Can Derek Barrs Rebuild What the FMCSA Let Fall Apart?

|

|

|

|

|

NEWSLETTER BROUGHT TO YOU BY — SIRIUSXM

|

SiriusXM keeps truck drivers informed and entertained with 24/7 music, sports, and more. Hear all your SiriusXM favorites on every haul for $6.06/month. Sign up.

|

|

|

UPS, Senate Talk, and What STL Means for You

|

|

|

(Photo: Jim Allen, FreightWaves. As freight rolls on, policy decisions made in Washington continue to shape what’s next for small carriers)

|

|

|

Can Derek Barrs Rebuild What the FMCSA Let Fall Apart?

|

For the first time in nearly two years, the FMCSA may finally get a permanent administrator.

Derek Barrs, former Florida Highway Patrol commander and a longtime voice for highway safety, is now officially in the hot seat. His Senate hearing wrapped this week, and while his nomination hasn’t sparked fireworks across cable news, the outcome could matter more than most in Washington realize — especially for small carriers who’ve been left unprotected by weak enforcement, rising fraud, and a regulator with no real teeth.

Let’s be clear: this isn’t just another suit filling a seat.

Barrs is the first true enforcement-focused nominee in years — a guy who came up through the ranks, not the revolving door. His background isn’t just policy. It’s boots-on-the-ground enforcement, with decades of firsthand experience in roadside inspections, crash investigations, and direct oversight of commercial motor vehicle compliance.

But here’s the real question:

Will Barrs be able to turn that real-world expertise into real results at FMCSA — or will he get swallowed by the same bureaucratic sludge that’s kept the agency spinning its wheels for years?

What He Said, and What Was Missing

During the hearing, Barrs said all the right things:

- Prioritize crash prevention

- Protect drivers from coercion

- Address fraud and double brokering

- Expand truck parking

- Push ELD compliance and improve safety tech

But saying, isn’t doing. And for small carriers, the problem isn’t the lack of rules — it’s the lack of follow-through.

The FMCSA has become a regulatory ghost town:

- No permanent leadership for nearly two years

- A fraud crisis that’s exploded without meaningful crackdown

- Speed limiter debates that drag on with no direction

- A double brokering epidemic with more guidance than enforcement

And now? The guy being asked to fix it all is walking into an agency that’s both understaffed and under fire.

Why Small Carriers Should Care

Barrs might be the best nominee we’ve seen in years — but his success will depend on one thing: how fast he can bring enforcement consistency back to the ground level.

Because right now:

- Unsafe carriers are slipping through loopholes

- Brokers and shippers are losing faith in carrier vetting

- Owner-ops are paying the price through insurance hikes, rate suppression, and fraudulent competition

If Barrs brings his roadside background to the national stage — and builds real tech infrastructure to back it — he could be the first FMCSA head in years to actually move the needle for the right people.

But if he gets trapped in advisory panels and slow-walked processes, it’ll be more of the same: big speeches, no change, and small carriers footing the bill.

The Bottom Line

Derek Barrs knows the enforcement game. He’s walked the shoulder. He’s seen the wreckage. But now he has to walk the line between political leadership and practical reform.

And the clock’s ticking.

Because the longer this agency stays reactive instead of proactive, the smaller fleets are left to fend for themselves in a broken compliance landscape. Let’s hope Barrs brings the boots, not just the briefcase.

Because out here? We don’t need another bureaucrat.

We need a bulldog.

|

|

|

(Photo: Jim Allen/FreightWaves. Tariffs aren’t just policy—they’re pressure. Proposed import penalties on China, Mexico, and beyond could choke critical freight volumes across ports, borders, and manufacturing lanes in early 2025. For small carriers, the freight won’t wait. The question is—will you be ready when it shifts?)

|

Del Monte Fallout Gets Uglier – Saddle Creek Left Hanging

|

We covered this one a few weeks ago when news first broke: Del Monte Foods’ transportation arm had filed for Chapter 11, leaving a trail of unpaid carriers and unsettled freight contracts. But the latest court filings just pulled the curtain back even further — and it’s not looking good for small fleets that did business under the Del Monte name.

This week, we learned that Saddle Creek Logistics, a major 3PL and transportation player, is now on the hook for a $1.28 million unsecured claim. That’s not pocket change — and it’s just one piece of a much bigger mess.

Here’s the update that matters:

Del Monte’s web of subcontracted freight, transportation services, and distribution work was bigger than it looked. Now that the dust is settling, it’s becoming clear that several brokers, carriers, and logistics partners are facing deep losses, with little chance of full recovery.

