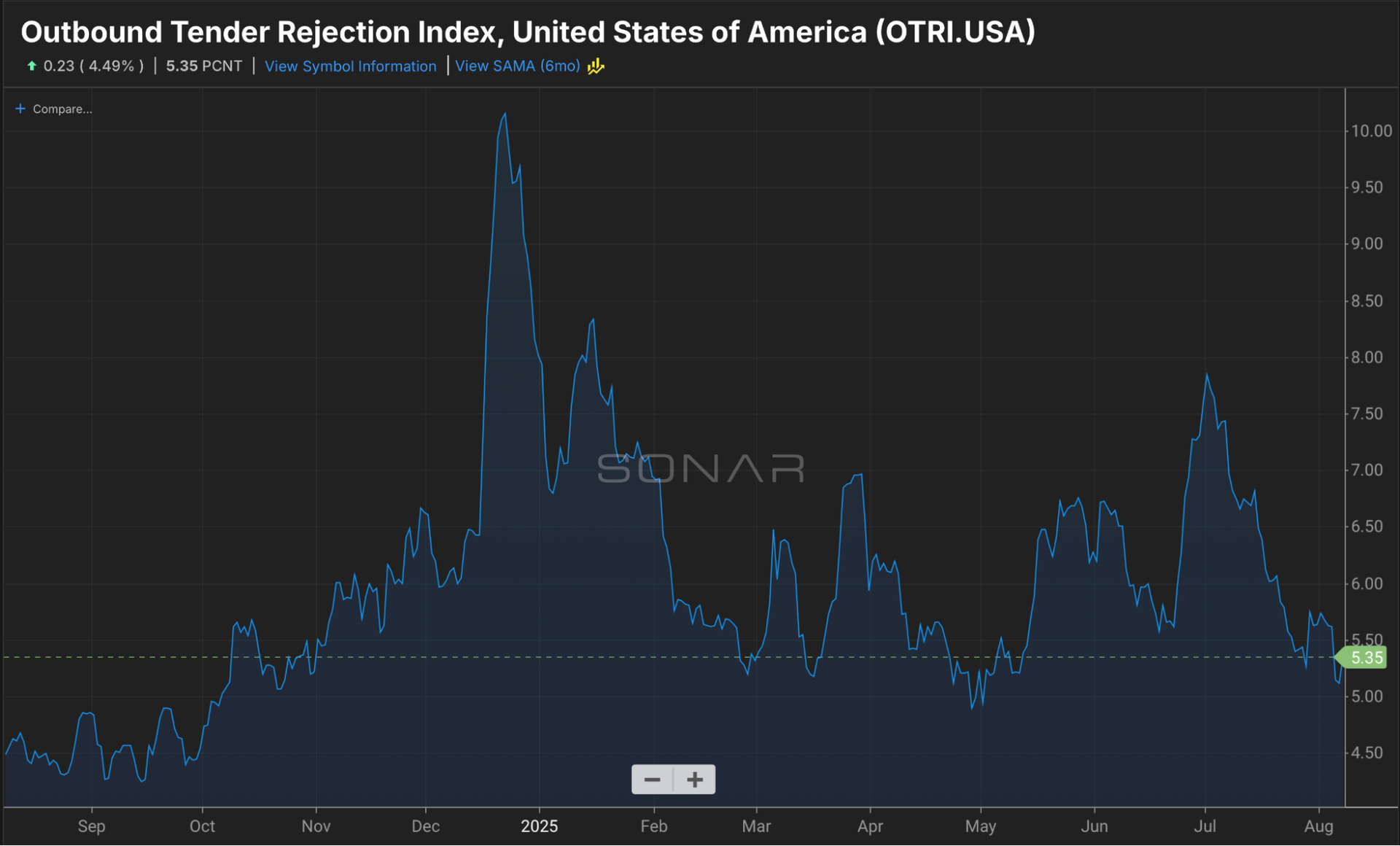

(Chart: SONAR Outbound Tender Rejection Index (OTRI.USA). Rejections are holding just above 5%)

|

Outbound Tender Rejection Index (OTRI) – Sitting at 5.35%

Rejections ticked up a hair to 5.35%, but don’t let that fool you — brokers still have plenty of coverage in most markets. This isn’t a “rates are about to skyrocket” number. What it means for you: if you’re seeing 2–3 brokers fighting for the same load, you’ve got room to push back a little. But if you’re just taking whatever pops up first, you’re leaving money on the table.

