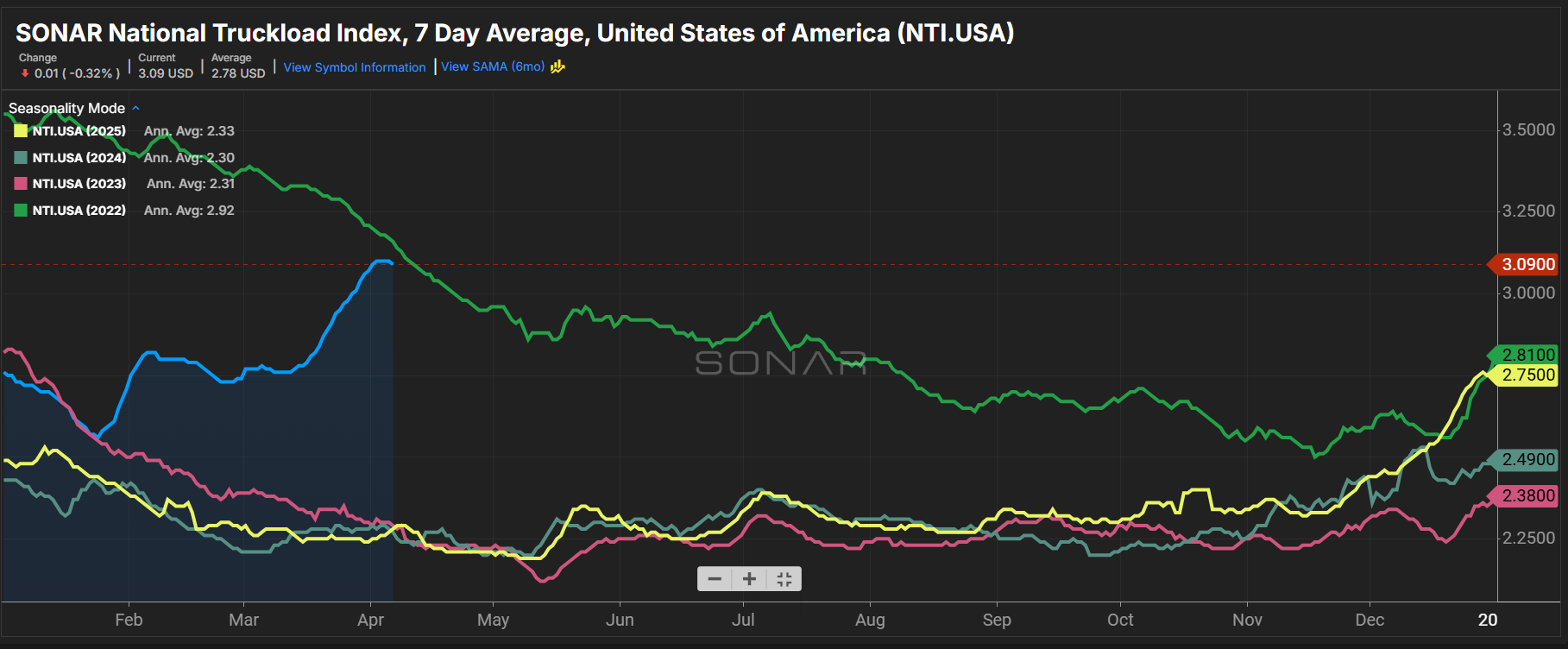

Summary: The mid-March rally in dry van spot rates has taken a brief pause in the first week of April. Despite the slowing in weekly gains compared to the last four years, all-in spot rates continue to be at their best levels since 2022.

The SONAR National Truckload Index 7-day average (NTI) rose 3 cents per mile all-in week-over-week from $3.06 on March 30 to $3.09 per mile. The NTI is 32 cents per mile, or 11.6%, higher than $2.77 last month and 80 cents per mile, or 35%, higher than $2.29 last year.

Weekly gains were much lower in spot market linehaul rates. The SONAR National Truckload Index Linehaul Only (NTIL) gained only 1 cent per mile week-over-week from $2.23 to $2.24 per mile. The NTIL is 10 cents per mile, or 4.7%, higher than last month and 51 cents per mile, or 29.5%, higher than $1.73 per mile last year.

Fuel costs for the NTIL are based on the average retail price of diesel fuel and a fuel efficiency of 6.5 miles per gallon. The formula is NTID – (DTS.USA/6.5).

Speaking of fuel costs, the price of diesel paid at the pump nationwide continues to rise. The Diesel Truck Stop Actual Price Per Gallon (DTS) rose 24 cents per gallon week-over-week from $5.42 per gallon to $5.66. The DTS is $1.21 per gallon, or 25%, higher than last month. Compared to last year, the DTS is $2.00 per gallon, or about 55%, higher.

The most recent Logistics Managers’ Index (LMI) reading for March showed transportation capacity continuing to contract, falling to 39.2 points. Transportation prices surged to 89.4, the widest price-to-capacity spread seen since the COVID-19 pandemic. The LMI shows a value over 50 as expansion, while a value below 50 indicates contraction.

Looking ahead, trucking capacity is gaining better pricing power while being negatively impacted by higher fuel costs. Larger fleets are less exposed due to fuel surcharges, while smaller fleets and owner-operators are most affected.

This dichotomy stems from fleet size: smaller fleets often cannot negotiate favorable fuel-buying plans, relying instead on fuel cards that save only cents on the gallon. Additionally, many of them are more likely to have higher exposure to the spot market, where prices are quoted all-in, and are more likely to be impacted by truckload supply and demand.