This bankruptcy isn’t just an isolated food industry story. It’s a cautionary tale for any small carrier doing contract freight with a brand-name customer, especially when third-party intermediaries are in play.

Why This Hits Small Carriers Hardest

- Unsecured claims get paid last — if at all. That means if you hauled loads for Del Monte or their intermediaries without tight payment terms, you may be out for good.

- Payment delays can tank a small fleet. If your invoices went 30–60 days unpaid, and now the debtor is in court, you’re burning cash with no return.

- This exposes a common vulnerability: when a shipper contracts through multiple layers of logistics firms, it’s easy for the small carrier at the end of the chain to get left holding the bag.

If Saddle Creek, with its legal team and financial leverage, can’t get paid in full — what chance does a three-truck operation have?

What This Teaches Us

Vet your customers. Don’t let the logo fool you. Just because the freight comes from a recognizable name doesn’t mean the money’s clean all the way through. Del Monte’s transportation arm was not the same entity as Del Monte’s consumer products business. And when that distinction matters — it matters big.

If your factoring company is rejecting paperwork or slowing approvals, it might not just be nitpicking. It could be your early warning system. Trust your gut, double-check rate cons, and know exactly who’s paying the invoice — not just who’s shipping the fruit.

Bottom line: a big name doesn’t mean a safe load. And in a freight market this tight, payment risk is just as real as weather, breakdowns, or low rates.