The move right now? Watch specific hot spots, not the national average. A bump in rejections in the Southeast or Midwest can mean the difference between $2.20 and $2.70 a mile on the same lane. If you’re working out of a flat market, you’re going to fight harder for every penny.

|

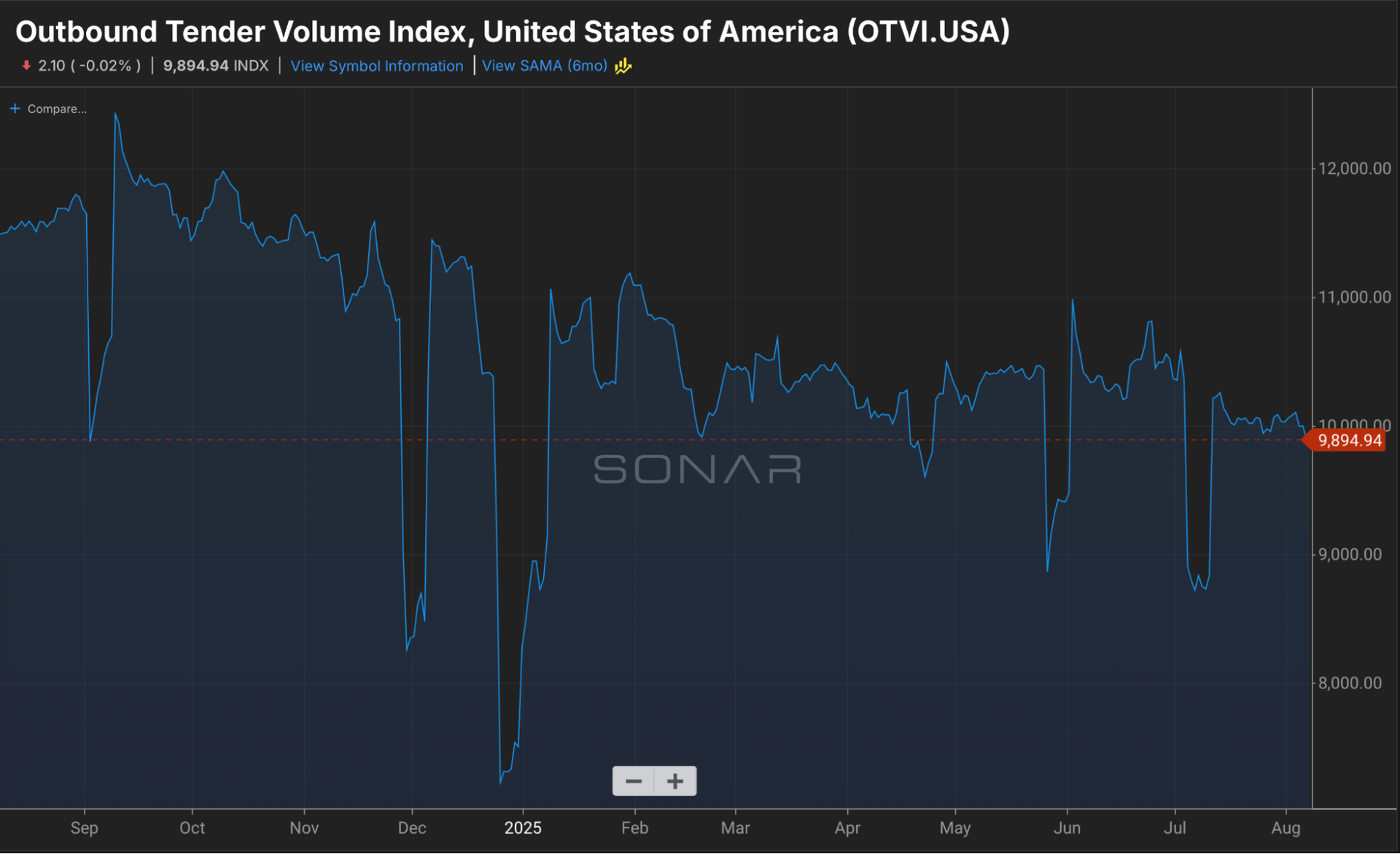

(Chart: SONAR Outbound Tender Volume Index (OTVI.USA). Volumes are stuck.)

