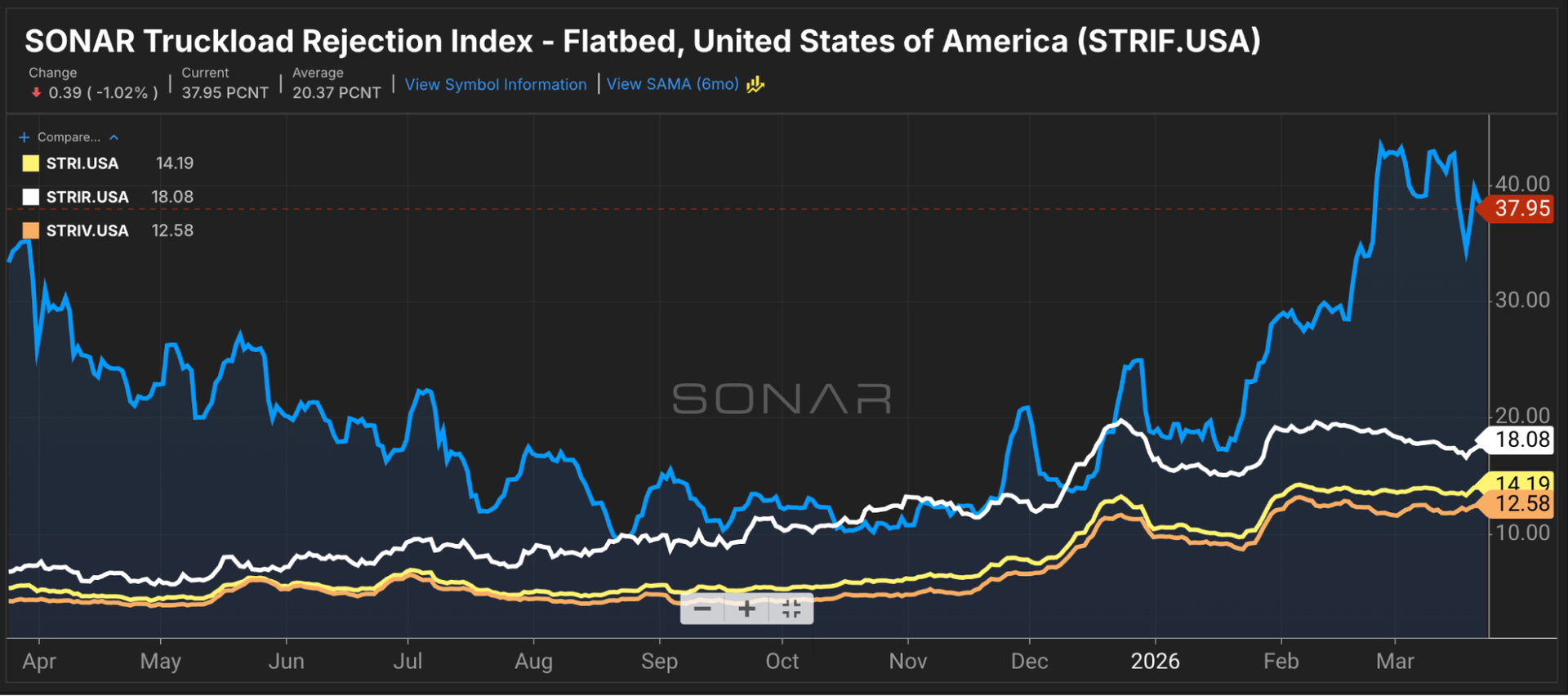

Summary: Flatbed outbound tender rejection rates remain elevated well beyond typical spring seasonality, signaling genuine tightness in the open-deck market.

The SONAR Flatbed Truckload Rejection Index (STRIF.USA) declined 38 basis points last week to 37.95 percent from 38.77 percent on March 16. While that is 264 basis points below last month’s peak of 40.59 percent, it remains 457 basis points higher than the same week last year.

Flatbed tender volumes have also strengthened, rising 9 percent compared with the prior month and 8 percent year-over-year.

Warmer weather and the normal resumption of construction projects typically boost open-deck activity this time of year. However, the current rally runs considerably deeper than pure seasonality.

The demand surge is supported by improving manufacturing signals, a construction boom and rising steel output. The Institute for Supply Management’s Manufacturing PMI registered 52.6 percent in January and 52.4 percent in February, marking the second consecutive month of expansion, with new orders at 57.1 percent and 55.8 percent, respectively.

Steel production, a key driver for flatbed freight, is showing solid gains. According to the American Iron and Steel Institute, U.S. raw steel output reached 1.781 million net tons for the week ended March 21, up 4.6 percent from the same week in 2025. Year-to-date production through March 21 totals 20.394 million net tons, 4.9 percent higher than a year earlier, with capacity utilization at 77.0 percent.

FreightWaves founder and CEO Craig Fuller has noted that much of the strength is coming from the industrial Midwest — particularly steel, aluminum and copper — rather than the still-weak housing sector.

DAT Principal Analyst Dean Croke attributes a significant portion of the flatbed strength to AI-driven data center construction. In a March 12 interview with Trucking Dive, Croke said the flatbed spot market “has been on fire for 18 months” due to heavy demand for equipment and power-generation projects tied to data centers.

On the supply side, ongoing carrier bankruptcies and tighter regulations have limited available capacity, allowing carriers to be more selective. The combination of these factors has produced one of the strongest flatbed markets in recent years heading into the second quarter.