|

|

|

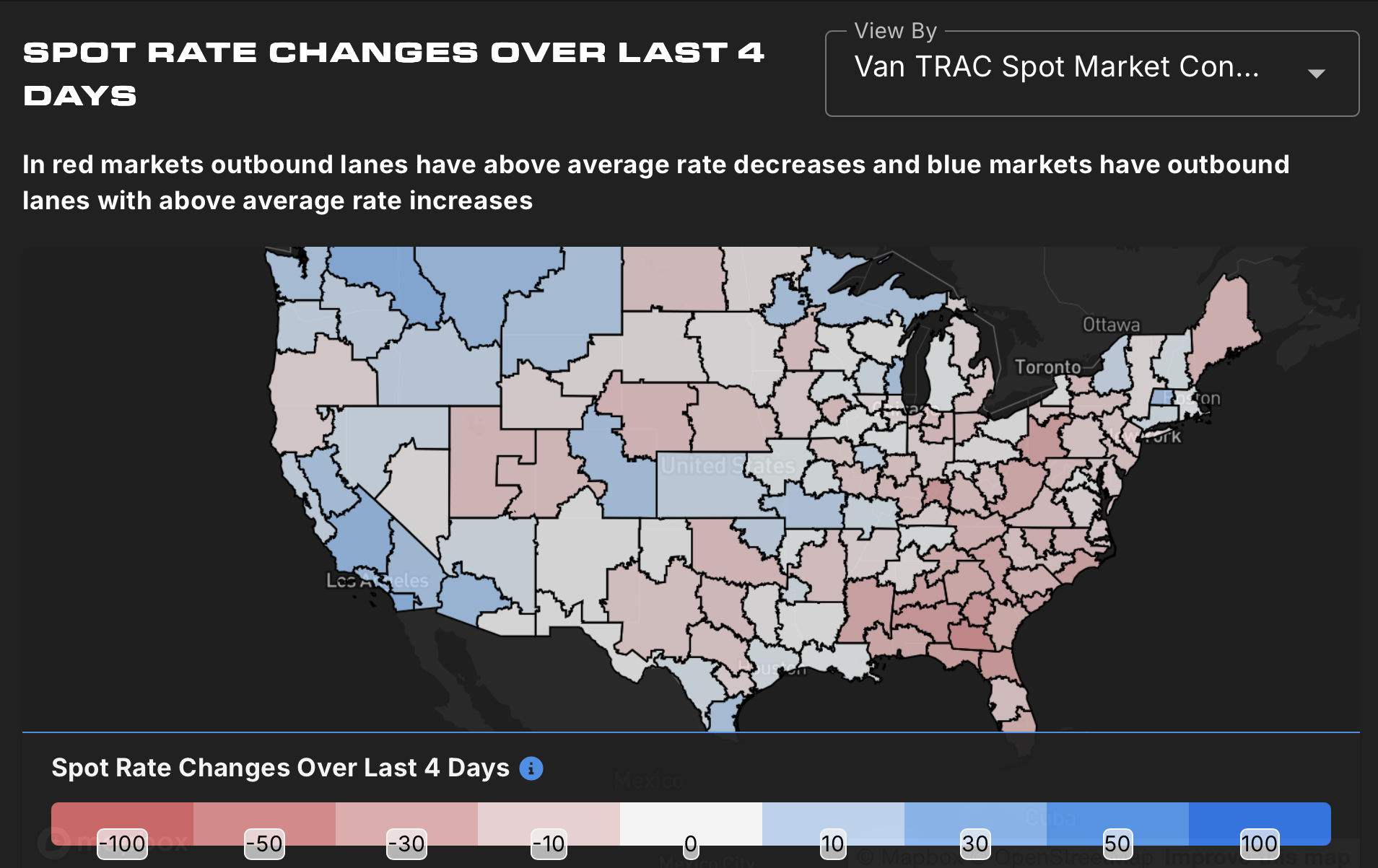

(Source: SONAR Spot Rate Changes Over Last 4 Days (Van TRAC Map). Rate shifts vary wildly by region—Southeast softens while parts of the Midwest and Southwest see mild boosts.)

|

Market Conditions Roundup – Stability Is Not Strength – Week of July 25, 2025,

|

You might look at this week’s data and say, “Well, at least it’s not worse.” But if you’re a small carrier relying on freight to feel consistent again—don’t confuse sideways motion with progress.

Spot rates over the past 4 days are telling a familiar story: red in the Southeast, pink in the East, and only minor blue pockets in the West. That’s your cheat sheet for rate leverage.

If you’re running the Carolinas, Georgia, or Florida—expect rate softness. Conversely, if you’re in SoCal or northern Rockies, some routes are still experiencing upward pressure.

Pair this data with your ELD tracking and dispatch records. Are your deadhead miles creeping up? Are your drivers sitting longer between loads? If so, you’re likely in the wrong zone—or you’re not adjusting quickly enough.

Let’s break it down chart by chart so you can move sharper this week.