|

Outbound Tender Volume Index (OTVI) – 9,894 and Flat

Volume’s holding at 9,894. That’s not a collapse, but it’s not the push we need to see either. Translation: there’s freight out there, but not enough to feed every truck. If you’re running on the spot market, this means you’ve got to pick your battles, as there are fewer to pick. High-volume markets are better for keeping your wheels turning, but you’ve still got to check how competitive they are. Pair this with rejection rates — low volume and low rejections? Skip it. Low volume but high rejections? That’s where you can push rates.

|

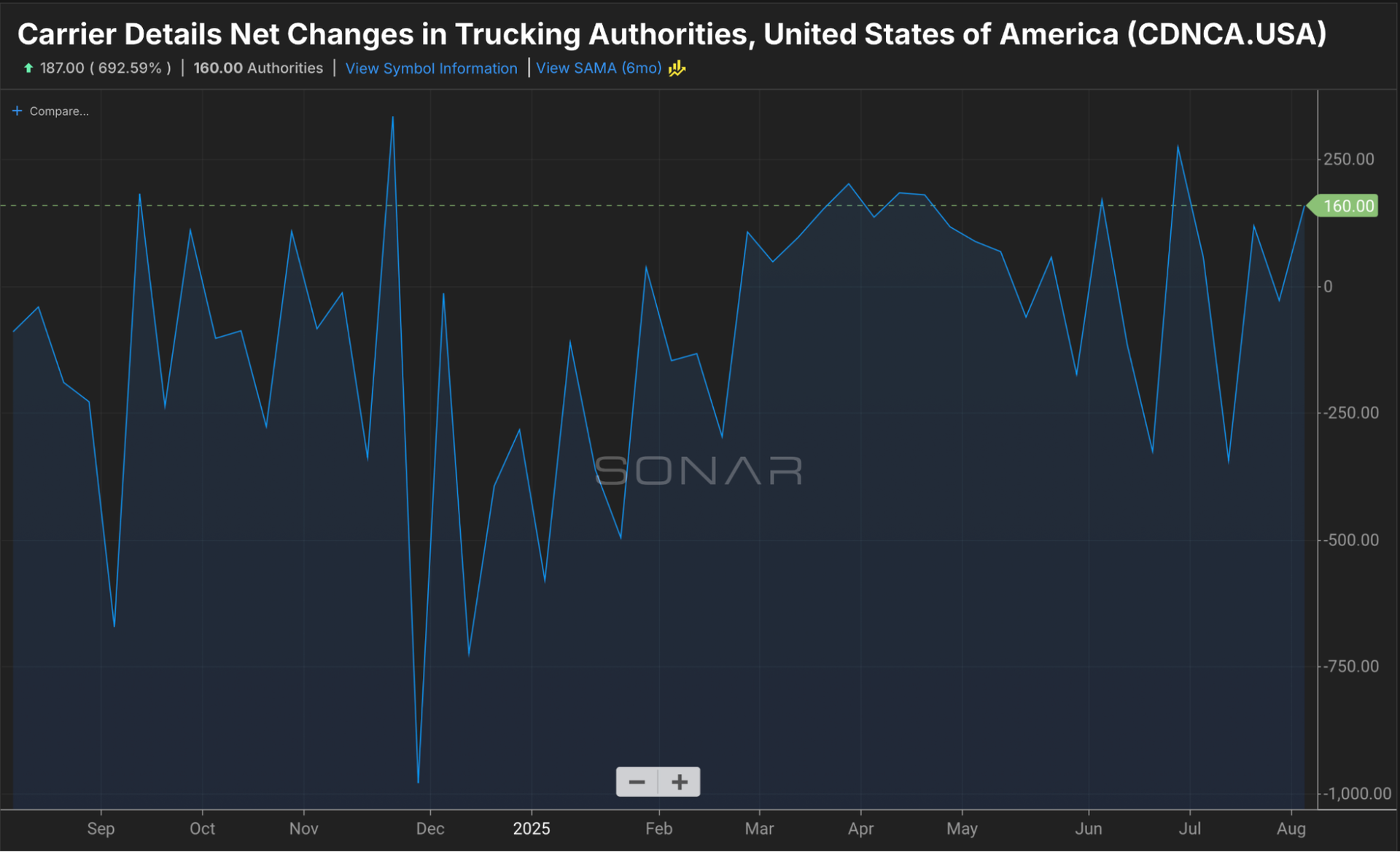

(Chart: SONAR Carrier Details Net Changes In Trucking Authorities (CDNCA.USA). )

|

Authority Changes Dip Negative – Net -27 This Week

We just had 160 more carriers get their authority than lose their authority. That’s 160 more trucks competing for the same freight you’re clicking on. It’s not a massive surge, but it’s enough to feel in soft markets. Every new truck means more competition for the “good” loads, especially those posted early in the day.

|

(Photo: Jim Allen/FreightWaves. For the first time in years, used truck pricing is on the rise.)

|

Used Truck Prices Tick Up for the First Time in Over Two Years

|

For the first time since late 2022, the average price of a used Class 8 truck has gone up instead of down. June’s numbers came in at $60,324—about 10% higher than the same time last year and 6% higher than May. That jump might not sound huge, but after two and a half years of steady decline, it’s a clear signal that the market for late-model used trucks is shifting.

Why the bump? A few things are in play:

- The trucks moving through the used market right now are newer and have fewer miles—around 403,000 on average, compared to 423,000 last year.

- Some dealers are actively going back through their customer lists and working deals with buyers who are in a position to make a move.

- With new truck sales slowing and production at big OEMs hitting snags, buyers who can’t get fresh inventory are looking harder at clean, late-model used iron.

Sales volume was up 9% year-over-year in June at 22,600 units, but about flat compared to May. The auction market is also showing normal mid-year movement, with more 3- to 5-year-old sleepers hitting the lanes as fleets cycle equipment.

For smaller carriers, the key takeaway isn’t just that prices went up—it’s why. If OEMs keep struggling to deliver new trucks, used prices could keep creeping up, especially for well-spec’d, low-mileage units. On the flip side, freight demand is still soft, which means you don’t want to overextend just to grab a truck you think you need.

Tactical takeaway: If you’re in the market, move quickly on good-spec, clean-title units that fit your lane mix, but avoid stretching your budget on price alone. Supply could get tighter, but the freight side hasn’t caught up yet—so protect your cash flow before chasing the upgrade.

|

|

|

This Week on The Long Haul – Todd Waldron from Truckstop

|

In this week’s episode, we sit down with Todd Waldron, a guy who knows the freight game from the inside out. Before joining Truckstop, Todd spent over 17 years in transportation and logistics, running the playbook in carrier procurement, business development, and operations — including time as CEO of a Minnesota-based carrier.

We get into the real talk about what carriers need to understand if they want to win more freight in today’s market:

- How brokers really view small carriers — and how to stand out.

- Why some carriers get the “good freight” while others keep getting ghosted.

- The role technology plays in leveling the playing field, especially for the one-truck and five-truck operations.

- The mistakes carriers don’t know they’re making until they lose the lane.

This isn’t theory — it’s straight from someone who’s been on both sides of the desk. If you want to understand how to position yourself for better rates, better freight, and better relationships, you don’t want to miss this one.

|

Final Word – When the Rules Tighten, the Smart Get Stronger

|

The lead story this week made one thing clear — rules are tightening, and drivers who can’t meet them are getting parked. Whether it’s language proficiency checks, higher fuel costs, or tighter freight competition, the market is quietly drawing a line between those who run like professionals and those who just drive.

The data this week doesn’t scream, but it doesn’t have to — it’s telling you exactly where the cracks and opportunities are. If you’re paying attention, you’ll see where you can step in and win business while others are getting pushed out. That’s not luck, that’s strategy.

Don’t wait for the market to turn in your favor. Position yourself in the lanes where you have leverage, keep your costs in check, and protect your margin like your business depends on it — because it does.

In this market, the ones who last aren’t the ones waiting for better days. They’re the ones making today work.

That’s the mindset we bring here every week. And that’s why the Playbook isn’t about hype—it’s about readiness.

Let’s keep building that edge. Mile by mile. Strategy by strategy.

We’ll see you out there.

|

|

|

|