|

|

|

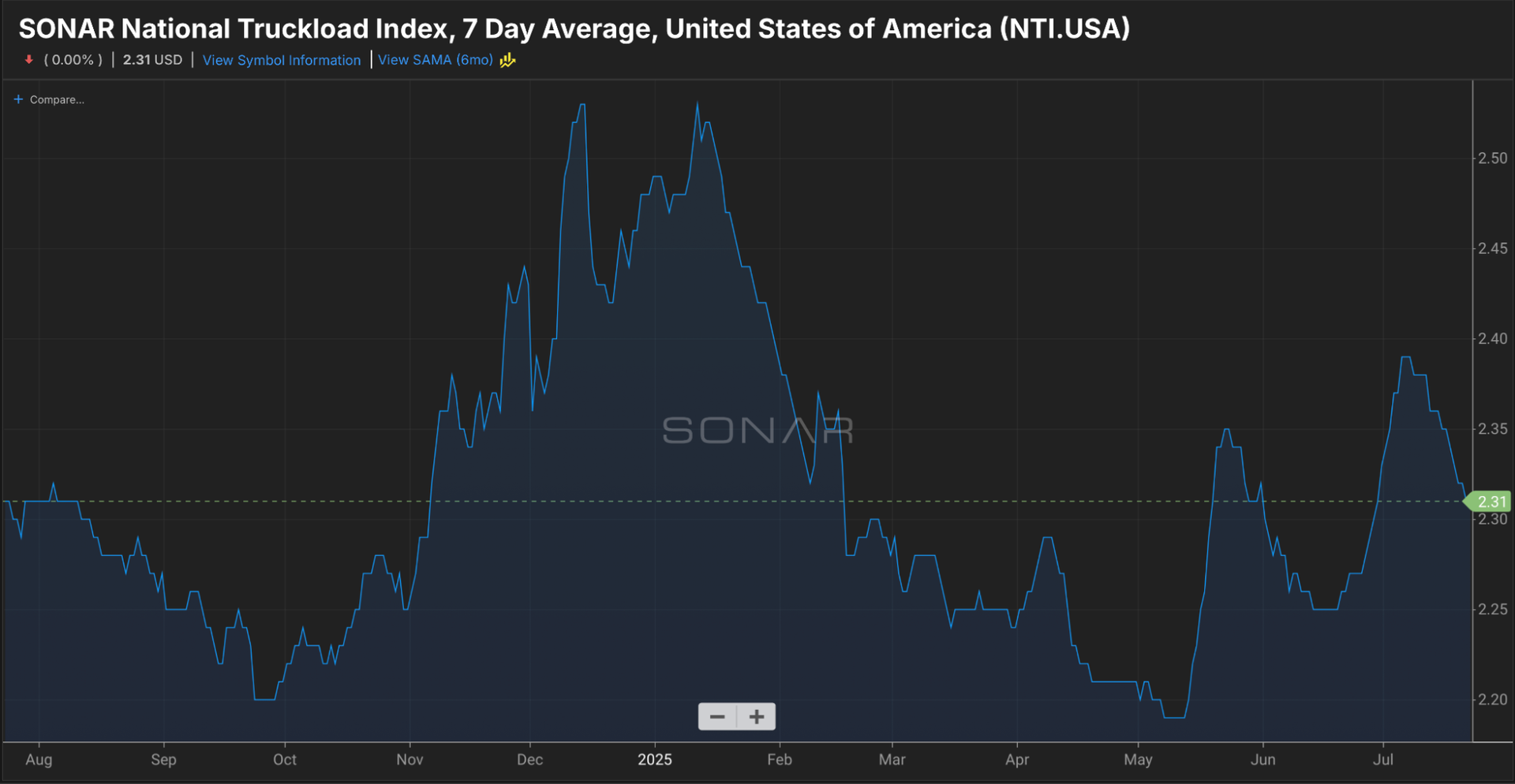

(Chart: SONAR National Truckload Index (NTI.USA). Spot rates are losing steam—now at $2.31/mi as seasonal pressure fades and volume steadies.)

|

Spot Market Cooling – NTI Drops to $2.31/mi

The National Truckload Index is now trending down again after a summer surge, currently sitting at $2.31 per mile. That’s a signal worth watching—especially for those chasing short-term highs.

Rates in early July saw a nice seasonal lift, but the momentum has cooled quickly. We’re now entering the late-summer plateau where rates tend to float sideways at best, and dip fast when fuel or capacity shifts.

If your breakeven is north of $2.00, the profit margin is getting slim—fast.

It’s critical now to pair rate chasing with strict cost control. This isn’t the time to gamble on high-mileage, low-margin loads.

You’re going to see market-specific spikes (Chicago, Dallas, Atlanta), but they’re short-lived. Stack your week with discipline, not desperation.

|

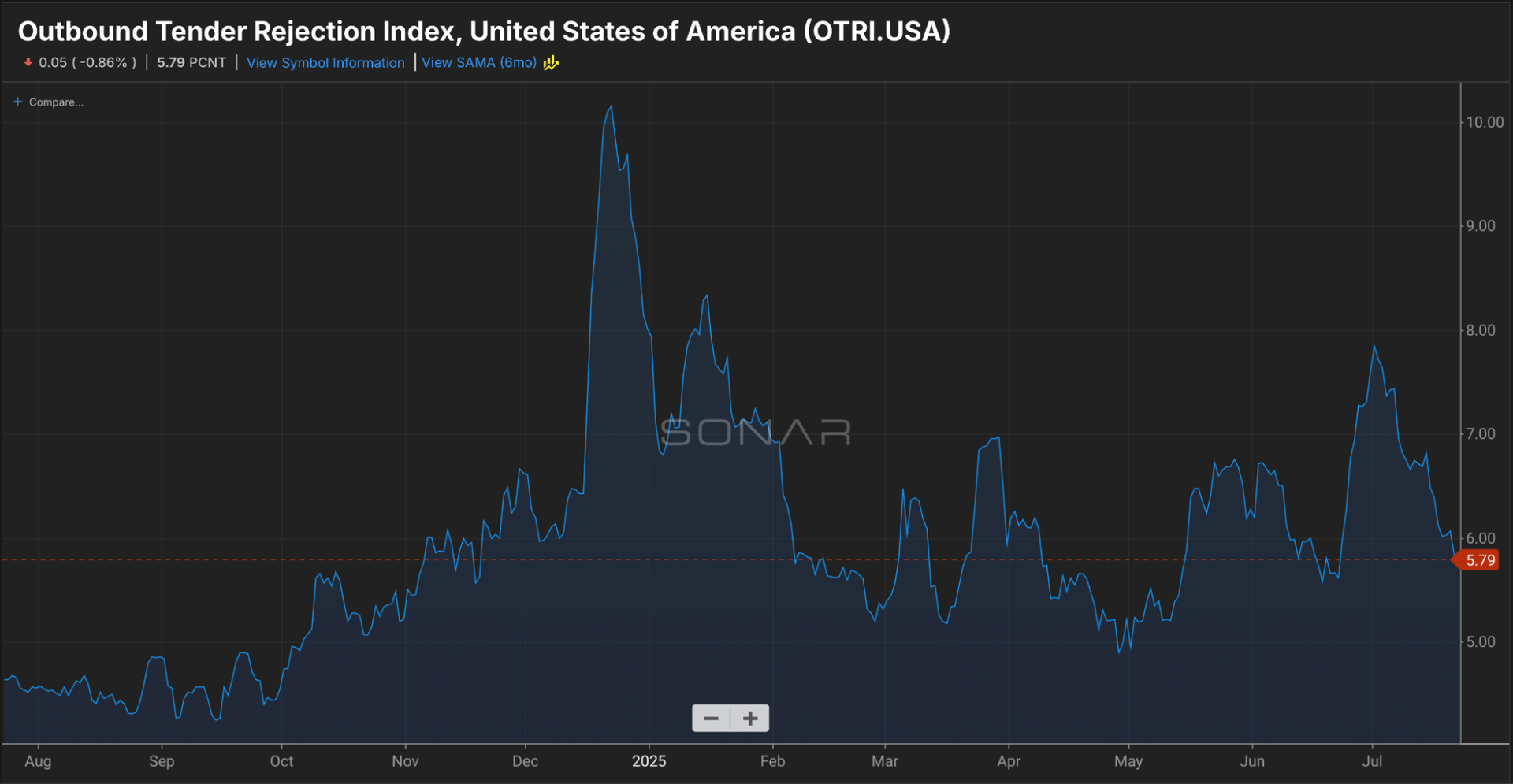

(Chart: SONAR Outbound Tender Rejection Index (OTRI.USA). Rejections continue their steady slide to 5.79%, signaling softer contract coverage pressure across the board.)

|

Rejections Pull Back – OTRI Slides to 5.79%

After peaking near 8% earlier this month, the Outbound Tender Rejection Index (OTRI) continues to back off—now sitting at 5.79%. That’s not just a dip—it’s a clear sign that the recent rate pressure is easing. The bounce we saw post-July 4th is fading, and contract freight is back to being widely accepted.

For small carriers, this means brokers are no longer scrambling. If you’ve been holding firm on rates, expect more pushback unless you’re sitting in a rejection-heavy market (parts of the Midwest still show some strain). Anything under 6% generally means broker leverage is creeping back in.

Now’s the time to sharpen your value prop, not your rate floor.

|

(Chart: SONAR Outbound Tender Volume Index (OTVI.USA). The index is sitting just above 10,000—neutral territory, but fragile as spot conditions remain highly regional.)

|

Volume’s Holding Steady—But That Doesn’t Mean It’s Good

Freight volume ticked up just a bit this week, landing at 10,023. That’s enough to keep things from crashing, but don’t take it as a green light. Volume is steady, not strong—and that’s a big difference.

What we’re seeing right now is just enough freight to keep the wheels turning, but not enough to lift rates across the board. And because there’s not a lot of extra freight floating around, more trucks are chasing the same loads. That makes it tougher to win loads at a good price—especially if you’re depending on load boards.

Bottom line? There’s freight out there, but you have to be more strategic about where you run. Some areas are flooded with trucks and paying dirt-cheap. Others are tight and offering better rates. That’s where your advantage is—figuring out where trucks are scarce and jumping on it before everyone else does.

Don’t worry about national numbers or flashy headlines. Focus on the zip codes and regions that give you leverage. That’s how you stay ahead.

|

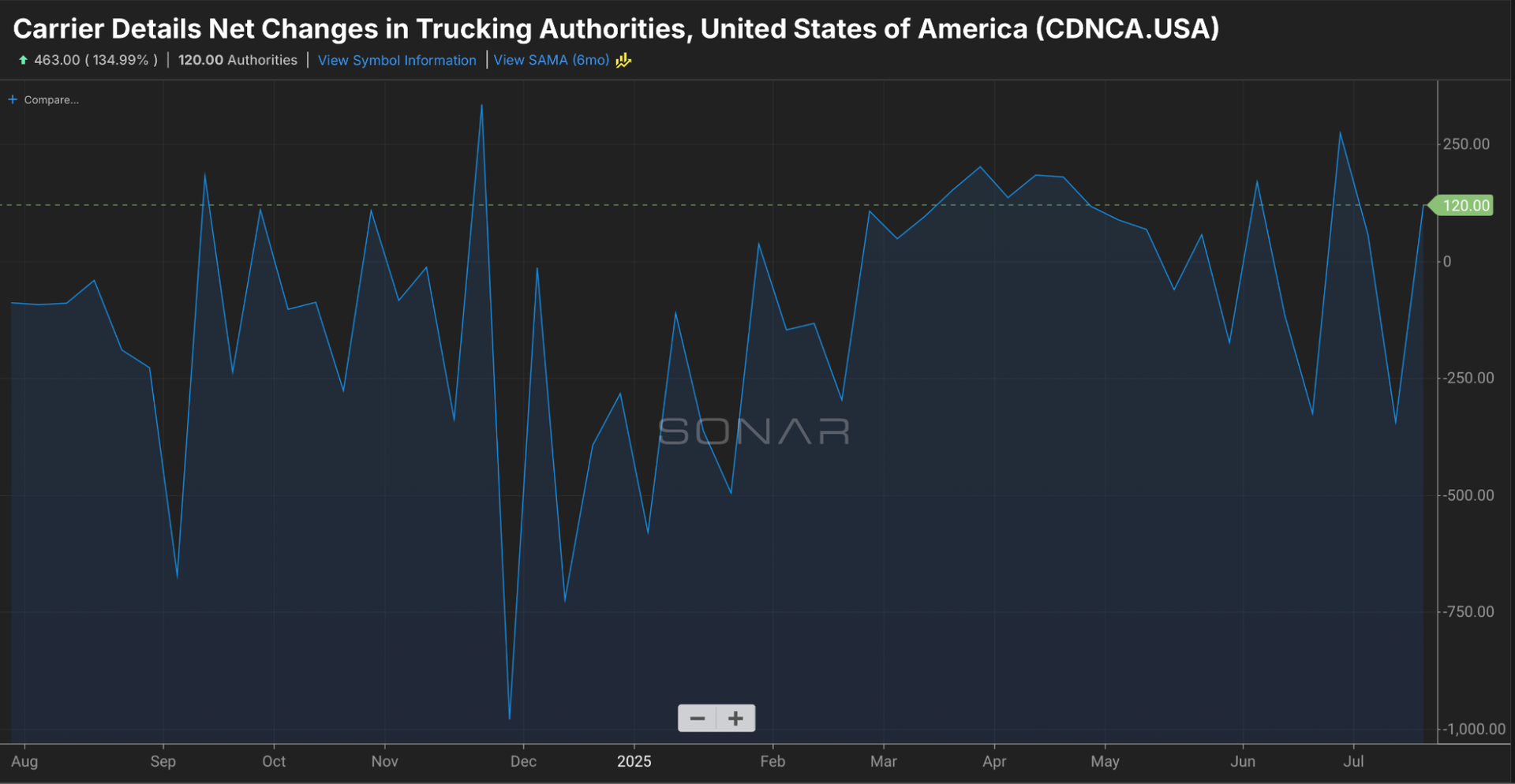

(Chart: SONAR Carrier Details Net Changes In Trucking Authorities (CDNCA.USA). Net new authorities rose by 120 last week—marking a slight return of capacity after a stretch of declines.)

|

Authority Gains Bounce Back – Net Increase of 120

After some wild swings over the past month, net carrier authority growth is back in the green—up by 120 last week. That’s not a flood, but it’s a noticeable rebound from the sharp drops we saw earlier this summer.

So what does that mean?

We’re still seeing folks dip their toe into the market—mostly newer carriers looking to make a move before peak season. But this isn’t a repeat of the 2021 gold rush. Most of the newcomers now are entering with eyes wide open, knowing they’ve got to run lean and smart to survive.

Here’s the play:

- If you’re already operating, a slow and steady gain in competition shouldn’t scare you—but it should tighten your pricing discipline.

- If you’re just getting started, don’t let this small bump in authorities fool you into thinking it’s easy money out here. It’s not.

This kind of modest growth shows us that capacity isn’t bleeding out like it was earlier this year, but we’re not in a full recovery either. That gives surviving carriers a small window of leverage—if they can hold their lanes, manage costs, and avoid rate-chasing.

This is still a war of attrition. Stay focused, stay selective, and let the weak fall off while you tighten your operation.

The Real Talk

Here’s the truth behind all this data: “flat” doesn’t mean “safe.” Flat just means the next drop is harder to predict.

Volumes are neutral. Rates are soft. Rejections are falling. And carriers are still trickling into the market. That’s not a setup for growth—it’s a warning shot for anyone flying blind.

If you’re relying on the same lanes, same brokers, same strategies week after week, you’re on borrowed time.

But if you’re adapting—using tools, tracking patterns, cutting costs, and raising your standards—this kind of market becomes a training ground, not a trap.

Keep grinding smart. The winners in Q3 won’t be the loudest, they’ll be the ones who move with purpose while others are playing catch-up.

Stay sharp. Stay strategic. Stay paid.

|

(Photo: Jim Allen/FreightWaves. A UPS sleeper-cab unit hauls twin trailers across the desert—while corporate leadership faces backlash over a controversial driver severance plan that union officials are calling both illegal and disrespectful.)

|

UPS Buyout Offer Sparks Union Outrage – And Raises Bigger Questions About Industry Workforce Strategy

|

This isn’t the first time we’ve covered the tensions rising inside UPS—but this week, it escalated.

UPS has officially rolled out a Driver Voluntary Severance Plan (DVSP) that offers full-time Teamsters $1,800 per year of service—to voluntarily walk away from their careers. On paper, it might sound like an early retirement package. But under the surface, it’s triggering alarm bells across the labor and freight landscape.

The Teamsters Union isn’t pulling any punches. They’ve publicly slammed the offer as “offensive and illegal,” accusing UPS of violating the National Master Agreement and undermining the value of long-term, union-protected work. According to Teamsters President Sean O’Brien, this isn’t a good-faith offer—it’s a pressure tactic aimed at thinning the workforce without honoring the full weight of retirement protections and earned benefits.

And here’s the bigger freight picture: This isn’t just about UPS. It’s about what happens when corporate freight strategy leans toward cutting experienced labor for short-term financial optics—without addressing the operational consequences.

Let’s break this down:

- Retirements and buyouts mean fewer experienced drivers—right as the industry braces for a volatile Q3 and ongoing capacity shifts.

- Losing union-protected roles creates a ripple effect, making it harder for companies to attract skilled labor when they need it most.

- If UPS sets this precedent, it won’t stop there. Other asset-based carriers and parcel giants may start seeing early exits and buyouts as a cheaper fix than wage increases or long-term retention.

For independent carriers and small fleets, this matters because the freight labor ecosystem is interconnected. When large fleets destabilize their workforce, more pressure gets pushed downstream. You see it in tighter capacity, rushed training pipelines, and, yes—rate disruptions.

It’s also a signal to watch labor relations closer than ever. Just like fuel or volumes, workforce strategy is now a freight variable that small carriers can’t ignore.

Whether you’re running with W-2 drivers or contracting O/Os, the question becomes:

Are you investing in long-term people—or just short-term fixes?

UPS might be making headlines, but small carriers are the ones who’ll be left picking up the slack if this trend continues. Pay attention. There’s more to this than just a buyout letter.

|

|

|

This Week’s Podcast – Box Trucks, Vans, and the STL Freight Boom Nobody’s Talking About

|

This week’s episode takes us off the beaten path and straight into a freight opportunity hiding in plain sight—Small Truckload (STL). If you’ve been sleeping on cargo vans, box trucks, or under-CDL freight, you might be missing one of the most consistent and overlooked lanes in the game right now.

Adam sat down with Mike Ernst, President of Expedite All and a 25-year freight industry vet who’s been in the STL trenches long before it was trendy. Mike breaks down why STL is booming, what makes it different from traditional truckload, and why big shippers are finally waking up to the power of right-size freight.

In this episode, we unpack:

- What STL actually is—and why it’s more than just local routes or last-mile drops

- How time-sensitive and high-value freight is driving demand for box trucks and cargo vans

- Why under-CDL carriers are finding surprising consistency (and less competition) in STL

- How to price STL loads profitably without falling into the “cheap freight” trap

- What STL success looks like—from equipment strategy to client relationships

This isn’t about chasing crumbs—it’s about building a real business model outside of the megacarrier blueprint. Mike lays out how STL can fit into a broader growth plan, whether you’re just getting started or looking to diversify beyond your current equipment.

If you’ve ever asked, “Can I grow without a sleeper and a 53-footer?” — this episode is your answer. Because small trucks are doing big things in this market—and the smart money is already on the move.

|

(Photo: US Senate.Chris Spear, President of the American Trucking Associations, delivers comments during the U.S. Senate hearing this week—highlighting concerns around safety enforcement, double brokering, and the urgent need for stronger oversight.)

|

Congress Just Turned the Heat Up – And Small Carriers Are in the Crosshairs

|

If you’ve been waiting for Washington to finally address the trucking chaos—fraud, safety, and regulatory mess included—this week delivered a wake-up call that can’t be ignored.

During a Senate Commerce Committee hearing, lawmakers from both sides of the aisle got loud about one thing: our current trucking oversight system is broken. And for once, the frustration didn’t just stop at finger-pointing. It came with receipts, real consequences, and a clear demand for accountability.

Senator Maria Cantwell kicked things off with a direct shot at the Federal Motor Carrier Safety Administration (FMCSA), pointing out the rise in fatal truck crashes—up 35% over the last decade—and calling out the agency for doing “nothing” in response to key watchdog recommendations. That wasn’t exaggeration—it was backed by a 2017 Inspector General report and a sharp warning from the Government Accountability Office that critical safety recommendations have been sitting untouched.

Let that sink in. The FMCSA’s own shortcomings are now in the congressional spotlight—and the ripple effects are going to touch everyone with a DOT number.

Why This Hearing Was Different

This wasn’t the usual surface-level soundbite. Senators dug deep:

- Carrier vetting? Broken. Too many bad actors are flying under the radar.

- Safety audits? Outdated. The FMCSA has failed to keep up with the pace of new authorities and fraud rings.

- Crash response? Weak. Families of victims from preventable truck crashes spoke out, demanding stronger oversight and consequences for negligence.

And while the discussion included large-scale reforms and future policy, it’s the immediate fallout that should have every small carrier paying attention.

Here’s what’s likely coming next:

- Stricter FMCSA audits. Especially for new carriers, safety scores, and insurance records will come under tighter review.

- Fraud enforcement. Double brokering and identity theft scams weren’t just mentioned—they were condemned. New verification tools and carrier vetting protocols are being fast-tracked.

- Congressional follow-through. Several senators, including Sen. Jon Tester and Sen. Tammy Baldwin, pushed hard for immediate oversight. Not in six months. Now.

What This Means for Small Carriers

If you’re a one-truck operation or a small fleet trying to stay compliant while navigating rates, this moment matters more than it may seem.

Because the folks cutting corners? They’re putting targets on everyone’s back. The more fraudulent MCs slip through, the more pressure comes down on the legit ones.

We’re likely entering a stretch where:

- Audits may get tougher.

- Insurance requirements could shift.

- Bad paper trails will get exposed.

If your paperwork isn’t in order—safety files, UCR, BOC-3, insurance records, hours of service—you could become collateral in the coming enforcement wave.

But here’s the flip side: carriers doing it right have a shot at standing out.

This new wave of scrutiny means brokers, shippers, and even compliance tech platforms will be more selective. And the carriers who can prove safety, consistency, and clean records? They’ll rise while the pretenders fall.

Bottom Line

Congress is finally pulling the curtain back on the trucking oversight crisis—and FMCSA is on notice. What happens next will shape the regulatory tone for the rest of the year and beyond.

So the real question isn’t whether change is coming.

It’s whether you’re ready when it does.

If you’ve been putting off cleaning up your compliance game, this is the time to act. Because when enforcement hits—and it will—you don’t want to be scrambling. You want to be the one shippers trust, brokers prefer, and FMCSA leaves alone.

|

Final Word – Clarity Over Chaos

|

If this week showed us anything, it’s that there’s no one-size-fits-all narrative in freight right now. Volumes ticked back above 10,000 on the OTVI, but rejections slid again. Rates held steady at $2.31, but that number doesn’t tell the story lane-by-lane. Meanwhile, regulators are in limbo, UPS is in damage control, and STL freight is heating up while Class 8 orders dip.

We’re not in a down market—we’re in a split market. Where you operate, what you haul, and how you adapt are defining success more than any national average.

So what does that mean for you?

It means watching the broader trends—but making local moves. It means doubling down on profitable relationships, not just posted rates. And it means paying closer attention to political and policy shifts, because they’re shaping the conditions you’ll be driving in next quarter.

This isn’t the time to coast. It’s time to calibrate.

Because while others wait for the market to “return,” the ones who are thriving are already adjusting—diversifying, negotiating smarter, running leaner, and building networks that last.

That’s the mindset we bring here every week. And that’s why the Playbook isn’t about hype—it’s about readiness.

Let’s keep building that edge. Mile by mile. Strategy by strategy.

We’ll see you out there.

|

|

|

|